- Freight surge, global disruptions support price surge

- Raw material costs firm, buyers remain cautious

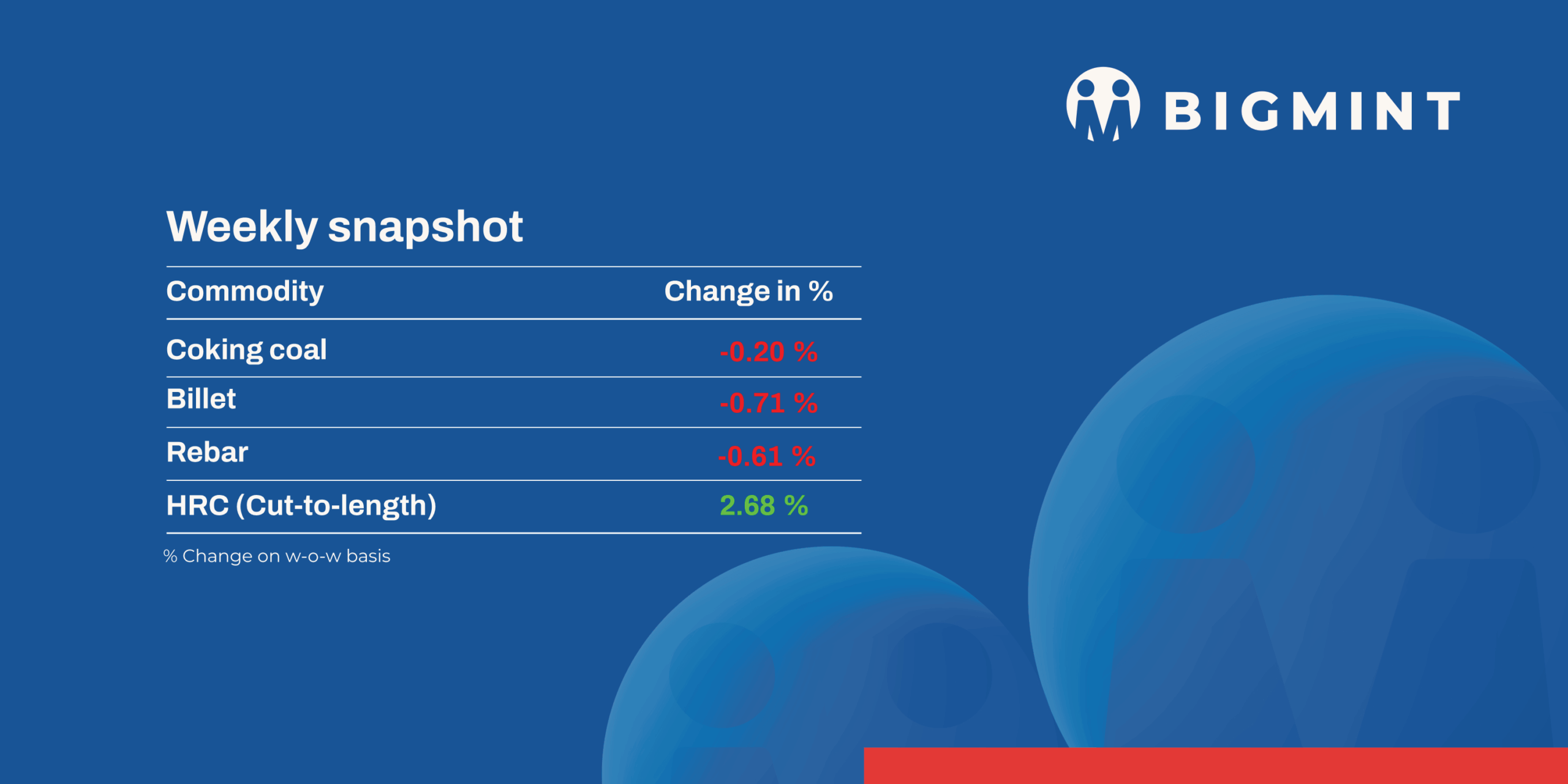

The Indian steel market showed mixed trends this week as raw materials prices remained firm, rebar prices rose, while buyers remained cautious amid geopolitical tensions. An overview:

Iron ore and pellet

- Jindal Steel emerged as the highest bidder for two iron ore mine blocks in Keonjhar district, Odisha: Thakurani-A1 (101.20% premium; 50.532 mnt resources), and Rengalaberha North-East Extension & Nuagaon West (111.15% premium; 37.95 mnt resources). Meanwhile, Kashvi Power and Steel won the Jajang-A Iron and Manganese block with a 127.01% premium, holding 16.05 mnt of iron ore resources.

