- Weak steel demand affects buying activity

- Firm import parity, higher coking coal costs support prices

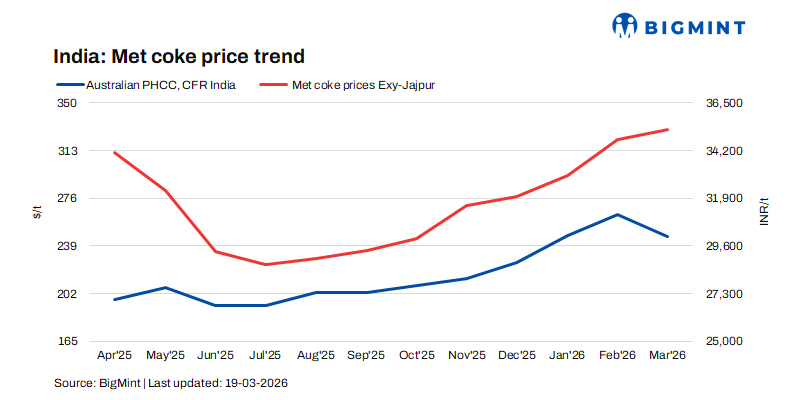

Price trend and domestic market movement

Indian blast furnace (BF)-grade metallurgical coke prices remained stable week-on-week as of 18 March 2026, reflecting subdued demand conditions across the domestic steel value chain.

According to BigMint’s assessment, BF-grade coke (25-90 mm) prices in eastern India held steady at INR 35,000/t ex-Jajpur, while prices in western India were unchanged at INR 31,000/t ex-Gandhidham. Similarly, foundry-grade coke (+90 mm) prices remained stable at INR 36,000/t ex-Rajkot.

Market participants indicated that trading activity remained limited as buyers were cautious amid weak steel demand and rising logistics costs. Additionally, reduced container availability and higher transportation expenses further discouraged fresh procurement, leading to minimal spot market transactions.

Import parity and raw material dynamics

Firm import parity continues to lend underlying support to domestic coke prices despite the prevailing weak demand conditions. According to BigMint’s assessment, Indonesian-origin BF coke (65/63) was assessed at $281/t CFR India, reflecting a decline of $5/t w-o-w.

Freight rates from Indonesia to India have reportedly softened to around $25-30/t, which could moderately ease the landed cost of imports. However, buying interest remains cautious, with buyers placing bids $5-10/t below prevailing offer levels, indicating resistance to higher prices amid sluggish downstream consumption.

On the raw material front, Australian premium hard coking coal prices increased by $5/t w-o-w to $222/t FOB. The uptick in coking coal prices continues to sustain cost pressure on coke producers, thereby limiting the scope for any significant correction in domestic coke prices despite subdued demand.

Global market influence

China’s domestic coking coal and coke markets remained largely stable during the period. Prices for quasi-grade dry-quenched coke were unchanged as coal mines maintained normal production levels, ensuring steady supply.

Steel mills continued to procure raw materials primarily based on immediate production needs. Although blast furnace utilisation improved slightly, weak downstream steel demand restrained aggressive procurement, resulting in a stable but cautious market outlook in China. This stability in China has indirectly contributed to the steady sentiment in regional coke markets.

Downstream demand indicators

Downstream demand signals remain weak, particularly in the pig iron segment. Steel-grade pig iron prices in Durgapur declined by INR 150/t w-o-w to INR 37,600/t ex-works, reflecting subdued buying interest from steelmakers.

Market participants reported that buyers remain reluctant to procure material at elevated price levels, resulting in limited deal activity in both the pig iron and coke markets. The overall slowdown in steel demand continues to influence raw material purchasing behaviour.

Market outlook

Domestic metallurgical coke prices are expected to remain range-bound, supported by firm import parity and elevated coking coal costs, while weak steel demand and cautious buying are likely to keep trading activity limited.

Leave a Reply