- Firm import parity supporting coke prices

- Weak demand, softer coal prices weighing on sentiment

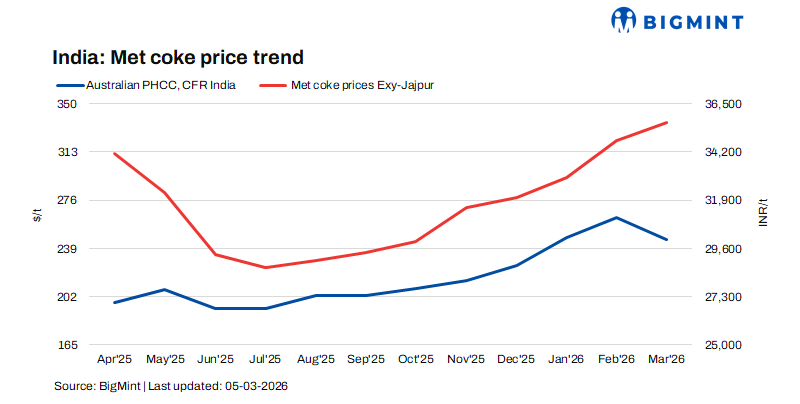

Indian blast furnace (BF)-grade metallurgical coke prices recorded a marginal w-o-w increase on 3 March 2026, supported by balanced domestic demand-supply dynamics and firm import parity levels, despite a mild correction in upstream raw material costs.

As per BigMint’s assessment, in eastern India, BF-grade coke (25-90 mm) prices rose by INR 600/t week-on-week to INR 35,600/t ex-Jajpur. A spot trade of 22,500 t was concluded at INR 36,000/t, indicating continued but selective buying activity, The prices in western India remained stable at INR 30,500/t ex-Gandhidham.

Meanwhile, foundry-grade coke (+90 mm) prices held steady at INR 36,100/t ex-Rajkot, reflecting stable demand from the casting and foundry sector and a generally balanced market without aggressive restocking or supply pressure.

Import parity and raw material dynamics

Firm import parity continued to underpin domestic coke prices. Indonesian-origin BF coke (65/63) was indicated at $270-275/t CFR India, translating to a landed cost of around INR 34,000-34,500/t, which effectively provided a pricing floor for domestic suppliers.

However, market participants reported bids heard lower by around $10/t, suggesting some resistance from buyers. Upstream, Australian premium hard coking coal prices declined sharply by $20/t w-o-w to $221/t FOB, which slightly eased cost pressures for coke producers.

Global market signals

External market developments also warrant attention. China’s coke market is expected to soften in the near term after several steel mills in Tianjin and Hebei initiated the first round of coke price cuts of RMB 50-55/t, following a similar reduction in domestic coking coal prices. The move reflects ample raw material supply, weak trading activity, rising inventories at coking plants, and a slow recovery in steel production, factors that could indirectly influence sentiment in regional coke markets.

Downstream demand indicators

Downstream indicators in India also point to cautious buying sentiment. NMDC Limited’s Nagarnar Steel Plant recorded weaker results in its 27 February pig iron auction, with 7,000 t sold at an average INR 36,000/t, down INR 500/t from the previous auction, while 5,000 t remained unsold out of the 12,000 t offered, reflecting selective procurement. However, some support was visible in the spot market as steel-grade pig iron prices in Durgapur increased w-o-w to INR 38,000/t ex-works, according to BigMint assessments.

Outlook

Next week, domestic BF-grade coke prices are expected to remain broadly stable, supported by firm import parity and steady steel production. However, softer global coking coal prices, potential Chinese coke price cuts, weak downstream demand, and ongoing United States-Iran tensions may pose downside risks to market sentiment.

Leave a Reply