- Demand improves; supply tightness persists

- Mills push prices higher; further hike expected

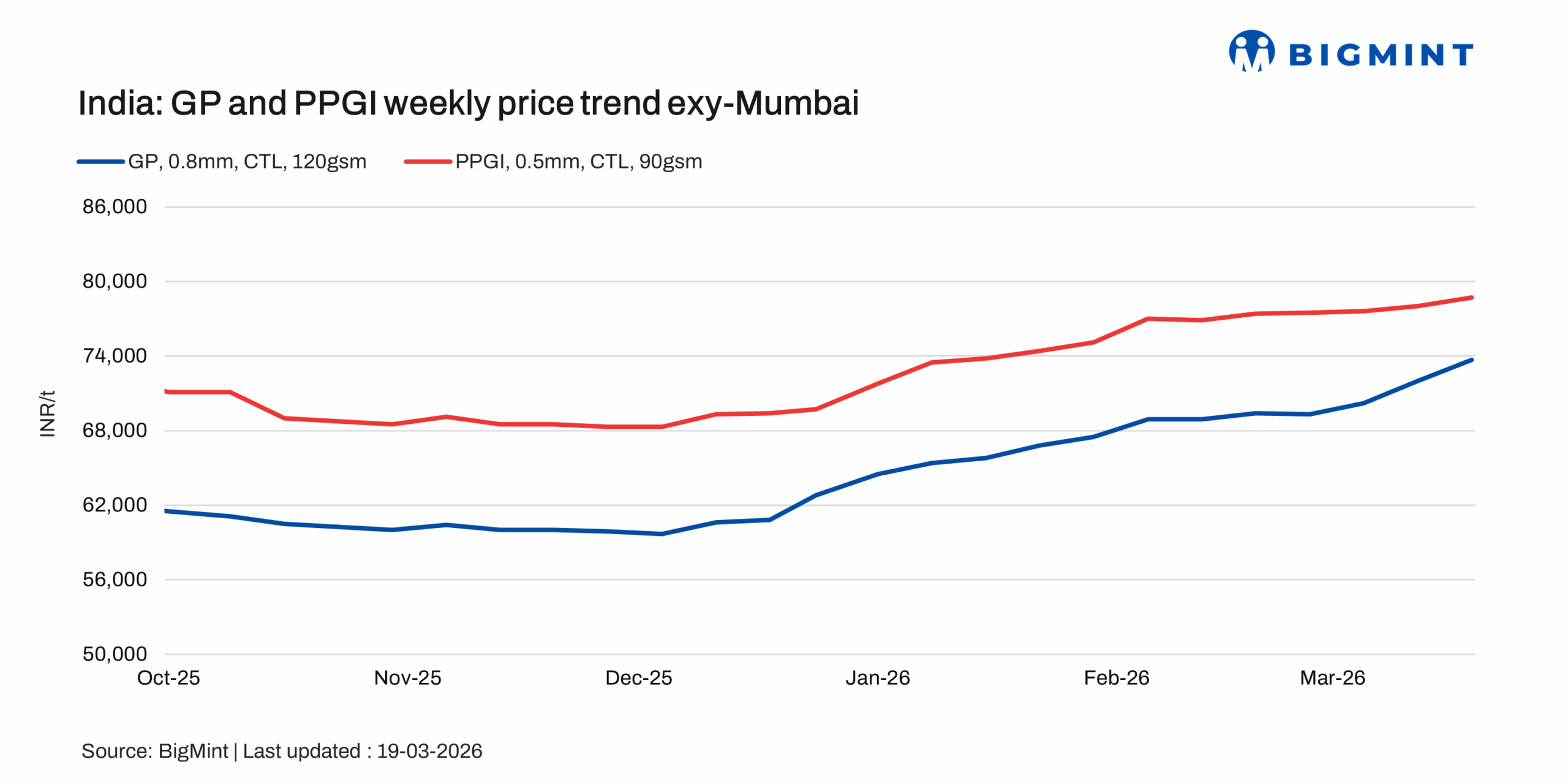

Indian coated flat steel prices moved up w-o-w across segments, supported by mill price hikes and tight supply conditions. GP prices increased in the range of INR 300-2,500/t, while PPGI prices rose by INR 700-1,100/t. BGL prices also moved up by INR 1,300-1,500/t during the same period.