- BigMint’s Fe 57% low-grade iron ore fines export prices rose $1.5/t w-o-w to $61.5/t FOB east coast on 12 March, supported by firmer global iron ore trends and a few export deals of around 250,000 t during the assessment window. However, exporters remained cautious amid rising vessel freight and ongoing Middle East geopolitical tensions, which are squeezing margins.

- PELLEX, BigMint’s bi-weekly domestic pellet (Fe 63%) index for Raipur, increased by INR 200/t w-o-w to INR 11,000/t ($119/t) DAP on 13 March supported by firmer sponge iron and semi-finished steel prices. However, trading activity remained slow, with buyers largely procuring to satisfy immediate needs.

Coal

- South African thermal coal prices at Indian ports increased w-o-w amid tight availability and higher freight. As per BigMint’s assessment, exw-Paradip RB2 (5,500 NAR) rose by INR 500/t to INR 12,200/t and RB3 (4,800 NAR) by INR 200/t to INR 10,600/t. Freight from Richards Bay to Paradip increased by $5.8/t w-o-w to $24/t, with levels heard around $22–25/t amid geopolitical tensions and higher oil prices. with levels heard around $22–25/t amid geopolitical tensions and higher oil prices. Buying remained limited as consumers held stocks until April and adopted a wait-and-watch approach. Offers for March-arrival cargoes at Mangalore were heard near INR 11,700/t for 5,500 NAR.

- Domestic non-coking coal prices increased by INR 150–250/t w-o-w, as per BigMint’s assessment. 4,500 GCV rose to INR 5,150/t and 5,000 GCV increased to INR 6,250/t exw Bilaspur. The rise was supported by active participation in the recent SECL auction and firm bids for higher grades. Additionally, SECL announced another auction offering 1,269,500 t of non-coking coal on 19 March covering grades G6 to G10, G12 and G13.

- BigMint’s PHCC index rose by $9/t w-o-w to $249/t CNF Paradip on 13 March, supported by higher vessel freights. Panamax freights from Haypoint to Paradip increased by over $4/t to $26.4/t. However, trade activity remained muted as buyers delayed bookings expecting lower prices, while Australian offers stayed range-bound. Meanwhile, domestic BF-grade met coke prices fell by INR 600/t to INR 35,000/t ex-Jajpur but held at INR 31,000/t ex-Gandhidham. Indian BF-rebar prices increased to INR 58,500-60,000/t landed, touching a three-year high.

Ferrous scrap

- Imported scrap sentiment in India remained firm this week as Middle East tensions disrupted trade flows and raised logistics risks. UK/EU-origin HMS (80:20) was indicated around $360-365/t CFR, while HMS 1 was heard near $370-375/t. Shredded scrap offers were reported at $385-390/t and PNS at $390-395/t CFR, although no trades were concluded as buyer bids remained lower.

- Freight rates surged sharply during the week, increasing from around $40 per container earlier to nearly $60-65, significantly raising landed scrap costs. Market participants also noted stronger buying interest from Pakistani mills, which limited scrap availability for Indian buyers. Meanwhile, rising oil prices and concerns over potential gas supply disruptions in India added pressure on mills, prompting many to adopt a wait-and-watch approach amid volatile global conditions.

Ferro alloys

- Silico manganese: Indian silico manganese (60-14) prices went up slightly INR 325/t ($4/t) w-o-w to INR 73,000 -74,300/t ($788-802/t ) across Durgapur, Raipur, Vizag, and Raigarh, supported by higher overseas raw material prices. Smelters raised offers as rising imported and domestic manganese ore prices lifted production costs, while firmer steel prices supported domestic silico manganese despite cautious export demand.

- Ferro manganese: Indian ferro manganese (70%) prices maintained stability with prices staying unchanged w-o-w to INR 74,200/t ($801/t) in Raipur while, moved up by INR 300/t ($3/t) to INR 74,100/t ($800/t) in Durgapur. Stable ferro manganese prices reflected balanced demand from alloy buyers and adequate domestic supply, preventing significant price movement during the week.

- Ferro silicon: Indian ferro silicon (Si 70%) prices dropped by INR 1,000/t ($11/t) w-o-w to INR 100,000/t ($1,080/t) exw Guwahati, while Bhutan’s prices remaining unchanged at INR 100,000/t ($1,080/t). Subsequently, sellers in both the Indian and Bhutanese markets aligned their offers around the same level, leading to price stability across regions..

- Ferro chrome: High-carbon ferro chrome (HC 60%, Si 4%) prices dipped slightly by INR 1,700/t ($18/t) to INR 119,800/t ($1,294/t) exw Jajpur. Prices declined slightly due to limited buyer inquiries and cautious procurement activity in the domestic market.

