- Chinese holiday slowdown keeps Capesize sentiment cautious

- Long-haul flows, tighter vessel supply support Atlantic rates

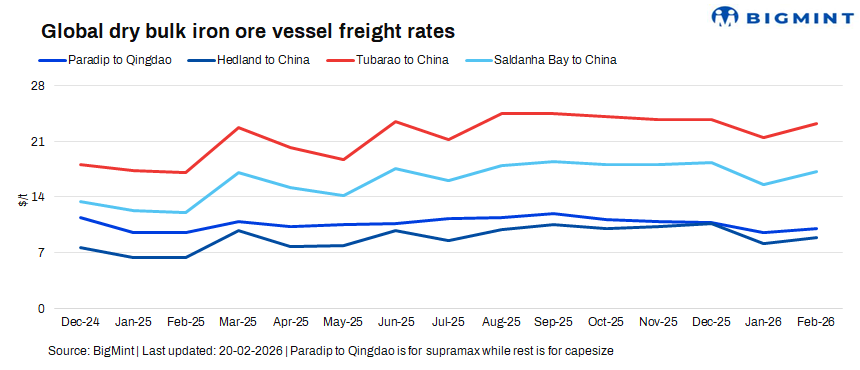

Dry bulk iron ore freight markets showed mixed trends w-o-w on 20 February 2026, as the Chinese New Year holiday period began, leading to thinner trading activity and cautious sentiment in the Capesize segment. Pacific freights exhibited divergent trends w-o-w, while Atlantic rates stayed supported. A seasonal slowdown and limited fresh enquiries kept overall fundamentals under pressure, despite mixed regional trends.

India-China sentiment remained bearish on muted exports and ample tonnage, while Australia-China reflected a firm undertone on steady miner-led activity. Meanwhile, Brazil-China and South Africa-China routes maintained a moderately positive sentiment, supported by long-haul cargo flow and relatively tighter Atlantic vessel supply, despite fragile broader momentum.

“Vessel hire rates across most of the Indian Ocean and Pacific regions are showing signs of a pick-up, with sentiment turning firmer. Rates are expected to improve further next week as Chinese market participants return post-holiday, potentially boosting fixture activity and freight momentum,” a source informed BigMint.

Route-wise updates

Market highlights

- Brent crude oil futures surge w-o-w: Brent crude oil futures gained around $4.04/barrel (bbl) w-o-w to $70.95/bbl for the May 2026 contract on 20 February, supported by renewed geopolitical tensions, expectations of tighter global supply, and improved demand outlook from major consuming economies.

- DCE iron ore futures steady w-o-w: Iron ore futures on the Dalian Commodity Exchange held largely stable w-o-w at RMB 746/t ($108/t) on 20 February, reflecting balanced market sentiment.

- Baltic index declines w-o-w: The Baltic Dry Index fell by 76 points w-o-w to 2,019 on 19 February, pressured by weaker Capesize earnings. The Capesize index dropped 240 points to 3,001, while the Supramax index eased 5 points to 1,160.

Enquiries understood fixed (13-19 Feb’26)

Outlook

Freights are expected to see a gradual improvement as Chinese participants return post-holiday, potentially lifting fixture activity in the Pacific. However, gains may remain limited unless fresh long-haul cargoes from Brazil and South Africa pick up, as ample vessel availability continues to cap upside. Overall sentiment remains cautiously balanced, with near-term direction hinging on post-holiday restocking and tonnage absorption.

Leave a Reply