- Sellers reduce offers by INR 300/t amid poor demand

- Hike in fuel prices keep market uncertain now

Pellet prices in Raipur moved lower on a w-o-w basis, with producers reducing offers amid subdued demand from the downstream steel segment. Market sentiment remained cautious, as weakness in sponge iron and billet segments continued to weigh on buying interest.

Trades and price movements

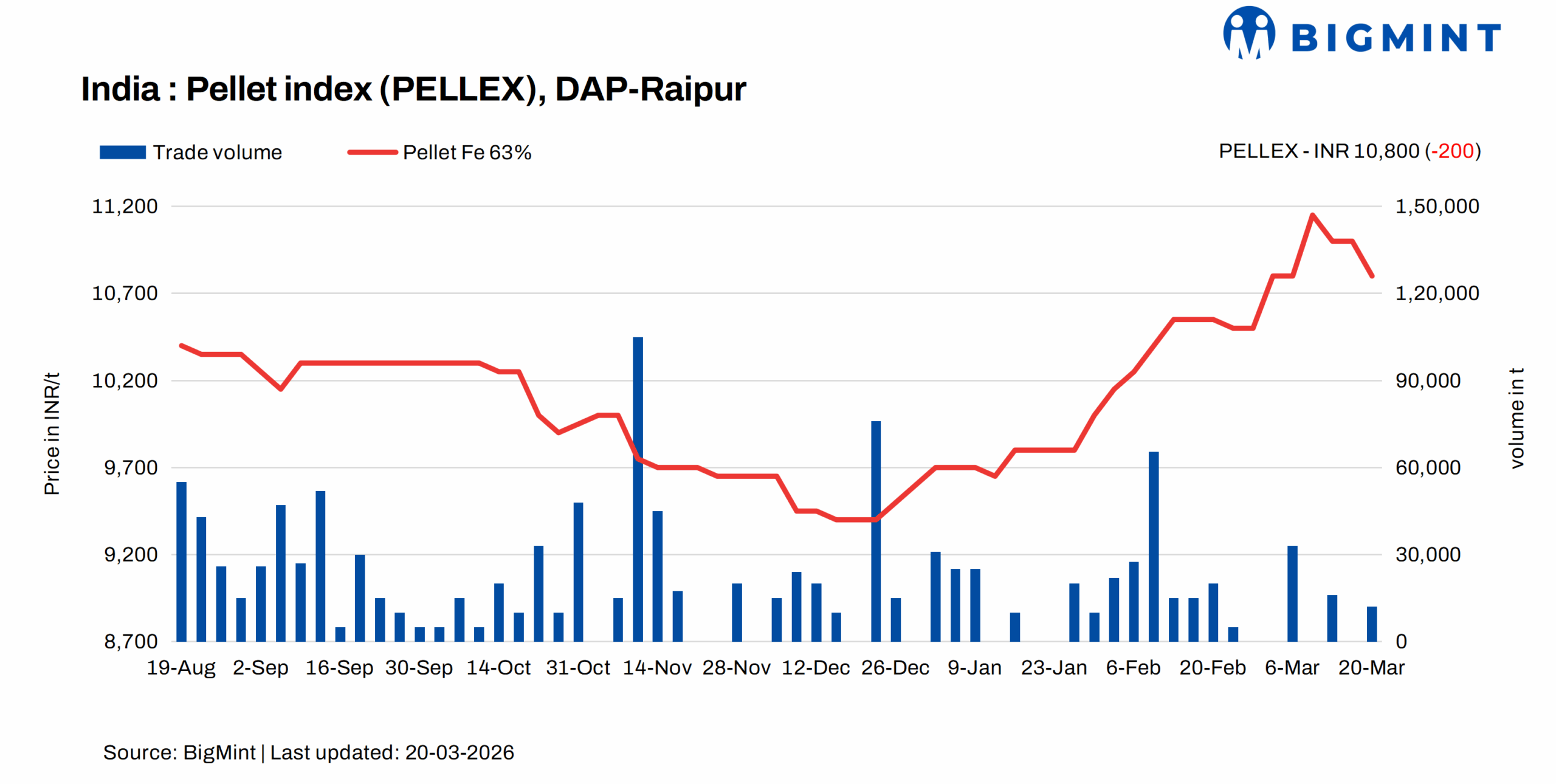

PELLEX, BigMint’s bi-weekly domestic pellet (Fe 63%) index for Raipur, decreased by INR 200/t to INR 10,800/t DAP on 20 Mar against 13 Mar, reflecting softer market conditions.