- Additionally, Vedanta-Ferro Alloys Corporation Ltd (FACOR) has scheduled an auction for high-carbon (HC) ferro chrome (Cr: 52.5-57% min, 10-150 mm) for 16 March.

Semi-finished steel

- India’s semi-finished steel market witnessed mixed price trends this week, as per BigMint’s assessment. Domestic billet prices declined by INR 50-500/t ($0.5-5/t) w-o-w across most regions. However, southern and western India recorded gains of INR 200-1,000/t ($2-10/t) amid region-specific demand variations. Overall buying interest remained uneven, while moderate bookings and slow offtake in the finished steel segment limited stronger billet procurement throughout the week.

- The sponge iron (DRI) market also reflected varied price movements, with weakening demand exerting pressure on prices. Pan-India sponge iron prices fell by INR 100-1,050/t ($1-11/t) w-o-w across most producing hubs. In contrast, Durgapur and Chennai regions registered a price increase of INR 300-350/t ($3-3.8/t), supported by a slight improvement in bookings at varying price levels. Despite these regional gains, overall market sentiment in sponge iron remained weak, with procurement largely driven by immediate requirements.

- NMDC’s Nagarnar Steel Plant auctioned 15,000 t of steel-grade pig iron on 13 March, with 5,000 t of the offered volume booked at an average INR 36,000/t. Prices decreased by INR 150/t from the 6 March auction, in which the entire volume was sold at INR 36,150/t. The results indicate cautious buying interest amid slightly softer market sentiment.

- On the export front, DRI offers showed an upward trend this week. Export offers to Nepal edged up by $1/t w-o-w to $347/t CPT Raxaul, while offers to Bangladesh increased by $4/t to $355/t CPT Benapole. Notably, a significant surge in export bookings was reported from both Bangladesh and Nepal, supported by rising global scrap prices, which improved the cost competitiveness of Indian-origin sponge iron for overseas buyers.

Finished long steel

- IF-rebar: IF-route rebar prices continued to increase on a w-o-w basis across major markets. Trading activity remained moderate, as traders procured material at varied price levels amid concerns over a potential correction. However, mills largely maintained higher offer levels, supported by elevated raw material costs, particularly sponge iron and billets, amid ongoing geopolitical tensions.

- On a weekly basis, rebar prices surged by INR 100-1,600/t w-o-w across regions and the major hike of INR 1,600/t was seen in Jaipur. However, only in Raipur prices dropped slightly by INR 300/t.

- Trade reference prices of Fe 500 grade rebars manufactured via the IF route (10-25 mm size) were assessed at INR 45,800-46,200/t exw Raipur, INR 51,200-51,800/t exw Jalna.

- Trade reference prices of heavy structural steel for the base size 150 mm channel stood at INR 47,000-47,500/t exw-Raipur.

BF-rebar: Trade-level BF-rebar prices have hit 3-year high levels in March. Continuous price hike in rebar prices by primary mills have led to surge in prices from last 3 months. - Indian primary steelmakers increased rebar prices by INR 500/tonne (t) ($5/t) during this week. Post-revision, list prices stood at INR 58,500-60,000/t ($633-649/t) on landed basis.

- Trade-level BF-rebar prices (distributor to dealer) rose by INR 600/t ($6/t) w-o-w to INR 59,800/t ($647/t) exy-Mumbai, as per BigMint’s assessment on 13 March 2026. Buying activities in the BF-rebar segment have slowed since last week & also there are material availability issues in some sizes, highlighted market participants.

- In the projects segment, prices hovered at around INR 59,000-60,500/t ($639-655/t) FOR basis..

Flat steel

- Trade-level prices of hot-rolled coils (HRC) in India remained firm or increased across key regions, reaching a 28-month high, with HRC prices assessed in the range of INR 53,000-56,200/t ($576-610/t) and cold-rolled coil (CRC) prices assessed at INR 58,100-63,500/t ($632-690/t).

- Indian trade-level HRC prices rose sharply this week as Iran-Israel tensions increased freight and energy costs, triggering panic buying. Tight supply supported prices, though demand remained moderate and liquidity concerns emerged.

- India’s bulk imports of HRCs touched 18,804 t as of 6 March, based on vessel line-up data. Around 114,944 t of additional cargoes are expected by mid-March.

- India’s bulk exports of HRCs touched 36,000 t as of 6 March. Around 25,000 t of additional cargoes are in transit.

- Indian HRC export offers remained absent w-o-w as Iran-Israel-US tensions hurt trade sentiment. Rising freight and insurance costs kept Europe and Middle East trade inactive, with participants adopting a wait-and-watch stance.

Leave a Reply