- Supply uncertainty supporting prices

- Portside coal inventories largely stable

Indian portside prices of Indonesian-origin thermal coal increased on a w-o-w basis during the week ended 6 February 2026, supported by supply-side constraints and cautious buying sentiment.

According to BigMint assessment, 5,000 GAR coal prices rose by INR 50/t w-o-w, assessed at INR 7,300/t at Kandla and INR 7,200/t at Vizag. Similarly, 4,200 GAR coal prices increased by INR 100/t w-o-w, reaching INR 5,700/t at Kandla and INR 5,600/t at Vizag.

In contrast, 3,400 GAR coal prices remained unchanged w-o-w at INR 4,500/t at Navlakhi.

Indonesian market awaits clarity on production cuts

An Indonesian miner indicated that supply visibility remains limited, as coal production deductions in CY’26 may range between 40-70%. Export availability is further influenced by the proportion of output committed to long-term contracts and the fulfilment of Domestic Market Obligation (DMO) requirements. While larger miners generally have higher long-term commitments, many small- and mid-sized producers rely predominantly on spot sales, ensuring some availability in the spot market. Consequently, spot supply may remain tight but not fully constrained.

Market participants noted that coal prices remained volatile during the week amid uncertainty. Several miners refrained from offering fresh cargoes and deferred laycans due to ambiguity surrounding RKAB approvals, which restricted near-term supply. This tightening supported firmer prices in Australian and South African coal markets. Additionally, Indonesian miners expressed concerns over the prevailing regulatory framework and called for a review of recent policy measures, further amplifying supply-side risks. The potential for China to increase coal exports was also cited as a downside risk to seaborne demand, which could exert renewed pressure on Indonesian coal exports.

Freight market overview

Seaborne freight rates remained stable on a w-o-w basis. BigMint assessed Supramax freight rates from East Kalimantan to Navlakhi at $ 11/dmt, reflecting steady vessel availability and limited volatility in freight costs.

Portside inventories and power sector stock position

India’s portside thermal coal inventories remained largely stable w-o-w, despite divergent trends across ports. Dhamra and Kandla recorded notable stock additions, while inventories at Adani and Agarwal ports declined modestly. Overall, total portside thermal coal stocks edged up marginally by 0.1% w-o-w to 12.96 mnt in week 5, compared with 12.95 mnt in week 4.

Coal stocks at Indian power plants stood at 57.1 mnt as of 5 February, marking a 3% w-o-w increase, equivalent to approximately 19 days of coverage. A total of 18 power plants continued to operate under critical stock levels, including seven domestic coal-based plants, seven imported coal-based plants, and 4 washery reject-based plants.

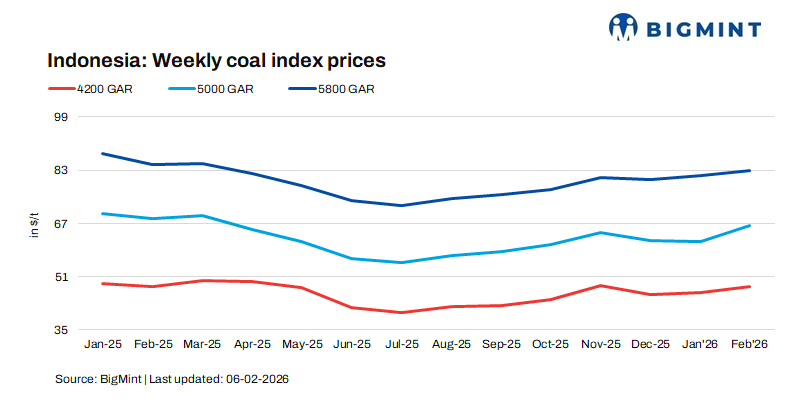

Indonesian benchmark price movements

Indonesian weekly benchmark prices recorded modest gains reflecting tighter supply conditions and cautious buying interest. 5,800 GAR coal prices increased by $ 1.32/t, 4,200 GAR by $ 0.86/t, and 3,400 GAR by $ 1.01/t w-o-w.

Outlook

Indian portside prices of Indonesian thermal coal are expected to remain firm to range-bound in the near term, supported by supply constraints and regulatory uncertainty, while stable freight rates, adequate inventories, and potential demand softness may cap further gains.

Leave a Reply