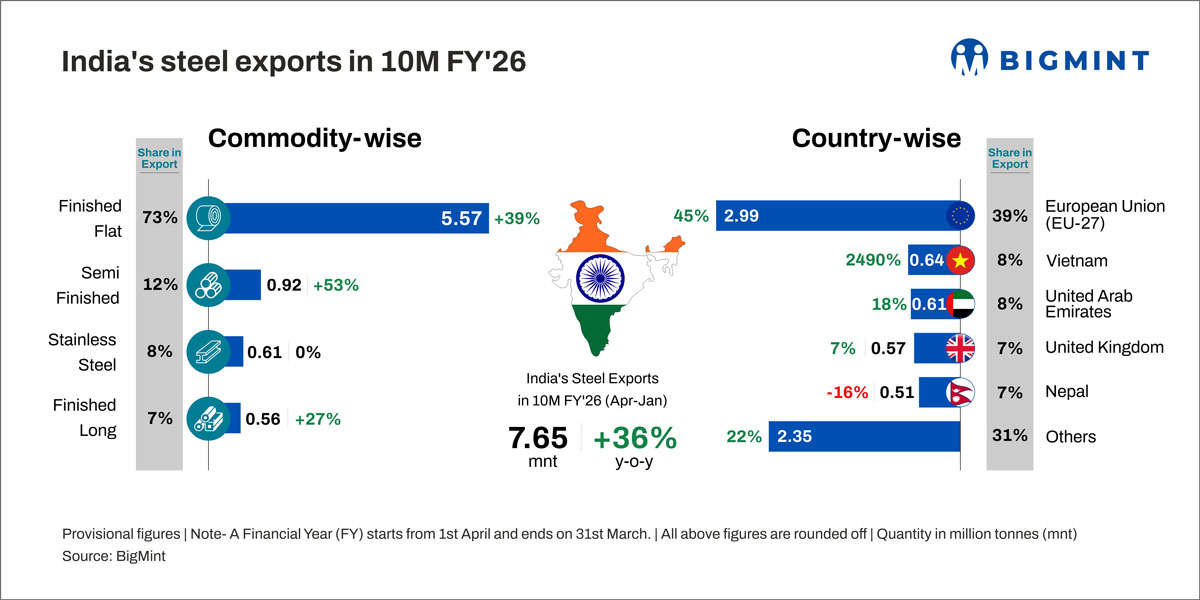

- EU sentiment weakens amid carbon costs, regulatory uncertainty

- Geopolitical tensions halt Middle East trade, inflate freight costs

BigMint’s Indian HRC (S275) export index for the European Union (EU) remained unchanged w-o-w at around $570/t FOB main port as of 3 March amid weak demand. Meanwhile, in the Middle East, no firm offers from India were heard due to the ongoing geopolitical tensions in the region.

1. HRC offers to the EU: Indian HRC export offers to the EU remained unchanged w-o-w at $620/t CFR Antwerp, as demand for imported material remained subdued. European buyers maintained a cautious stance amid uncertainty over the potential cost implications under the European Union’s Carbon Border Adjustment Mechanism (CBAM) and the anticipated replacement of the existing safeguard measures, which have further dampened market sentiment.

On the domestic front, European HRC prices continued to edge higher, driven primarily by supply-side constraints. Extended mill lead times and limited import competition tightened spot availability, allowing regional producers to gradually push through price increases despite muted demand fundamentals. With fewer competitively priced overseas offers available, buyers had limited sourcing alternatives, strengthening mills’ pricing power. However, acceptance of higher prices remained slow, underscoring that the recent uptrend is supply-led rather than demand-driven.

2. HRC offers to the Middle East: Indian HRC export offers to the Middle East remained absent this week, with no firm offers heard amid the ongoing Iran-Israel-US conflict. Escalating geopolitical tensions prompted market participants to adopt a cautious wait-and-watch approach, leading them to withhold fresh offers. Concerns over a sharp rise in freight rates and war-risk insurance premiums, which are expected to significantly increase shipment costs, have further dampened the market sentiment, keeping overall trading activity largely at a standstill.

A Middle East-based BigMint source indicated that “the Strait of Hormuz remains the only entry route for vessels into the Gulf Cooperation Council (GCC) region, and it is currently under threat of closure. With tensions escalating, shipping lines are expected to impose war-risk surcharges, raising freight costs and placing additional strain on regional trade flows.”

Similarly, no firm Chinese HRC export offers to the Middle East were heard, with suppliers refraining from issuing fresh offers amid the prevailing uncertainty and lack of visibility on near-term developments. The last heard Chinese HRC export offers to the Middle East were around $500/t CFR UAE. Meanwhile, May 2026 HRC contracts on the Shanghai Futures Exchange (SHFE) increased by RMB 14/t ($2/t) w-o-w to RMB 3,212/t ($466/t) on 3 March from RMB 3,198/t ($464/t) on 24 February 2026.

Outlook

The Indian HRC export market is expected to remain highly volatile and cautious in the coming week amid persistent global uncertainties. In the EU, buyers continue to defer purchases amid uncertainty over the potential cost impact under CBAM and the implementation of new safeguard measures. Meanwhile, the Iran-Israel-US conflict is likely to keep trade activity in the Middle East muted until geopolitical conditions stabilise and greater clarity emerges.

Leave a Reply