- Weekly scrap gains persist on tight arrivals

- Semis, finished steel prices jump INR 400-700/t w-o-w

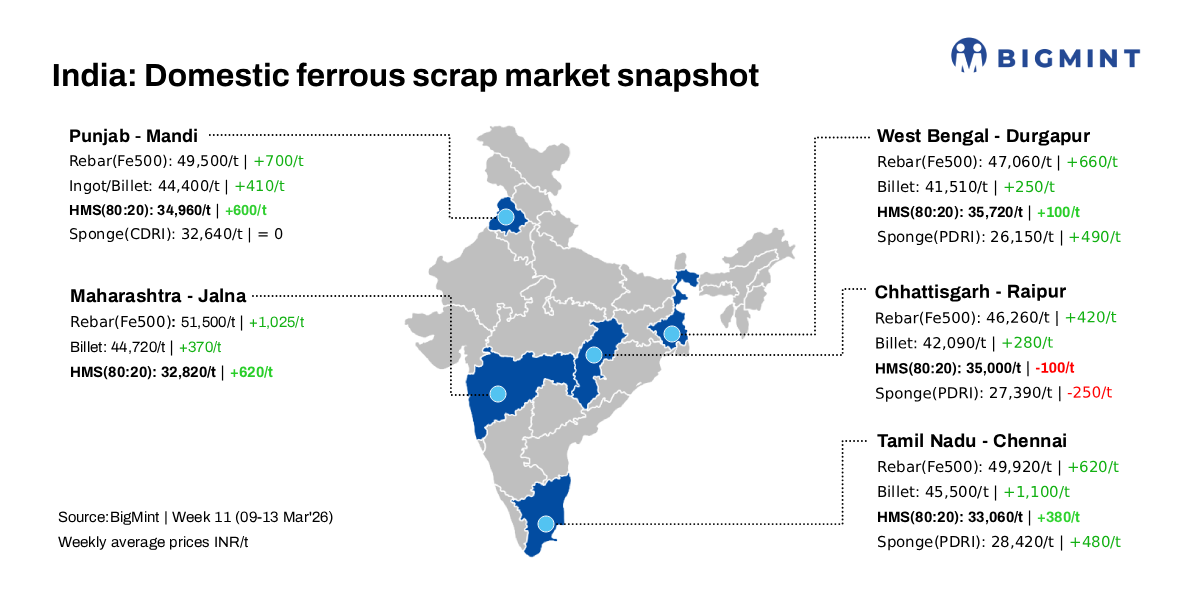

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, fell by INR 200/t d-o-d to INR 37,700/t DAP on 13 March 2026. Despite the daily correction, the index increased by INR 400/t w-o-w, while other scrap grades strengthened by INR 380-600/t over the same period. Market participants attributed today’s correction to muted trading activity in both semi-finished and finished steel segments, prompting scrap suppliers to soften their offers.

Steel prices in Mandi Gobindgarh rose w-o-w on moderate demand and sluggish scrap arrivals, bolstering upward momentum as major steelmakers secured decent scrap volumes.

A mill owner informed, “Geopolitical tensions led to suppliers to Mandi Gobindgarh’s industrial units announcing a 20% supply cut on 9 March, as per central government directives. With 200 rolling mills in Punjab’s steel capital now facing reduced PNG supply and soaring fuel costs, several operations teeter on the brink of closure.”

Another mill owner informed, “The gas crisis and sudden price surge are severely impacting re-rolling mills and steel scrap sellers and are poised to drive steel prices further.”

Alternative raw material prices

Sponge iron (CDRI) prices in Mandi Gobindgarh declined by INR 200/t d-o-d to INR 32,400/t DAP but remained firm w-o-w. Steel-grade pig iron prices in Ludhiana also slipped by INR 200/t to INR 40,000/t DAP, down INR 170/t w-o-w.

Steel market dynamics

In the semi-finished segment, ingot prices in Mandi Gobindgarh fell by INR 200/t d-o-d to INR 44,200/t DAP, though they remained up INR 410/t w-o-w. Rebar (Fe500) prices held steady d-o-d at INR 49,500/t but rose INR 700/t over the week.

Overview of other markets

Mumbai: Rebar (Fe 500) prices on the Mumbai IF route remained stable at around INR 51,500/t ex-works. Buying activity stayed slow to moderate throughout the day, with limited bookings observed. Continuous price correction have kept buyers in a wait-and-watch mode. Meanwhile, mills are attempting to maintain their offers despite slow trading activity. However, due to higher raw material costs, any major correction in prices appears unlikely in the near term.

HMS (80:20) scrap was assessed at INR 33,950/t DAP, with the scrap-billet conversion spread hovering around INR 11,050/t.

Durgapur: Market assessments from Durgapur indicated marginal corrections across steel and scrap prices. Billet prices eased by INR 250/t to INR 41,300/t, while rebar prices declined by INR 200/t to INR 47,000/t. Meanwhile, HMS (80:20) scrap prices slipped by INR 100/t to INR 35,600/t. Trading activity in finished steel remained slow during today’s session. Although a mild scrap shortage persists due to LPG supply constraints, sellers are holding back material expecting a near-term improvement in steel prices.

Upcoming scrap auctions

Price highlights

End-cutting to billet spread: In Mandi, the spread between end-cutting scrap and billets stood in the range of INR 6,300-6,600/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were assessed at $362-$365/t, approximately INR 35,913/t (inclusive of freight). HMS (80:20) prices in Mumbai remained stable d-o-d at INR 34,000/t DAP. Indicative prices of shredded from Europe stood at $382-$385/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 14,950/t.

To provide feedback on this index or if you would like to contribute by becoming a data partner, please contact – support@bigmint.co

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

Leave a Reply