- Around 3.5 mnt of iron ore booked in OMC auction

- Buyers expect correction in iron ore prices in near term

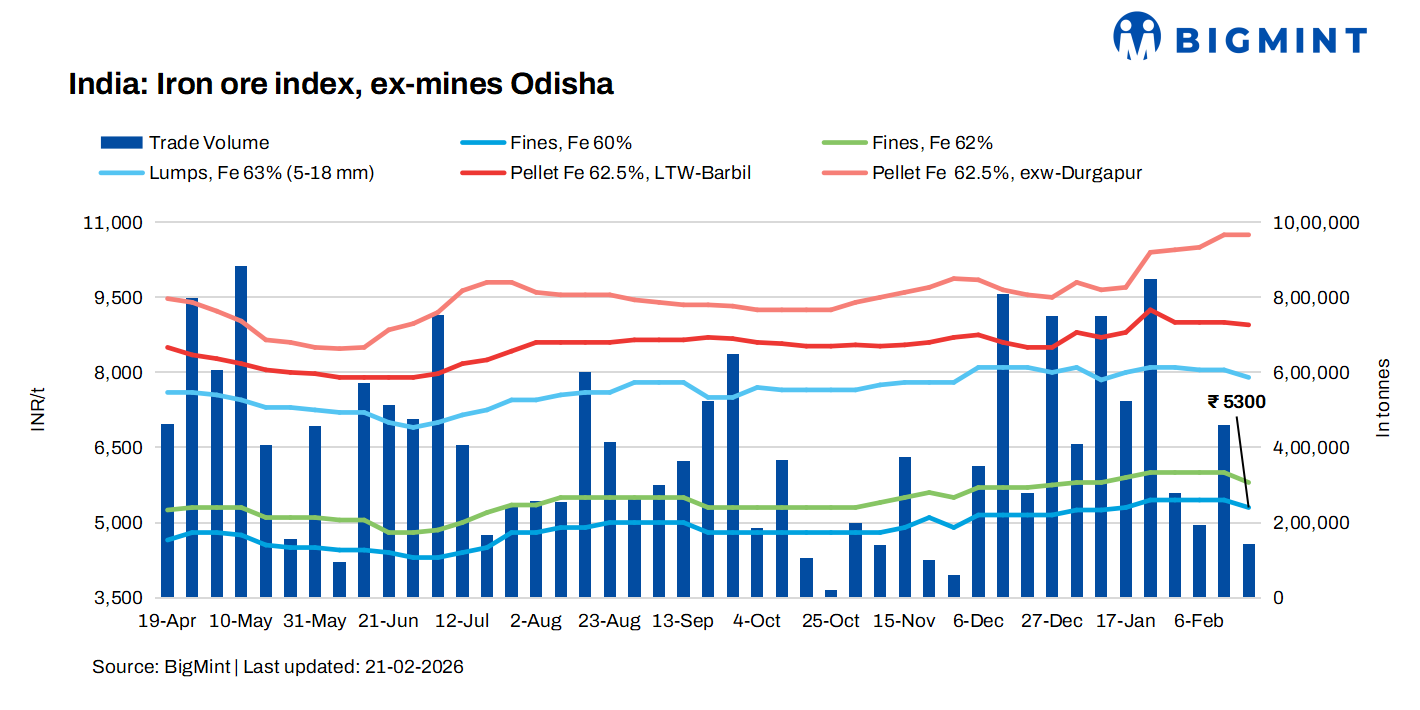

Iron ore prices in Odisha witnessed fluctuations of around INR 100-250/t this week, as assessed on 21 February, largely tracking the bids in the latest auctions conducted by Odisha Mining Corporation (OMC). Market sentiment remained cautious as auction prices trended lower compared to last month, pulling down expectations in the spot market.

Price update

BigMint’s Odisha iron ore fines (Fe 62%) index dropped by INR 200/t w-o-w to INR 5,800/t ($64/t) ex-mines on Saturday. BigMint recorded deals for around 140,000 t this week, concluded directly by steelmakers.

In OMC’s iron ore fines auction for 2.25 mnt (Fe 51-62%) on 19 February, around 1.97 mnt (88%) were booked at INR 4450-6,300/t. Few lots received premiums of INR 350-950/t over base prices, with INR 350/t being the average premium. However, bids (weighted average) fell by INR 100/t m-o-m. Fines base prices were raised by INR 150-350/t m-o-m.

In 1.58 mnt of iron ore lumps (Fe 60-65%) auction, around 1.574 mnt (99%) were booked at INR 5,850-7,350/t, with premiums of INR 150-900/t. Weighted average bids fell by INR 150/t m-o-m. Earlier, OMC had raised the base prices of lumps by INR 100-300/t.

Market highlights

According to buyers, iron ore prices had reached a peak in recent weeks, making procurement less viable for sponge iron and steel producers. A steelmaker said, “The correction in OMC auction bids reflects the actual ground demand. We expect some more softening in prices as finished steel and semi-finished segments are already under pressure.” Sponge iron and billet prices have declined in recent weeks, which has directly impacted raw material buying appetite.

Meanwhile, miners are currently in discussion over fresh offers following the OMC auction and are expected to announce revised prices in the next couple of days. A private miner informed that availability is limited, as their Environmental Clearance (EC) is nearing final extraction limits. He added, “We have only a few lots left. Despite the drop in OMC prices, we are trying to maintain stability in our offers due to constrained supply.”

On the demand side, buyers have largely secured bulk raw material through the recent OMC auction, while additional requirements are being fulfilled on a need-based basis from private miners. Market participants believe a clearer direction in iron ore pricing will emerge once fresh offers are announced by miners in the coming days.

Overall, the market remains in a wait-and-watch mode, with both buyers and sellers closely monitoring auction trends and downstream steel price movements for further cues.

Factors affecting iron ore prices

Pellet prices firm w-o-w: Pellet (6-20 mm, Fe 62.5%) prices in Odisha’s Barbil inched down by INR 50/t w-o-w to INR 8,950/t ($98/t) loaded to wagon on 20 February. Pellet (Fe 62.5%, 6-20 mm) prices in Durgapur remained stable at INR 10,750/t ($119/t) exw.

Sponge iron prices down w-o-w: According to BigMint’s assessment, sponge iron C-DRI (FeM 80%) prices in Rourkela fell by INR 300/t ($3/t) w-o-w to INR 27,00/t ($299/t) on 21 February.

Billet prices fall w-o-w: Meanwhile, steel billet (100*100 mm) prices in Rourkela declined by INR 700/t ($2/t) w-o-w to INR 40,000/t ($441/t) on 21 February.

Rationale

- T1- Six (6) deals for Fe 62% fines were recorded in the publishing window, and five (5) were considered for price computation. These were given 50% weightage for index calculation.

- T2 – BigMint received seventeen (17) offers and indicative prices under the T2 category (offers, indicative, and bids) in this publishing window. Fifteen (15) were taken into consideration and given 50% weightage. To check BigMint’s iron ore assessment, pricing methodology, and specification document, click here.

Outlook

Iron ore price trends in Odisha are expected to be become clear over the next couple of days, with new offers being announced by miners. According to our analysis, the new prices are likely to be lower than current levels, even with limited material availability due to pressure from the downstream steel sector.

Leave a Reply