- Indian mills lift HRC, CRC sharply

- Bullish sentiment amid supply concerns

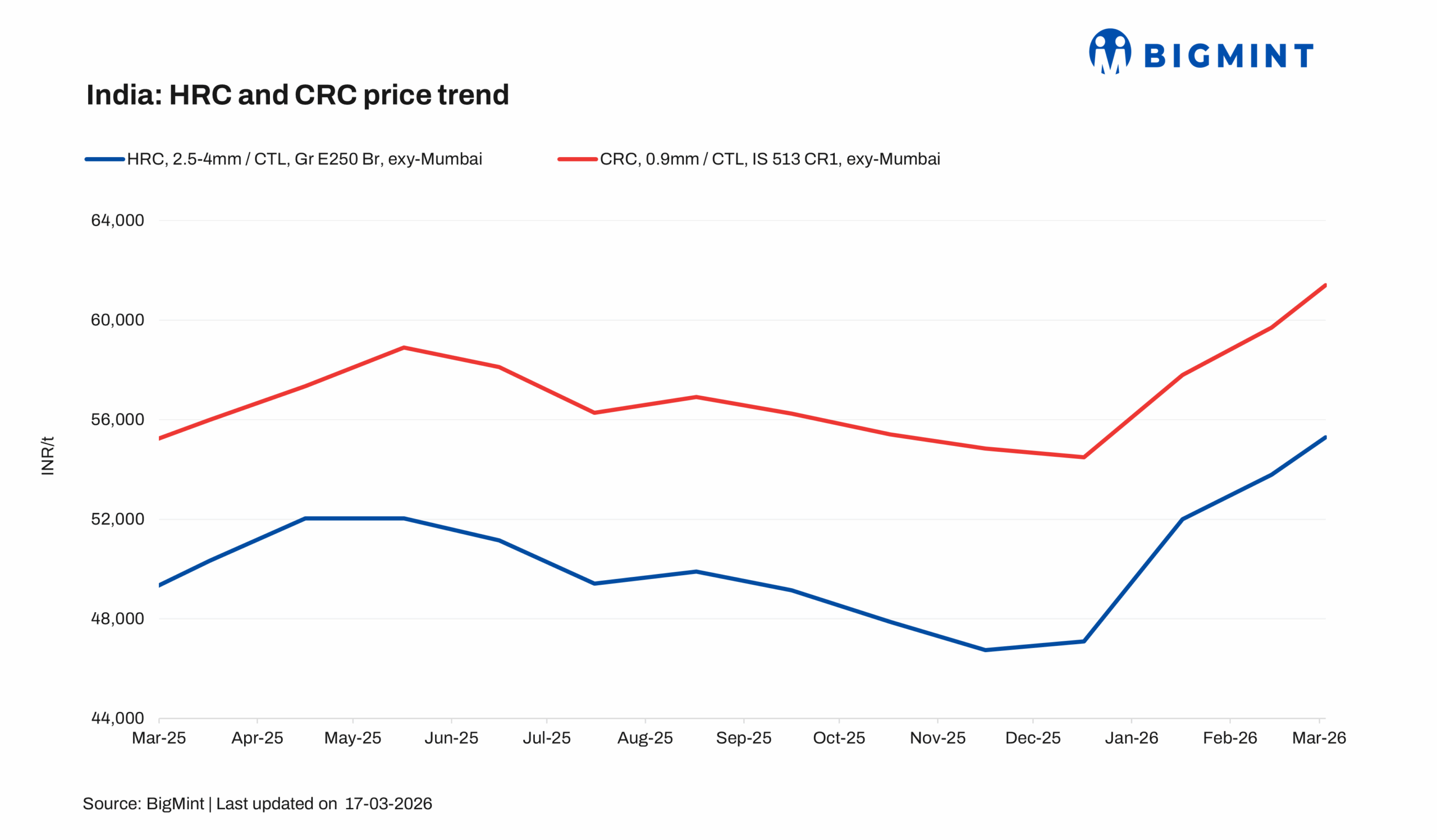

Leading Indian steelmakers have increased list prices of hot-rolled coils (HRCs) and cold-rolled coils (CRCs) by INR 1,000-1,500/t ($11-16/t) for mid-March 2026 sales. List prices of HRCs (2.5-8 mm, IS2062, Gr E250 Br) ranged within INR 55,250-57,000/t ($598-617/t) ex-Mumbai. Moreover, CRCs (0.9 mm, IS513 CR1) were listed at INR 63,200-64,250/t ($684-695/t).

M-o-m, trade-level HRC prices rose by INR 1,500/t ($16/t) to INR 55,300/t ($599/t) in March 2026 compared with INR 53,800/t ($583/t) in February 2026. Meanwhile, CRC prices surged by INR 1,700/t ($18/t) to INR 61,400/t ($665/t) from INR 59,700/t ($647/t) in the same period.

W-o-w price assessment

BigMint’s benchmark assessment (bi-weekly) for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) prices increased by INR 1,000/t ($11/t) w-o-w to INR 56,500/t ($612/t) on 17 March against INR 55,500/t ($601/t) in the same period last week.

CRC (IS513, Gr O, 0.9 mm/CTL) prices stood at INR 62,800/t ($679/t) as assessed on 17 March, up by INR 1,200/t ($13/t) w-o-w against INR 61,600/t ($666/t) on Tuesday. These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Market Update

Indian trade-level sentiment for both HRC and CRC prices remains firmly bullish, underpinned by geopolitical uncertainty and ongoing supply-side constraints. Rising tensions between Iran and Israel have injected volatility into global commodity markets, prompting traders and distributors to build inventories in anticipation of potential supply disruptions. This stocking activity, along with tight material availability, particularly in northern regions, has resulted in a sharp w-o-w increase in HRC prices.

Simultaneously, market chatter indicated that, “constrained availability of fuel and gas may disrupt mill operations, leading to reduced downstream production and encouraging mills to divert surplus HR material into the open market”. Consequently, HR prices continue to be supported by precautionary buying as well as persistent supply and operational challenges.

In comparison, CR market sentiment remains tighter, as downstream production of CR and coated products is being impacted by limited LPG availability. Market participants informed Bigmint, “if the current geopolitical situation continues for the next 10–15 days, the price gap between HR and CR is likely to widen further”. Additionally, a financial crunch in the market has emerged as a key concern, which may weigh on purchasing capacity and overall trade liquidity.

Additional updates

Import volumes: India’s bulk imports of HRCs touched 47,025 t as of 13 March, based on vessel line-up data. Around 166,902 t of additional cargoes are expected by late-March.

Export volumes: India’s bulk exports of HRCs touched 61,000 t as of 13 March. Around 144,000 t of additional cargoes are in transit.

Outlook

In the near term, HRC prices are expected to remain elevated with a firm upward trajectory, underpinned by ongoing supply constraints and recent mill price hikes. However, market participants remain vigilant regarding any de-escalation in Iran-Israel tensions, as well as shifting demand-supply dynamics that could alter the price trend.

Leave a Reply