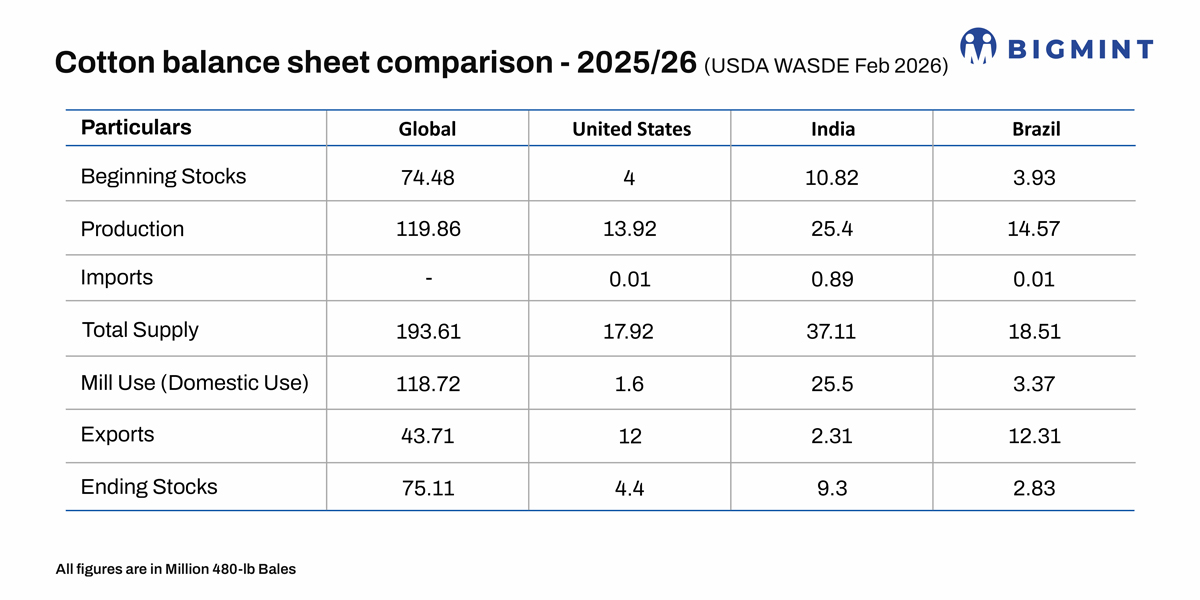

- World production raised to 119.86 million bales; consumption cut to 118.72 million

- US ending stocks rise to 4.40 million bales; farm price lowered to 60 cents/lb

The February 2026 World Agricultural Supply and Demand Estimates (WASDE) report signals a clearer shift toward surplus conditions in the global cotton market. For 2025/26, world cotton production is projected at 119.86 million 480-lb bales, up from 119.43 million in January. At the same time, global mill use is reduced to 118.72 million bales from 118.92 million earlier. With output now exceeding consumption, global ending stocks increase to 75.11 million bales, compared with 74.48 million in January and 73.76 million in 2024/25.

This lifts the global stocks-to-use ratio to 63 percent, up from about 62.6 percent in January and significantly above the 2023/24 level of 73.30 million bales of ending stocks against 114.99 million bales of use. The steady rise in stocks over three seasons shows that supply growth has outpaced demand recovery.

Global trade is also marginally lower. World exports for 2025/26 are estimated at 43.71 million bales, down slightly from 43.77 million in January. Consumption reductions are led by Pakistan (down 100,000 bales) along with smaller cuts in other markets. This reflects weak yarn margins and cautious raw cotton procurement by spinning millers in Asia.

In the United States, the balance sheet has softened further. Production remains steady at 13.92 million bales, but exports are reduced by 200,000 bales to 12.00 million. Domestic mill use is unchanged at 1.60 million bales. With lower exports and steady supply, U.S. ending stocks rise to 4.40 million bales, up from 4.20 million projected in January and 4.00 million in 2024/25. The U.S. stocks-to-use ratio now stands near 32 percent (4.40 million bales ending stocks against total use of 13.60 million bales), compared with about 30 percent in January. Reflecting this looser outlook, the projected 2025/26 upland season-average farm price is reduced to 60 cents per pound, down from 61 cents in January and sharply lower than 76.1 cents recorded in 2023/24.

For ginners, higher ending stocks globally and in the U.S. indicate limited immediate price upside. Inventory management and basis movement will be crucial during the export window. For spinning millers, the comfortable global stocks position provides bargaining power, encouraging short-term buying strategies rather than aggressive forward coverage. Brokers may expect range-bound futures with downside risk if export shipments continue to lag.

Looking ahead, the cotton market remains fundamentally well supplied as of February, with with global stocks at 75.11 million bales and the stocks-to-use ratio at 63 percent.

Leave a Reply