- Aluminium hits four-year high on supply disruptions

- Qatalum shutdown sparks surge in aluminium prices

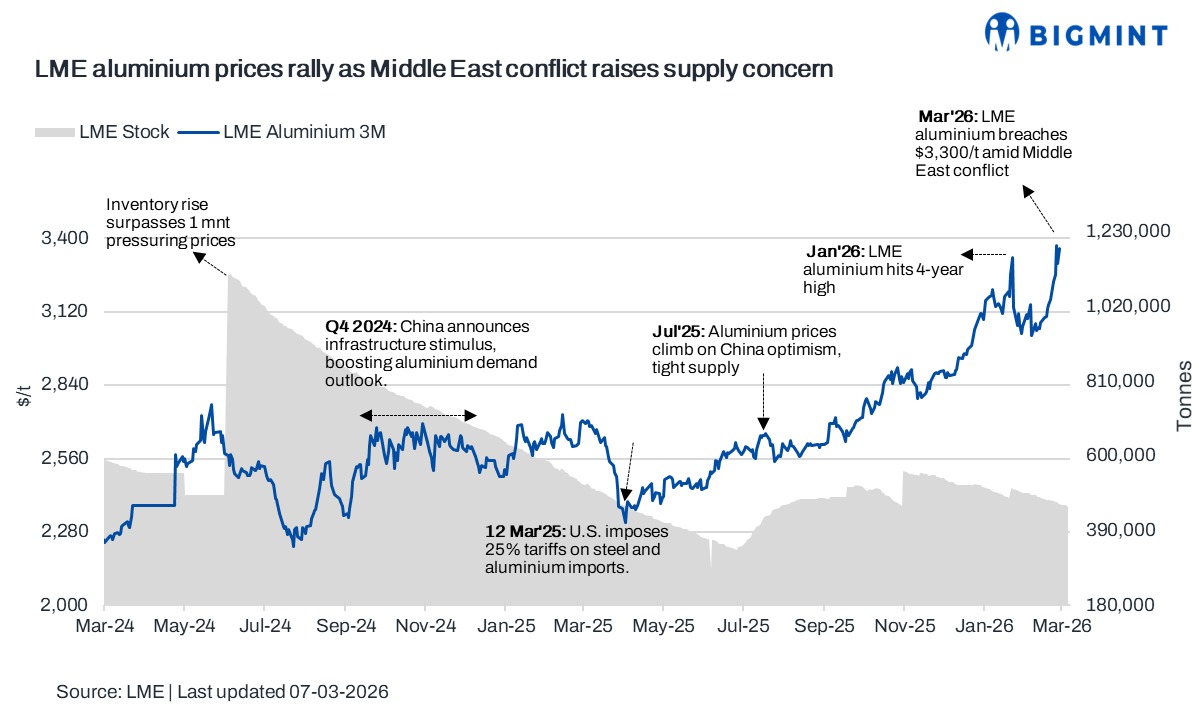

Benchmark aluminium prices on the LME rose 4% in the week ended 6 March 2026, supported by escalating geopolitical tensions and supply-chain disruptions that heightened concerns over global aluminium availability.

Pricing, inventory trends

LME aluminium averaged $3,306/t during the week, rising $129/t or 4% w-o-w. Prices opened the week near $3,233/t, strengthened to $3,372/t mid-week, and settled at $3,362/t by the close.

Meanwhile, LME aluminium inventories declined 1.4% w-o-w to 456,875 t, down from 463,550 t, highlighting tightening visible supply and reinforcing the supportive tone in the aluminium market.

Factors impacting prices

LME aluminium prices rallied sharply last week, averaging around $3,306/t, up $129/t or 4% w-o-w, and briefly touching a nearly four-year high above $3,400/t amid escalating geopolitical tensions and tightening global supply. The surge was primarily triggered by the shutdown of Qatar’s Qatalum smelter, a joint venture between QatarEnergy and Norsk Hydro, after its gas supplier suspended natural gas deliveries following attacks linked to the ongoing Middle East conflict. The shutdown forced the company to halt aluminium and other downstream production, tightening supply expectations in the global market.

The disruption comes at a time when the Middle East plays a crucial role in global aluminium supply, accounting for roughly 8% of global output. Supply risks intensified further after Aluminium Bahrain (Alba) declared force majeure and halted shipments due to shipping disruptions in the Strait of Hormuz, a critical trade route for metals and raw materials. Concerns that the conflict could disrupt shipments or production across the Gulf region have heightened fears of a supply crunch, driving aluminium prices to multi-year highs.

The price rally has been amplified by already tight global inventories and limited supply flexibility outside China. Stockpiles are near multi-year lows, while China’s production growth remains constrained by capacity caps and rising domestic demand. With the Middle East disruptions threatening a key source of supply and alternative production unable to ramp up quickly due to high energy costs, analysts expect continued volatility in aluminium markets in the near term.

Outlook

Aluminium prices are likely to remain firm in the near term as Middle East tensions continue to embed a supply-risk premium and LME inventories trend lower, with stocks falling 1.4% w-o-w. Ongoing disruptions, including the shutdown of Qatar’s Qatalum smelter and shipping uncertainties around the Strait of Hormuz, could keep supply tight and sustain prices near recent multi-year highs. However, any easing in geopolitical tensions or improvement in regional logistics may cap further sharp gains, with market participants closely monitoring inventory trends and developments in Gulf shipping routes.

Leave a Reply