- Inventory draws extend for fifth week, tightening visible supply

- Concentrate tightness continues to cap smelter margins

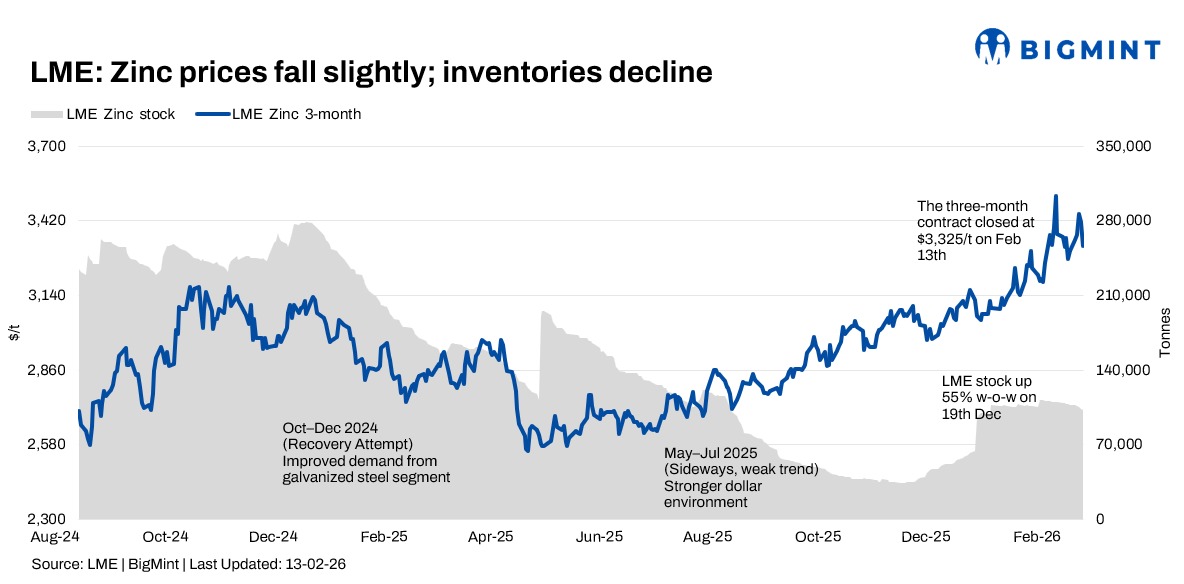

London Metal Exchange (LME) zinc prices ended lower in the week ended 13 February, as late-week profit-taking offset strong mid-week gains. While macro cues remained mixed, continued inventory draws and ongoing concentrate tightness provided underlying support.

Price trends

LME zinc cash prices opened the week at $3,325/t on 9 February and rallied to a weekly high of $3,437/t on 11 February, supported by firm buying across the non-ferrous complex. However, prices retreated in the final sessions, settling at $3,295/t on 13 February, down around 0.9% w-o-w.

The three-month contract followed a similar trajectory, rising to $3,447/t mid-week before easing to $3,325/t at close, marking a 0.7% w-o-w decline. The market once again struggled to sustain gains above the $3,400/t level, with resistance emerging near recent highs.

Inventory analysis

LME zinc inventories declined for a fifth consecutive week, reinforcing signs of tightening spot availability. Stocks fell from 106,925 t on 9 February to 102,225 t on 13 February, marking a weekly draw of 4,700 t, down 4.4% w-o-w.

Notably, the sharpest decline occurred on 11-12 February, when inventories dropped below the 105,000 t mark. The steady pace of withdrawals suggests firm physical offtake, even as futures prices struggled to hold higher levels.

Market participants indicated that while visible stocks are thinning, downstream buying remains measured, with consumers largely adhering to need-based procurement.

MCX zinc trends (9-13 Feb)

On the MCX, zinc futures traded in a relatively volatile but narrow band, tracking mixed global cues. The active March 2026 contract moved within a range of INR 323,650-335,550/t during the week. Prices opened at INR 328,600/t on 9 February and settled slightly lower at INR 327,200/t on 13 February, down 0.4% w-o-w. Volume peaked on 12 February alongside intraday volatility, suggesting active participation before mild profit-booking emerged into the weekend.

Domestic availability remained comfortable, with galvanising demand described as steady but not aggressive.

SHFE zinc trend

The SHFE zinc contract, assessed in dollar terms, displayed relative resilience compared with LME. Prices opened the week around $3,517/t (RMB 24,299/t) and closed higher at $3,559/t (RMB 24,589/t) on 13 February, reflecting a modest weekly gain.

The relative firmness in SHFE compared with LME suggests continued domestic support in China’s physical market. However, smelter margins remain constrained amid low treatment charges (TCs), signalling persistent concentrate tightness despite stable refined output.

Outlook

We expect persistent inventory draws and concentrate tightness continue to underpin the market, but upside momentum appears capped near the $3,400/t resistance zone. Absent fresh supply disruptions or a decisive improvement in macro sentiment, prices may continue to oscillate within recent ranges. Market participants are expected to maintain cautious, hand-to-mouth buying strategies amid ongoing volatility.

Leave a Reply