- Chennai scrap up w-o-w, steel shows mixed cues

- Imported offers firm, mills prefer alternate origins

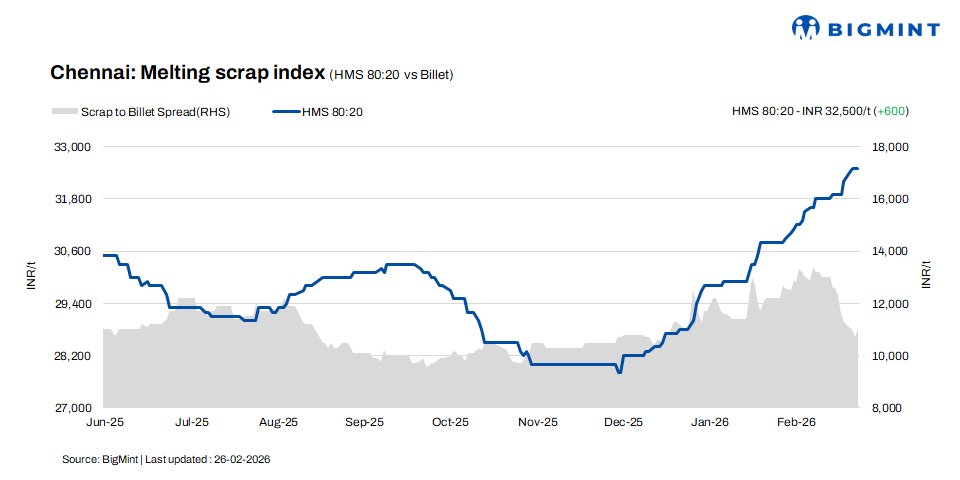

In the Chennai market, HMS (80:20) scrap prices rose by INR 600/t on a w-o-w basis to INR 32,500/t on 26 February 2026, driven by steady buying activity, while prices remained flat on a daily basis, according to BigMint assessment.

Meanwhile, billet prices declined by INR 700/t w-o-w, but registered a daily increase of INR 300/t, settling at INR 43,500/t. Rebar prices fell by INR 500/t w-o-w to INR 48,200/t, while remaining stable on a d-o-d basis. The market sentiment remained mixed, reflecting cautious trade amid limited weekly movements.

Imported and domestic price trends

Market participants reported that Australia-origin imported shredded scrap was offered at $365-370/t CFR Chennai, while HMS (80:20) scrap was quoted at $342-345/t CFR. However, buyers were bidding $5-10/t lower than prevailing offers. Buying interest remained limited as mills found current offers firm and instead focused on alternative origins such as Malaysia, Singapore, Hong Kong, and Thailand, where lower-priced and readily available loaded cargoes were being preferred.

In the domestic market, HMS (80:20) scrap prices were assessed at INR 32,500-33,000/t for immediate payment, while transactions on extended credit terms were concluded at higher levels of INR 33,000-33,500/t. Overall market sentiment remained stable, supported by steady liquidity conditions. Both buyers and sellers adopted a cautious trading approach, balancing procurement volumes with payment terms and financing availability.

Buyer-supplier sentiments

A mill representative noted that buying interest in sponge iron remained weak, as buyers expect further price correction in the near term. However, following a weekly decline in billet prices, buyers have resumed bookings from the merchant market, leading to an improvement in demand in recent sessions. Meanwhile, rebar demand from the project segment remained healthy, while retail demand continued to be sluggish.

A scrap supplier indicated that HMS (80:20) prices were currently hovering in the range of INR 32,500-33,500/t, with variations largely dependent on payment terms and mill-specific volume requirements. The market is witnessing a mild supply tightness, primarily due to limited imported scrap bookings over the past few months.

Higher import offers compared to domestic prices, coupled with the strengthening dollar, have discouraged overseas procurement, thereby tightening scrap availability in the domestic market.

Regional comparison

In the western India based Jalna market, billet prices declined by INR 400/t to INR 42,000/t, while rebar prices fell by INR 300/t to INR 48,300/t. Meanwhile, HMS (80:20) scrap prices edged up by INR 100/t to INR 31,900/t.

Trade activity in the finished steel segment remained subdued amid moderate demand conditions. According to market participants, rebar inventory levels at mills are estimated at around 10-15 days. However, due to tight scrap availability, suppliers are reluctant to offer material at lower levels, thereby limiting further downside in scrap prices.

Outlook

HMS (80:20) scrap prices in Chennai are likely to remain range-bound with a firm bias in the near term. While finished steel prices have corrected on a weekly basis, steady mill buying continues to support scrap prices. Price movements are expected to remain restricted within INR +/- 200-500/t.

Leave a Reply