- HMS (80:20) prices remain unchanged d-o-d

- Rebar prices in Chennai up INR 200/t w-o-w

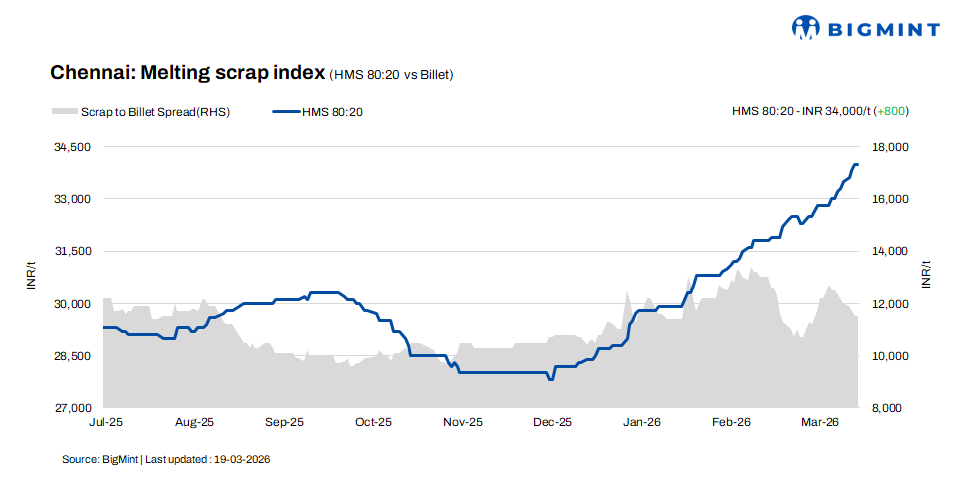

In the Chennai market, HMS (80:20) scrap prices increased by INR 800/t w-o-w to INR 34,000/t on 19 March 2026, while remaining unchanged on a daily basis, as per BigMint’s assessment. The rise was supported by steady buying activity. Billet prices remained stable at INR 45,500/t on both d-o-d and w-o-w basis, reflecting balanced market conditions. Meanwhile, rebar prices edged up by INR 200/t w-o-w to INR 50,200/t, holding firm on a daily basis. Stable billet prices and firm rebar demand indicate a balanced yet cautiously positive market sentiment, supporting scrap price stability.

Imported and domestic price trends

Market participants reported that Australia-origin shredded scrap was offered at $380-385/t CFR Chennai, while HMS (80:20) was quoted at $360-365/t CFR. However, buyers were bidding $5-10/t lower than the prevailing offer levels. Buying interest remained subdued, as domestic scrap offers are currently more cost-effective compared to imported material, thereby limiting fresh bookings.

In the domestic market, HMS (80:20) scrap prices were assessed at INR 33,500-34,500/t for immediate payment, while transactions on extended credit terms were concluded at higher levels of INR 34,000-35,000/t. The price variation reflects the impact of payment terms on deal levels, with suppliers factoring in credit risk and liquidity conditions.

Buyer-supplier sentiments

A mill representative noted that sponge iron supply in the merchant market has improved, with additional inflows from neighbouring states at more competitive rates, supporting overall market availability. Meanwhile, billet demand from Kerala has strengthened for Chennai-based suppliers, providing some support to trade activity. However, rerolling mills in Chennai are continuing with need-based procurement, as rebar demand remains at a moderate level. With state elections announced, major government projects are likely to slow down or temporarily halt, which may impact finished steel demand in the coming weeks.

A scrap supplier indicated that HMS (80:20) prices were currently hovering in the range of INR 33,500-35,000/t, with variations largely dependent on payment terms and mill-specific volume requirements. Market sources highlighted that the ongoing Iran-Israel war has disrupted the availability of commercial gas, leading to supply shortages. As most processors rely on gas-based cutting, the sharp rise in gas prices now more than double the usual levels has increased operational costs. Amid rising input costs, suppliers expect further upward movement in scrap prices in the near term.

Regional comparison

In the western India based Jalna market, rebar and HMS (80:20) scrap prices remained stable at INR 51,300/t and INR 32,900/t, respectively. Meanwhile, billet prices edged down by INR 100/t to INR 43,700/t. Market participants reported a slight softening in finished steel trading activity compared to recent sessions. Prices are expected to remain largely stable in the near term, supported by adequate scrap arrivals, which are sufficient to meet mills’ current production requirements.

Outlook

The Chennai scrap market is expected to remain stable. Domestic scrap prices are supported by costlier processing due to gas issues and steady mill procurement. However, subdued interest in imported scrap due to higher offers may keep supply largely domestic-driven. Amid moderate rebar demand and stable billet prices, scrap prices are likely to trade in a narrow range with a slight upward bias.

Leave a Reply