- Discounts steady for 57% fines, pressure persists

- Firm domestic ore prices continue squeezing exporter margins

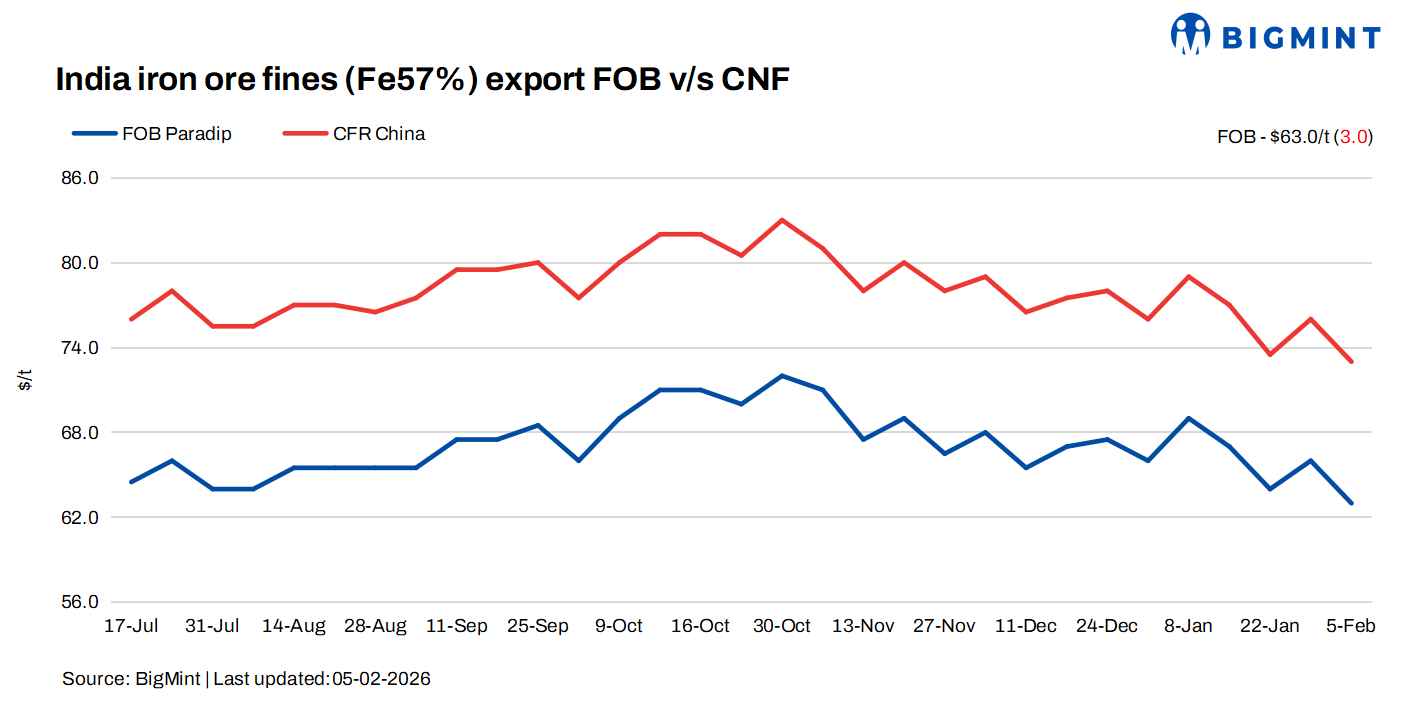

Indian iron ore fines export prices decreased w-o-w on 5 February 2026, with widening of discount levels against the global Fe 61% benchmark index. The seaborne market continued to witness cautious sentiment, although sporadic buying interest provided some stability to prices.

Prices, deals

BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export prices inched down by $3/tonne (t) w-o-w to $63/t FOB east coast on Thursday. Index has hit lowest since mid-Aug’25, as per data maintained with BigMint.

No export deals were reported by Indian sellers in the overseas market during the assessment window, as trading activity remained largely muted. BigMint did not record any confirmed export transactions, although a few discussions were heard for March laycan cargoes without closure.

According to sources, the export discount for Fe 57% fines was heard around 21-23%, while discounts for Fe 55% material widened to nearly 26-27% against the global fines index, reflecting continued pressure on lower-grade offerings.

Market scenario

No major export trades for 57% Fe iron ore fines were recorded, as seaborne prices dropped by around $3/t, which further weighed on market sentiment.

An overseas buyer said, “Prices are softening, but mills are not in a hurry. Many expect further corrections before stepping in.”

Market sources said that although single-mine cargoes are still preferred for their consistent quality, even these could not draw firm bids in the current falling market. Blended fines faced even stronger resistance, as buyers remained cautious about quality variations at a time when overall demand is already fragile.

An exporter told BigMint, “There is talk, but no closures. Buyers are testing lower price ideas after the recent fall, and sellers are reluctant to accept steep discounts.” Some inquiries were heard for March laycan cargoes ahead of the Lunar New Year period, but this seasonal factor did little to improve sentiment. A trader said, “Enquiries are there, but it’s mostly price discovery – not real demand.”

On the domestic side, iron ore prices in the east coast region continued to stay firm, with miners maintaining their offer levels. This has further squeezed exporter margins and made overseas sales less workable. A trader said, “Domestic ore is firm while export prices are falling – margins don’t work.”

On the supply side, market activity was subdued as sellers largely refrained from offering material. Several exporters held back shipments, targeting higher realisations around $78-80/t CFR, while others diverted volumes to the domestic market where prices were comparatively more remunerative, further constraining export-side liquidity.

Domestic vs export market

Domestic prices exceeded export realisations by around INR 300/t ($3/t), with the gap being largely stable w-o-w. Iron ore fines (Fe 57%) prices in Odisha were recorded at INR 4,100/t ($45/t) ex-mines, steady w-o-w on 5 February. Meanwhile, the ex-mines realisation in exports from the Barbil region rose w-o-w to INR 3,800-3900/t (42/t) ex-mines.

Chinese spot prices edge down w-o-w: The benchmark iron ore fines index (Fe 61%) was recorded at $102/t CFR China, down by $1/dmt w-o-w on 4 February. Prices eased early in the week despite fresh trades, mainly in medium-grade fines, amid thin liquidity and softer sentiment after raw material price declines. Softer seaborne prices prompted Shandong-based mills to step up purchases of imported cargoes instead of drawing from port inventories.

DCE iron ore futures rise w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the May 2026 contract closed at RMB 768.5/t ($111/t) on 5 February 2026, depreciating by RMB 25.5/t ($4/t) w-o-w.

Rationale

- Zero (0) deals for Fe 57% was recorded during this publishing window. Therefore, T1 trade was given 0% weightage in the index calculation. For the detailed methodology, click here.

- BigMint received fifteen (15) indicative prices in the current publishing window, and thirteen (13) were considered for price calculation as T2 inputs and given rest 100% weightage.

Outlook

Export sentiment is likely to remain weak, with mills buying cautiously amid softer prices and tight exporter margins. Activity may stay slow unless demand improves or prices stabilise.

Leave a Reply