- LME base metals prices fall w-o-w amid cautious sentiment

- Domestic aluminium scrap remains firm despite LME price correction

LME base metals traded lower on a w-o-w basis during the week ended 6 February 2026, reflecting cautious market sentiment. Copper and nickel led the decline, while aluminium, zinc, and lead posted marginal losses. Meanwhile, inventory trends remained mixed, with rising stocks in copper and lead contrasting with drawdowns in aluminium, nickel, and zinc.

Tracking LME price movements, Indian domestic and imported prices assessed by BigMint also declined. Prices of most commodities recorded a sharp correction this week after a notable increase in the previous week. Meanwhile, trading activity across the Indian non-ferrous scrap and semi-finished markets remained low to moderate.

Aluminium

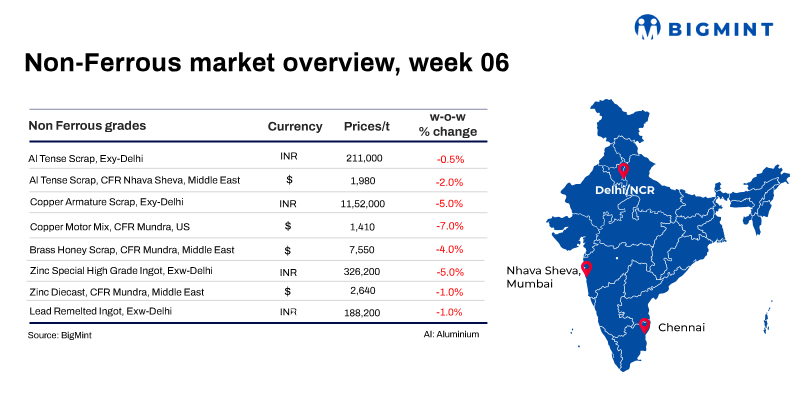

Primary ingot: Domestic aluminium P1020 prices in India declined sharply w-o-w, driven by a fall in LME and MCX aluminium futures.

As per BigMint’s assessment, domestic aluminium ingot prices in Delhi decreased by INR 16,000/t, or 5%, w-o-w to INR 310,000/t. Similarly, Mumbai prices witnessed a sharp decline of INR 39,000/t, or 11%, w-o-w to INR 312,000/t.

Imported, domestic scrap: India’s imported aluminium scrap prices fell w-o-w, aligning with the correction seen on LME. Meanwhile, domestic scrap prices held largely steady amid tight domestic supply.

BigMint assessed Middle East-origin Tense (8-9%) at $1,965/tonne (t), down $35/t w-o-w, whereas Extrusion 6063 edged down by $35/t to $2,865/t, though demand for these grades remained firm.

Despite the decline in LME aluminium prices and imported scrap values, domestic scrap prices remained largely firm, with only limited corrections across grades. This resilience was driven by a continued shortage of domestic scrap, especially tense scrap used by ADC12 producers, which continued to trade at premiums due to restricted availability and steady demand from secondary producers.

ADC12 ingot: India’s aluminium ADC12 prices increased in January 2026, supported by higher domestic and global raw material costs. Prices are expected to remain elevated in February amid tight domestic scrap availability, elevated import costs, and exchange-rate pressures, with settlement discussions indicated in the range of INR 255,000-260,000/t.

Copper

Imported, domestic scrap: Imported copper scrap prices in India fell w-o-w, tracking a drop in benchmark copper futures on the London Metal Exchange (LME). Domestic copper scrap prices also fell.

According to BigMint’s assessment, Middle East-origin Birch Cliff scrap was assessed at $11,770/t CFR Mundra, down w-o-w, while Armature scrap prices fell w-o-w to INR 1,152,000/t ex-Delhi.

Domestic brass honey prices dropped slightly w-o-w. According to BigMint’s assessment, brass honey, exw Jamnagar, Gujarat, stood at INR 682,000/t as against INR 687,000/t a week ago.

Zinc

Primary ingot: India’s zinc ingot (99.995%) prices fell sharply by 5% w-o-w to INR 326,200/t ex-Delhi, supported by a drop in global benchmarks and decline in producers’ offers, BigMint’s assessments showed. The downtrend followed after HZL cut prices by nearly 1%. Following the drop in LME zinc prices, buying remained largely requirement-driven.

Imported, domestic scrap: India’s zinc scrap and by-product market witnessed mixed trends w-o-w, as a sharp correction in LME zinc prices tempered sentiment, even as domestic demand remained stable. BigMint assessed Middle East-origin zinc diecast scrap at $2,640/t CFR west coast India, down 1% w-o-w, amid steady inquiries but resistance to higher replacement costs.

Domestic zinc dross prices moved higher across key markets, supported by ongoing demand from secondary processors. In north India, zinc dross was assessed at INR 265,100/t ex-Delhi, up INR 5,900/t w-o-w. In western India, prices strengthened to INR 260,000/t ex-works Mumbai, with market participants citing healthy offtake from alloy makers and galvanising-linked consumers.

Lead

Domestic primary lead ingot prices stood at INR 198,200/t, down by 1% w-o-w, while re-melted ingots stood at INR 188,200/t, down by 1% w-o-w.

Meanwhile, HZL’s lead prices stood at INR 217,000/t ex-Chanderiya.

Other updates

India-US trade talks advance, aluminium and auto tariffs unresolved

India and the US are nearing a revised trade framework that could cut tariffs on most Indian goods to 18% from 50%, reportedly linked to India halting Russian oil purchases. However, aluminium, steel, and automotive duties remain unresolved. While broader tariff relief may improve market access, lingering metals and auto tariffs continue to pose challenges for manufacturers and trade flows.

Vedanta Aluminium advances Odisha expansion with new land allotment

Vedanta Aluminium has secured 1,447 acres in Odisha for a proposed 3 mnt/year aluminium smelter and 4,900 MW captive power plant in Dhenkanal. The project supports Vedanta’s expansion strategy, strengthens Odisha’s industrial investment drive, and aligns with India’s Aluminium Vision 2025, which targets nearly 37 mnt/year production capacity by FY’47.

Nickel market faces sustained pressure amid Indonesian oversupply

The global nickel market is expected to remain under pressure in 2026 due to persistent oversupply, led by expanding Indonesian output. Weak recovery in stainless steel and battery demand continues to weigh on prices. Rising NPI and MHP capacities are likely to keep inventories elevated, with prices struggling to find a durable floor amid volatile market conditions.

Leave a Reply