- Export licensing and trade barriers pressure steel exports

- Middle East tensions disrupt trade flows, exports face uncertainty

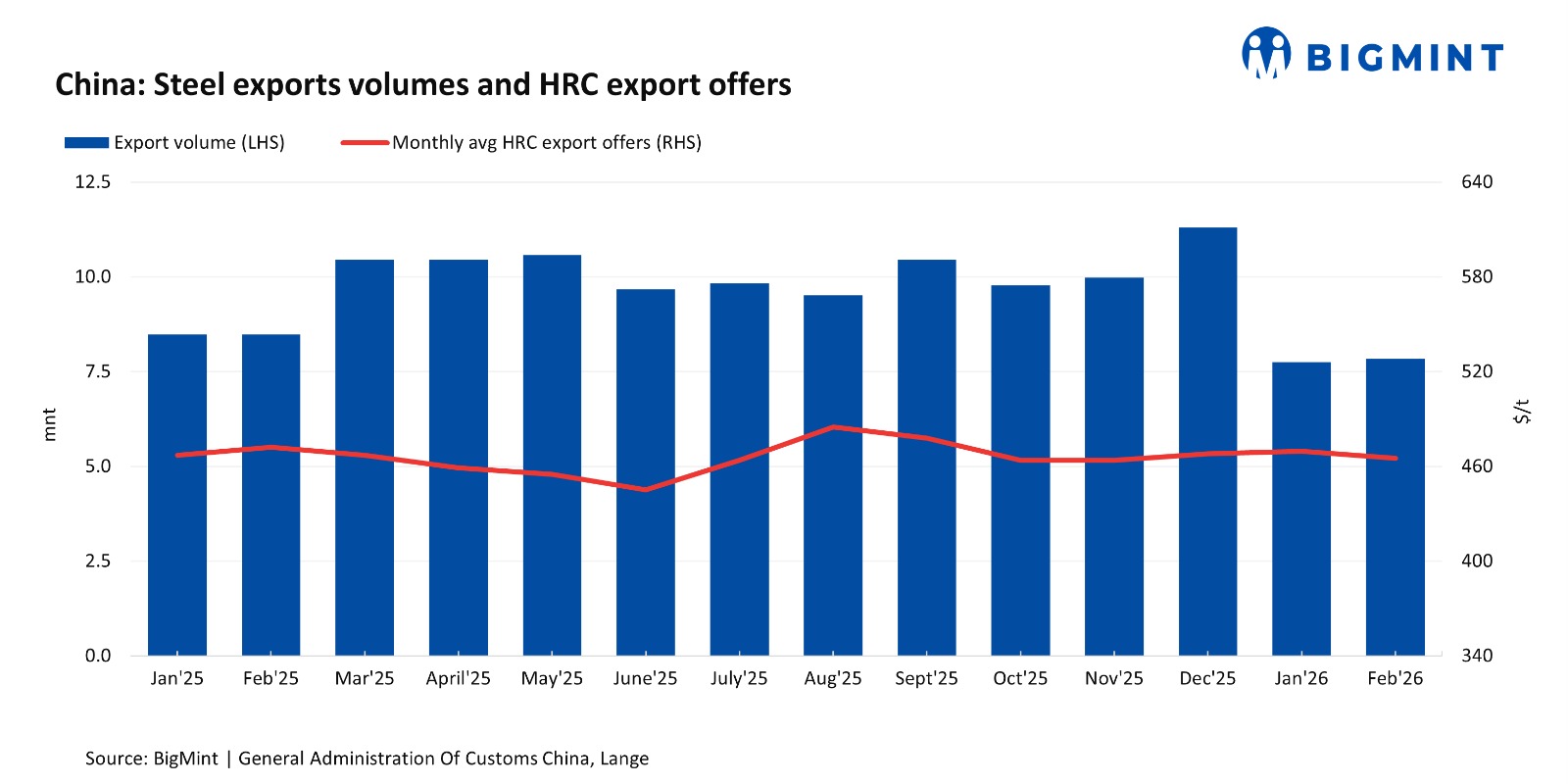

China’s steel exports declined by 8.1% y-o-y to 15.59 million tonnes (mnt) in January-February 2026, according to data from the General Administration of Customs.

Exports in January alone fell by 13.2% y-o-y to 7.75 mnt, while in February 2026, shipments stood at around 7.84 mnt, slightly higher than January on a monthly basis but 2.5% lower y-o-y compared with the same period last year.

Factors influencing China’s steel exports

Export licensing rules weigh on shipments: The implementation of the export licensing system from January 2026 have weighed on shipments during the first two months of the year. Under the new policy, exporters are required to obtain export licences and manufacturer quality certificates, covering around 300 steel products prior to shipment, adding additional administrative and compliance requirements. These procedures likely slowed export activity during the initial phase of implementation, though the impact may ease gradually as exporters adjust to the new system.

Rising trade barriers add pressure: A growing number of anti-dumping duties and trade protection measures against Chinese steel may have also weighed on the export volumes. Countries including Vietnam, Malaysia, India, South Korea and Brazil had imposed trade protectionist measures on certain steel imports from China in recent times to protect their domestic industry from cheap imports. For instance, Vietnam imposed anti-dumping duties in July 2025 on HRC imports from China with specific thickness and width specifications, following which steel imports from China declined by around 1 mnt y-o-y to 8.49 mnt in July-December 2025, compared with 9.49 mnt in the same period of 2024.

Outlook

China’s steel exports may remain under pressure in the near term amid ongoing geopolitical tensions in the Middle East and disruptions to key maritime routes. The region typically absorbs around 25-30 mnt of Chinese steel annually, making it a key export destination. If disruptions persist, Chinese mills may redirect part of their shipments to alternative markets such as Southeast Asia.

However, persistently weak domestic steel demand in China is likely to keep mills actively seeking overseas markets for surplus supply, supported by competitive export offers. At the same time, higher freight costs, longer transit times and regulatory hurdles could keep shipment trends volatile in the near term.

Leave a Reply