- Turkiye: Deep-sea market stable amid limited US/EU offers

- Pakistan: Low utilisation keeps shredded scrap sentiment subdued

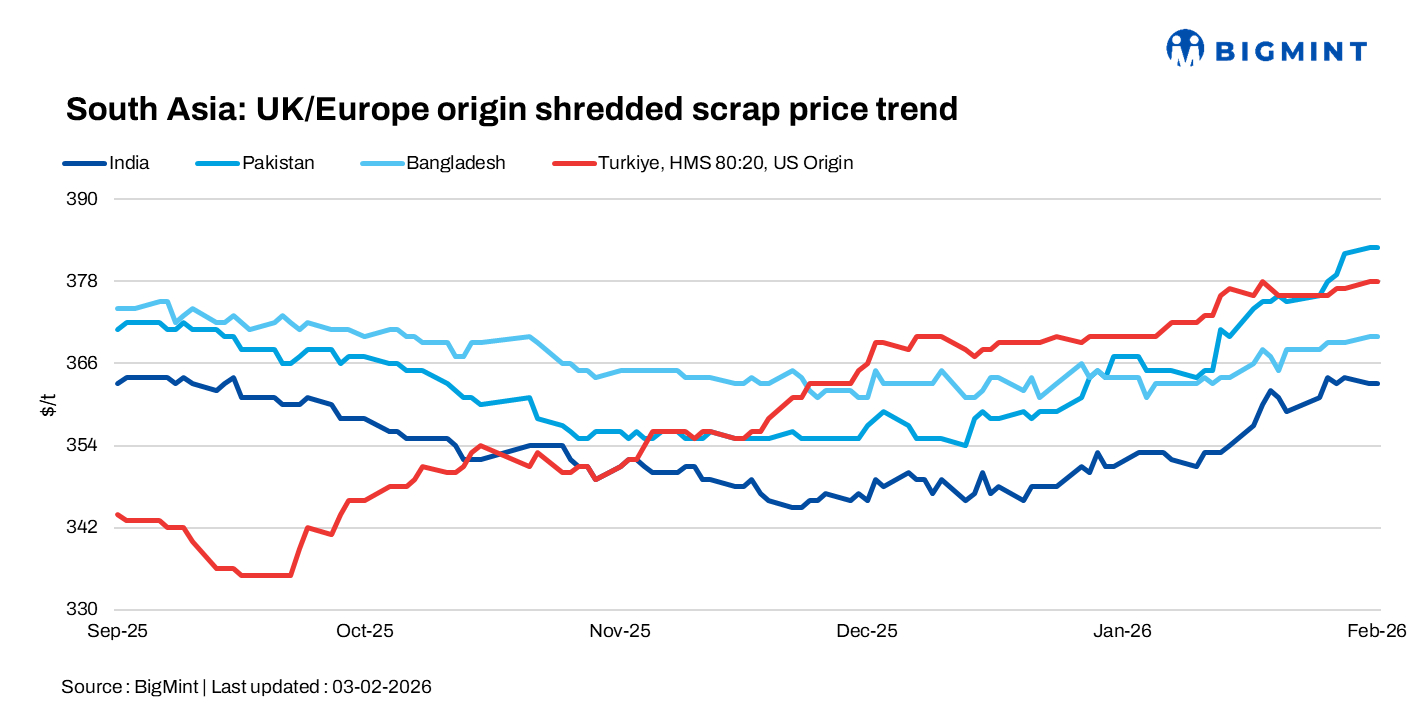

South Asia’s imported scrap market stayed slow on 3 February 2026, with India facing weak buying, Pakistan constrained by low utilisation, Bangladesh seeing steady but subdued prices, and Turkiye holding stable amid limited deep-sea offers and tight US domestic supply.

Region-wise highlights

India: Imported scrap prices in India remained under pressure day on day, with buying interest muted due to comfortable domestic scrap availability and cautious mill sentiment. Market activity stayed thin, with few confirmed deals. EU-origin shredded was last heard near $365/t CFR at Nhava Sheva and Mundra, while HMS 80:20 around $335-340/t was considered workable by select buyers.

Australian offers into India continued to indicate a steady range, with HMS (80:20) at $330–335/t, HMS 1 at $340-342/t, shredded at $355-358/t, and PNS at $360-365/t. Confirmed trades of machine-loaded HMS from Brazil at $345 CFR Mundra and a African HMS (25 mt) at $352 CFR Mundra.

Pakistan: Imported shredded scrap sentiment in Pakistan remained subdued, with capacity utilisation still low at 35-40% and only a few regions operating near 50%. UAE-origin shredded held at $400/t CFR Qasim and sheared HMS at $375/t, though buying interest improved slightly amid active procurement from the UAE and EU. A small deal of UAE-origin HMS 80:20 was concluded at $374/t CFR Qasim.

Bangladesh: Imported ferrous scrap prices in Bangladesh remained largely unchanged, with Australian-origin HMS (80:20) at $345-350/t, HMS 1 at $355-360/t, shredded at $365-370/t, and PNS at $370-375/t, while Japanese H2 traded steady in the $355-357/t CFR Chattogram range.

Turkiye: Deep-sea scrap prices held stable through the week, with the market showing little direction amid limited offers from both US and European suppliers. Uncertainty persisted as buyers waited for clearer signals, while US exporters stayed largely absent from the export market.

By 3 February, deep-sea prices remained steady, with US-origin material indicated around $380-382/t CFR. Expectations of a $20-30/lt rise in February-delivered shredded in the US-driven by seasonal tightness and harsh winter weather on the East Coast-kept exporters focused on the domestic market and slowed overseas availability.

Leave a Reply