- Australia, South Africa drag exports despite Colombia rebound

- Firm freights support rates, but fixing remains muted

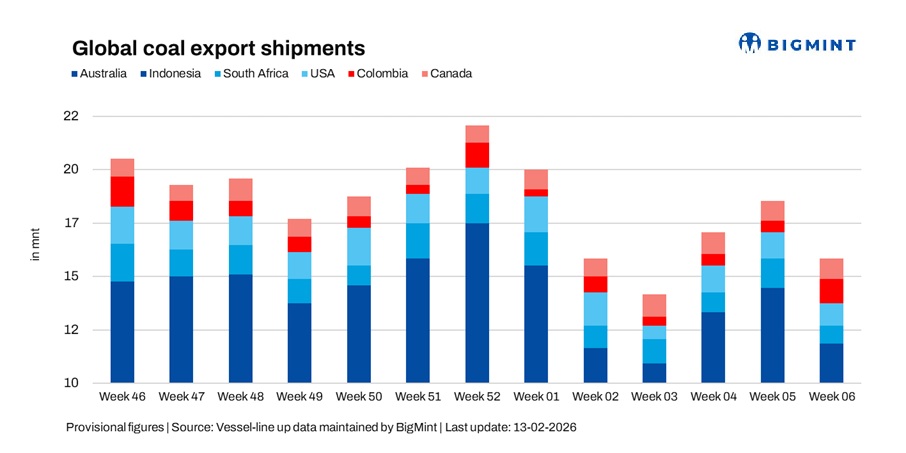

Global seaborne coal exports declined by around 14.4% w-o-w to 15.56 mnt in the week ended 6 February, from 18.18 mnt in the previous week, hitting two-week low, as per vessel line-up data. The fall was driven by weaker cargo execution and reduced scheduled loadings, led by sharp declines in exports from Australia, South Africa, Indonesia, and the US, which outweighed a strong rebound in Colombian shipments.

Export activity remained largely schedule-driven, with fewer confirmed loadings reflecting cautious buying sentiment and softer demand visibility across key Asian markets, indicating that last week’s rebound momentum was not sustained.

Country-wise trends

Australian coal exports fall sharply

Australia’s coal exports declined 24.1% w-o-w to 5.53 mnt in week 06, from 7.29 mnt in week 05, reflecting weaker cargo execution and a slowdown in weekly loading programmes. Shipment activity was led by Newcastle (2.03 mnt), followed by DBCT (1.20 mnt) and Gladstone (1.03 mnt).

On the supply side, BHP led shipments at 0.70 mnt, followed by Glencore (0.56 mnt), while Japan remained the top destination at 1.75 mnt, followed by China (0.93 mnt). The decline also aligns with reports of weaker Queensland coal exports in January, reinforcing near-term pressure on Australia’s seaborne shipment momentum.

Indonesia shipments soften

Indonesia’s coal exports slipped 9.1% w-o-w to 6.34 mnt in week 06, from 7 mnt in week 05, reflecting softer cargo scheduling and muted spot activity. Shipment activity was led by Taboneo (1.17 mnt) and Bunati (1.14 mnt), followed by Samarinda (0.88 mnt).

On the supply side, Borneo Indobara led shipments at 0.98 mnt, while India remained the top destination at 1.67 mnt, followed by China (1.43 mnt). Export momentum stayed capped amid ongoing uncertainty over Indonesia’s proposed 2026 production quota cuts, which has reportedly weighed on spot export availability and kept buying sentiment cautious.

South African exports drop sharply

South Africa’s coal exports fell significantly by 41.1% w-o-w to 0.78 mnt in week 06, from 1.33 mnt in week 05, reflecting weaker cargo execution and reduced scheduled loadings. Export activity was entirely concentrated at Richards Bay (0.78 mnt), highlighting softer terminal throughput during the week.

On the demand side, India remained the key destination at 0.32 mnt, though shipment flows stayed uneven amid persistent logistics constraints and limited fresh demand visibility. The decline comes even as recent reports indicate some improvement in rail performance supporting Richards Bay exports, although broader infrastructure bottlenecks continue to keep overall shipment momentum volatile.

Colombian coal shipments surge

Colombia’s coal exports jumped sharply by 123.5% w-o-w to 1.08 mnt in week 06, from 0.48 mnt in week 05, supported by improved cargo execution and higher scheduled loadings. Export activity was led by Puerto Nuevo (0.68 mnt), followed by Puerto Bolivar (0.34 mnt), indicating stronger throughput at key terminals.

On the supply side, Prodeco Group led shipments at 0.74 mnt, followed by Cerrejon Mines (0.34 mnt). Spain emerged as the top destination at 0.17 mnt, reflecting fragmented Atlantic Basin demand. The rebound was largely driven by improved operational execution and shipment timing, supported by enhanced security monitoring around key export corridors and ports.

US exports decline after steady momentum

US coal exports declined 21.5% w-o-w to around 1 mnt in week 06, from 1.22 mnt in week 05, reflecting weaker shipment scheduling and softer export momentum. Shipment activity was led by Baltimore (0.40 mnt), followed by Norfolk (0.24 mnt) and Mobile (0.22 mnt).

On the demand front, Germany was the top destination at 0.19 mnt, followed by The Netherlands (0.16 mnt). While port operations remained stable, limited fresh enquiries kept cargo movement dependent on sporadic programmes, although sentiment was supported by recent discussions around a stronger US-Asia trade push, which could aid future energy and coal flows.

Canadian exports remain largely stable

Canada’s coal exports dipped marginally by 1.4% w-o-w to 0.87 mnt in week 06, compared with 0.88 mnt in week 05, indicating stable throughput and consistent port operations. Shipment activity was led by Roberts Bank (0.47 mnt), followed by Prince Rupert (0.25 mnt) and Vancouver (0.15 mnt).

On the supply side, Elk Valley Resources led shipments at 0.15 mnt, while South Korea was the top destination at 0.25 mnt, followed by China (0.24 mnt). Despite stable flows, export momentum remained moderate, although sentiment stayed supported by ongoing discussions around capacity optimisation and infrastructure upgrades at key west coast terminals to sustain coal flows into northeast Asia.

Freight supported, but fixing remains muted

Coal freight rates into India remained range-bound during the week, supported by firm bunker prices and balanced vessel positioning, despite limited fresh cargo enquiries. Higher voyage costs helped prevent sharp rate declines, while cautious buyer sentiment widened the bid-offer gap. Meanwhile, softer dry bulk sentiment, particularly in the Panamax segment, reflected subdued trading activity across coal and grain markets, with elevated freight costs on longer routes dampening spot shipment appetite and keeping exports largely dependent on scheduled cargo movements.

Outlook

Global coal exports are expected to remain volatile in the near term, with shipment momentum largely driven by cargo scheduling and operational execution rather than demand recovery. Australian and South African exports may stay uneven due to fluctuating loading programmes, while Indonesian volumes could remain capped amid policy uncertainty. Meanwhile, coal freight rates into India are likely to remain range-bound, supported by firm bunker prices and balanced vessel availability, although subdued enquiries and cautious buying may continue to limit aggressive fixing activity and spot export growth.

Leave a Reply