- Russian mills keep prices firm amid limited sales pressure

- Strong rebar sales lift UAE billet demand, but supply tight

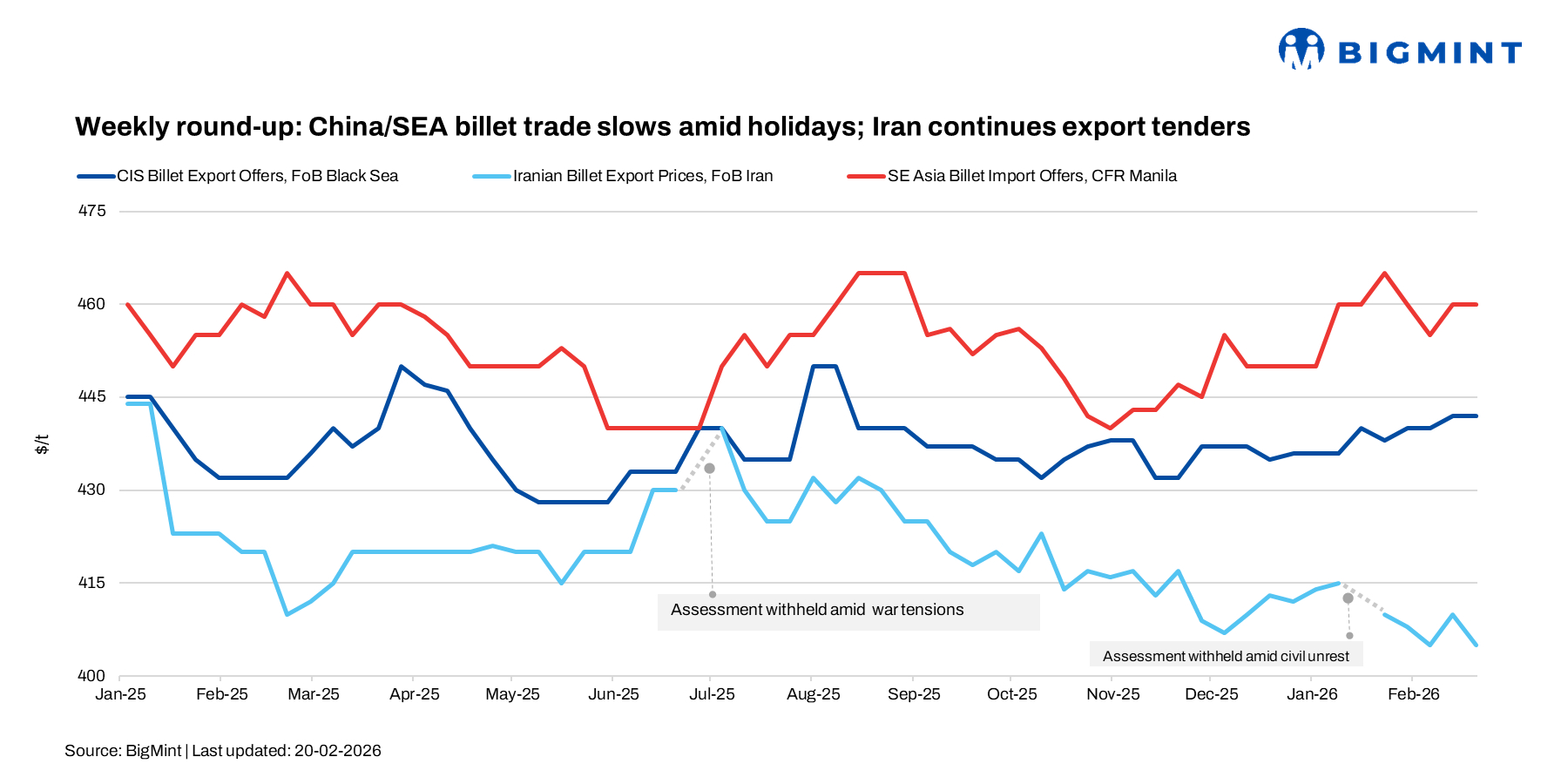

Major billet markets remained largely stable in the week ended 20 February 2026, with trading activity slowing across Asia, the Black Sea, and the Middle East due to the Lunar New Year holidays, Ramadan-related demand softness, and cautious re-roller procurement. Meanwhile, Iran continued export sales even as geopolitical tensions escalated.