Offers for Fe 62.5-63% (+/-0.5%) grade pellets were heard lower at INR 10,600-10,800/t exw Raipur, translating to around INR 10,850/t DAP. Two deals totalling around 12,000 t were recorded at INR 10,750-10,850/t DAP, indicating limited but active spot-level transactions.

The reduction was fuelled by lower demand and a fall in sponge iron prices by INR 600/t ($6/t) w-o-w to INR 26,300/t ($281/t) exw.

Market dynamics

Overall, trading activity remained slow, with sellers lowering offers slightly amid weak enquiries, while buyers continued to stay cautious. The market largely remained in a wait-and-watch mode, with limited clarity on near-term price direction and no urgency from either side to conclude bulk deals.

A Raipur-based seller said, “We have reduced our offers slightly, but enquiries are still not very encouraging. Buyers are holding back for now. We are expecting some inquiries now as prices has dropped.”

A trader noted, “There is pressure from the sponge iron and billet side, so buyers are not willing to commit at higher levels.”

Participants indicated that pellet prices are expected to remain under pressure in the immediate term, with no sharp correction visible yet. A clearer direction is likely to emerge next week, post the Eid holidays, as trading activity normalises and participants return with fresh procurement plans.

A buyer said, “We are waiting for the price clarity as bids for lumps remained stable in the OMC auction, but fuel prices has incraesed, which may raise the iron ore prices. So the pellet will have better viability for raw material.”

Market participants also highlighted that they have yet to assess any immediate impact of the recent auction results by the Odisha Mining Corporation (OMC). While the auction witnessed healthy booking levels, its direct impact on pellet pricing is still unclear. Sellers are expected to reassess their price stance once there is more visibility on how Odisha-based players adjust their offers in response to these results.

In the meantime, buyers are closely monitoring raw material trends and holding back on aggressive purchases until a clearer pricing benchmark emerges. The gap between buyer expectations and seller offers continues to restrict deal closures, keeping volumes limited.

Meanwhile, some sponge iron producers continue to prefer iron ore lumps over pellets due to better cost economics, which is further weighing on pellet demand in the region.

Rationale

- PELLEX has been derived using data points, i.e., trades, offers, and bids. To download the detailed methodology, click here.

- Two (2) deals were recorded in this publishing window, and taken for calculation. Thus, the T1 trade category was accorded 50% weightage.

- Seventeen (17) firm offers, bids, and indicative prices were heard and thirteen (13) were taken for price calculation and given balance 50% weightage.

Key market drivers

- Sponge iron prices decline w-o-w: Sponge PDRI prices fell by INR 600/t w-o-w to INR 26,300/t exw Raipur, reflecting weak buying interest and cautious sentiment. While on a d-o-d basis the cluster rose by INR 200/t, as sellers revised offers upward amid volatile market conditions. Nevertheless, buyer response remained subdued, with procurement largely restricted to need-based volumes.

- Billet prices down w-o-w: BigMint’s billet index in Raipur dipped by INR 300/t w-o-w; buoyed by slower response from buyers. In contrast, prices inched up by INR 50/t d-o-d to INR 41,550/t ex-works on 20 March 2026, marking a marginal recovery after recent corrections. The market remained largely range-bound, with limited transactions concluded mainly for immediate requirements.

Outlook

Pellet prices in Raipur are expected to remain under pressure in the near term. While no immediate upward movement is visible, a clearer trend may emerge next week post-holiday, with potential support from any uptick in fines prices, while lump prices are likely to remain largely stable.

Leave a Reply