- China led with 1.04 mnt, highlighting strong export concentration.

- Domestic absorption and higher costs squeezed exportable surplus.

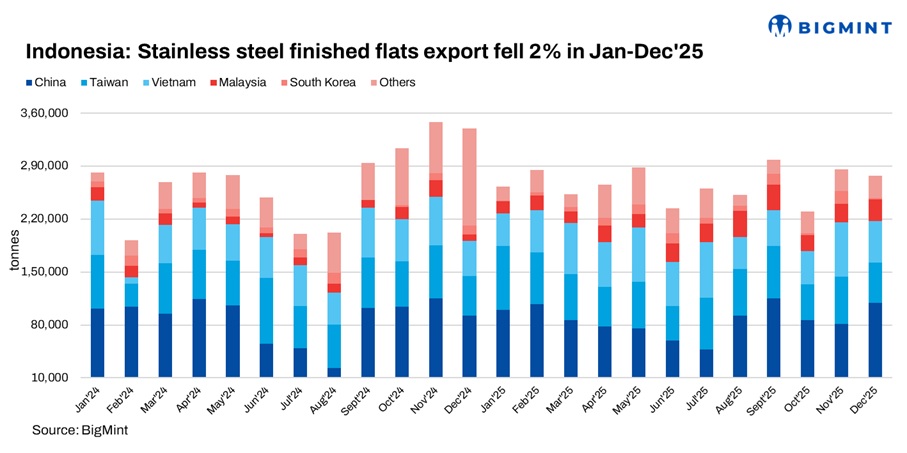

Indonesia’s stainless finished flat exports fell to 3.19 mnt in CY’25, down 2% y-o-y from 3.24 mnt in the previous year, as softer global demand and cautious overseas procurement weighed on shipments, with strong reliance on export markets amplifying the impact of weaker buying across key destinations

Country-wise performance

China remained the largest importer, accounting for 1.04 mnt of exports, down 2% y-o-y from 1.06 mnt in 2024, as softer domestic stainless demand and cautious procurement weighed on annual volumes. However, December shipments rose 25% m-o-m to 109,338 t amid short-term restocking and improved mill activity.

Taiwan ranked second at 0.74 mnt, broadly unchanged y-o-y, with steady downstream manufacturing demand offsetting a 15% m-o-m decline in December and sustaining its role as a key growth market.

India’s imports dropped sharply to 0.04 mnt in Jan–Dec 2025, down 84% y-o-y from 0.26 mnt in the same period of 2024, hit by weak domestic demand, high inventories, and greater reliance on alternative metallics.

Vietnam imported 0.69 mnt, up 12% y-o-y on expanding downstream stainless output and infrastructure demand, while Malaysia posted the fastest growth, rising 88% y-o-y to 0.28 mnt on stronger construction and consumer-goods consumption.

South Korea’s imports declined 3% y-o-y to 96,243 t in Jan-Dec 2025 from 99,052 t a year earlier, while shipments to other destinations dropped 40% y-o-y to 0.02 mnt as trade volumes normalized following strong inflows in 2024.

Port-wise exports:

Bahudopi Port remained the primary export hub, handling 3.15 mnt, down 2% y-o-y from 3.20 mnt, reinforcing its position as Indonesia’s key stainless steel shipping gateway.

Tanjung Perak Port accounted for 40,598 t, declining 10% y-o-y from 45,209 t, while other minor ports handled 5,318 t, registering a 170% increase compared with the previous year.

Factors supporting down in exports

Weak overseas demand: Indonesia’s export-oriented stainless output left shipments highly sensitive to soft demand across key markets—particularly China and India with cautious procurement, elevated inventories, and normalization in smaller destinations driving the marginal decline in 2025.

Growing domestic absorption: Indonesia’s rising stainless capacity is increasingly absorbed domestically, reducing exportable surplus, while global competition and price pressures continue to cap overseas shipments.

Raw material cost: Nickel prices on the London Metal Exchange traded broadly between $14,000–15,000/t, representing an estimated 13% y-o-y correction from the $15,500–$19,500/t range recorded in 2024.

Outlook: China’s stainless steel demand will remain a key determinant of Indonesia’s export trajectory. While structural demand from infrastructure, manufacturing, and equipment sectors continues, procurement trends are likely to remain cautious amid margin pressure at Chinese mills and fluctuating nickel prices. Any sustained restocking cycle or policy-led stimulus in China could support Indonesian shipment volumes, particularly in 300-series flats.

At the same time, Indonesia’s domestic nickel ore quota and mining policy will play a critical role in shaping stainless production economics. Any tightening of nickel ore approvals or supply discipline could influence NPI availability, raw material costs, and ultimately stainless output allocation between domestic consumption and exports. Conversely, stable ore supply and controlled input costs would support production continuity and export competitiveness.

Export performance in 2026 will therefore hinge on China’s stainless demand recovery pace and Indonesia’s nickel supply management, alongside broader regional procurement sentiment.

Leave a Reply