Market activity in the coated segment showed relatively better movement compared to other finished flat products such as HRC and CRC, which remained comparatively slower. Participants also reported some supply tightness in select grades, supporting the upward price trend.

Additionally, mills are actively pushing prices in the market, and trade discussions indicate the possibility of another round of price increases in the near term.

Price update

Benchmark assessment for GP coil (exy-Mumbai) increased by INR 1,700/t ($/t)w-o-w to INR 73,700/t, ($790/t)compared with INR 72,000/t ($772/t) last week. Market offers were largely reported in the range of INR 73,500-74,500/t ($788-799/t), indicating improved mill realisations despite cautious buying sentiment.

PPGI prices (exy-Mumbai) also moved up by INR 700/t ($7/t)w-o-w to INR 78,700/t,($844/t) against INR 78,000/t ($836/t) previously. Market offers were heard in the range of INR 78,000-79,500/t ($836-853/t), reflecting steady demand and firm pricing trends.

BGL prices (exy-Mumbai) witnessed an increase of INR 1,300/t ($14/t)w-o-w to INR 84,000/t ($901/t), compared with INR 82,700/t ($887/t) last week. Market offers were largely reported in the range of INR 83,500–84,500/t ($895-906/t), supported by continued tight availability in the market.

Market updates

Demand in the coated flat steel segment remained comparatively better than other flat products, with improved activity observed during the assessment period. The market also witnessed material shortage in select grades, which, along with expectations of further price increases by mills, led to instances of panic procurement by traders and end-users.

In the western and northern regions, demand conditions ranged from normal to good, supported by steady enquiries and trading volumes. Overall, the market maintained a reasonable demand outlook, with buying interest sustained despite cautious sentiment in other flat steel segments.

Participants continue to monitor supply conditions closely, as availability constraints and ongoing mill pricing strategies are likely to influence near-term market direction.

Raw material prices

India’s zinc ingot (99.995%) prices declined by INR 2,600/t w-o-w to INR 3,31,600/t ex-Delhi as of 17 March, reflecting subdued domestic sentiment despite relatively firm global cues. A recent price cut by a leading domestic producer to INR 3,40,000/t ex-Chanderiya further weighed on market sentiment. Meanwhile, LME three-month zinc futures eased by $39/t w-o-w to $3,327/t, offering limited external support.

On the finished steel front, leading Indian mills increased list prices of HRC and CRC by INR 1,000-1,500/t for mid-March 2026 sales. HRC (2.5–8 mm, IS2062, Gr E250 Br) list prices were reported in the range of INR 55,250-57,000/t ex-Mumbai, while CRC (0.9 mm, IS513 CR1) prices were heard at INR 63,200–64,250/t.

On a month-on-month basis, trade-level HRC prices increased by INR 1,500/t to INR 55,300/t in March, compared with INR 53,800/t in February. Similarly, CRC prices rose by INR 1,700/t to INR 61,400/t from INR 59,700/t during the same period.

As per BigMint’s bi-weekly benchmark assessment, HRC (IS2062, Gr E250, 2.5–8 mm/CTL) prices increased by INR 1,000/t w-o-w to INR 56,500/t on 17 March compared with INR 55,500/t in the previous week.

Similarly, CRC (IS513, Gr O, 0.9 mm/CTL) prices were assessed at INR 62,800/t, up by INR 1,200/t w-o-w from INR 61,600/t in the last assessment. These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Outlook

The coated flat steel market is showing improving demand, supported by better activity and supply tightness in certain regions. Demand is expected to strengthen further, while mills continue to push prices. Market sentiment indicates a high likelihood of another price increase in the coming weeks.

Leave a Reply