Overall sentiment stayed subdued, with limited fresh bookings and participants awaiting clearer demand signals before taking positions.

In Turkiye, deep-sea scrap prices were broadly stable, with US-origin HMS 80:20 at $375-376/t CFR and EU/Baltic material at $372-374/t CFR. Weak rebar demand and maintenance outages kept mills cautious, restricting billet buying despite tight winter scrap supply. Sentiment remained muted, with only limited deep-sea bookings reported.

Chinese, Southeast Asian market

Southeast Asia’s billet import market remained largely inactive this week due to the Lunar New Year holidays across China and several regional countries, which kept both suppliers and buyers out of the market.

“The Asian and Chinese billet markets remained effectively closed during the Lunar New Year holidays, with limited offers and negligible buying interest. Meaningful price movement is expected only after full trading activity resumes next week,” said a major Southeast Asia-based billet trader.

China-origin 5sp billet was heard at around $460-465/t CFR Southeast Asia, stable w-o-w, while buying interest remained negligible as most importers preferred to wait for Chinese mills to fully resume operations. Weak construction demand across the region, particularly in the Philippines, continued to weigh on sentiment.

Elevated Chinese inventories, with Tangshan billet stocks reaching 1.8 mnt by mid-February, may exert downward pressure once trading normalises.

Black Sea & CIS market

Black Sea square billet offers remained largely unchanged w-o-w, while trading activity slowed amid the onset of Ramadan in key destinations and approaching holidays in Russia.

Russian suppliers maintained April-shipment offers at $445-447/t FOB Black Sea, compared with $445-448/t a week earlier. Mills refrained from reducing prices, supported by rouble fluctuations and limited spot sales pressure. Material from the Donbas region was available at $440-443/t FOB Novorossiysk, steady w-o-w.

CIS billet offers to Turkiye were heard at $465-470/t CFR ($445-450/t FOB). However, buyers’ workable levels remained lower at $450-455/t CFR, referencing scrap prices around $372-375/t CFR. In the Far East, Russian semis were indicated at around $422-425/t FOB, with limited fresh transactions reported.

With stable offer levels and subdued booking activity, CIS exported billets were assessed at $442/t FOB.

Iran: Iran’s billet export prices were at $405/t FOB, down by $5/t over the week. A 4,000-t prompt cargo was concluded at $407/t FOB; however, the deal was not viewed as a benchmark due to its limited tonnage and immediate shipment terms. Khouzestan Steel Company also reportedly sold 50,000 t of billet at $405/t FOB, supporting the prevailing market prices. Slab export prices were unchanged at $425/t FOB, while rebar export prices held steady at $375-380/t exw amid measured booking activity.

Heightened geopolitical tensions between Tehran and Washington, alongside continued uncertainty surrounding Iran’s nuclear programme, kept overseas buyers cautious. Although producers continued to float export tenders, most customers adopted a wait-and-watch approach.

Currency fluctuations remained limited and had no material impact on trade, while the secondary market rate for exporters was around 136,000 toman per dollar. Overall export activity remained subdued, but price levels were firm.

UAE: Strong rebar sales in the UAE lifted billet requirements, while prompt supply remained constrained. Domestic and GCC mills currently lack immediate availability, prompting re-rollers to increasingly rely on traders for spot and short-notice cargoes.

“EMSteel is expected to announce its rebar prices on Monday, with a decision likely between a price hike or a rollover,” said a major UAE-based steelmaker source.

Asian Emirates Conformity Assessment Scheme (ECAS)-certified billet was assessed at $475-485/t CFR, broadly stable, with minor variations depending on origin and shipment size. Although more suppliers have secured ECAS approval, delivery schedules remain uncertain.

Market sources reported tightness in semi-finished supply, with rebar backlogs adding further pressure on billet demand and sustaining firm price sentiment.

Outlook

Outlook

BigMint believes billet prices will remain largely stable, with trading activity gradually improving as the holiday slowdowns ease. However, support may emerge from tight prompt supply in select regions, while scrap-linked markets will continue to track rebar demand and mill margins closely.

Leave a Reply