- India: Imported scrap under pressure, mills buy hand-to-mouth

- Pakistan: Shredded prices firm, HMS at workable level keeps suppliers engaged

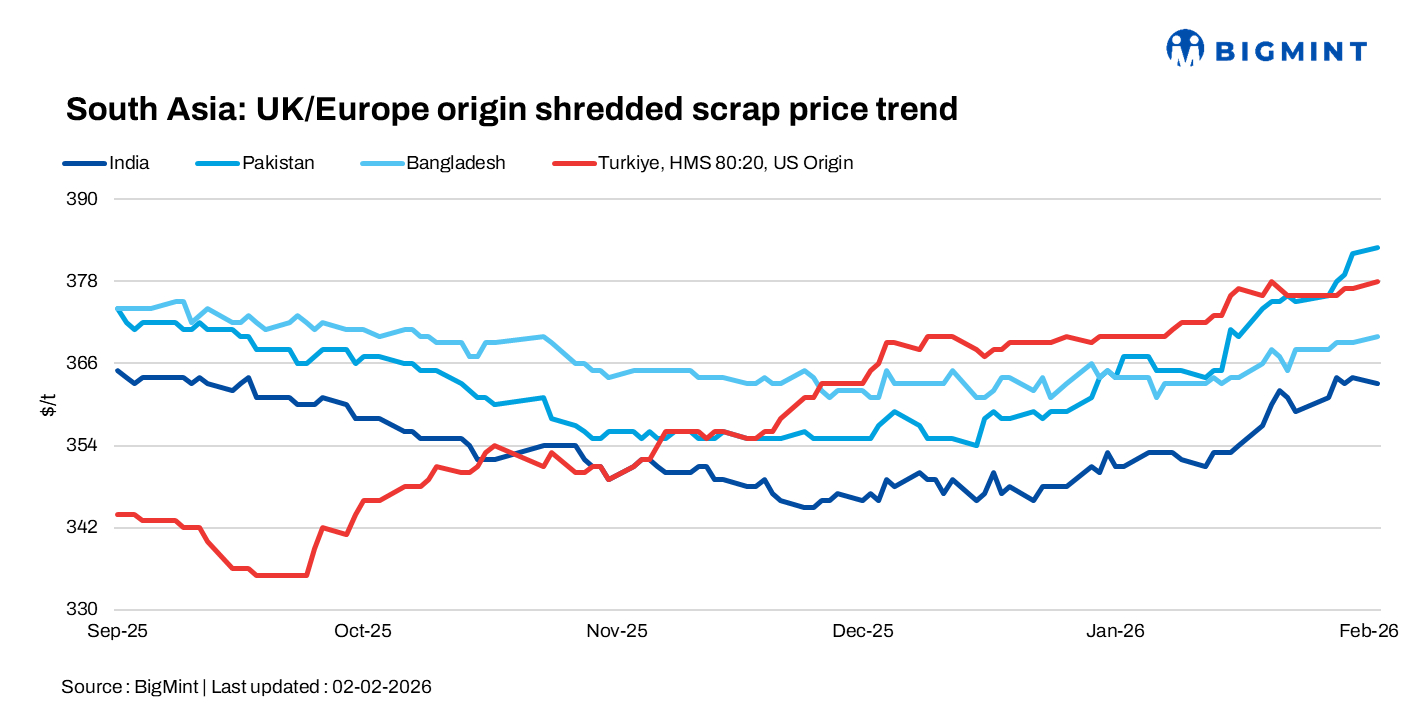

South Asia’s imported scrap market stayed subdued on 2 February 2026, with India, Pakistan and Bangladesh seeing cautious, need-based buying amid adequate supply, while Turkish prices remained mostly stable, supported by weather-led supply constraints despite persistent margin pressure on mills.

Region-wise highlights

India: Imported scrap prices in India remained under pressure day on day, with buying interest subdued amid comfortable domestic scrap availability and cautious mill sentiment. Offers from multiple origins were reported, with Africa-origin HMS 80:20 (casting) quoted at around $343/t, Chile-origin HMS (1-2%) at $340-342/t, and UK-origin HMS 80:20 at $332-335/t CFR. Shredded scrap continued to command a premium, with offers largely in the range of $363-365/t CFR.

Market activity, however, stayed thin, with limited deal closures. EU-origin shredded was last heard at around $365/t CFR at Nhava Sheva Port and Mundra Port, while HMS 80:20 at $335–340/t was considered workable by some buyers. Despite this, no major trades were reported, as mills continued to procure strictly on a need basis, supported by adequate local scrap availability.

Pakistan: Imported shredded scrap sentiment in Pakistan remained mixed, with UK and EU offers heard around $380/t CFR, while UAE-origin material was quoted higher at $395/t and above and a Bahrain-origin parcel was likely to settle near $390/t CFR; meanwhile, keeping Pakistan attractive for suppliers even as buyers remained selective.

Bangladesh: Imported ferrous scrap prices in Bangladesh were largely unchanged, with Japanese H2 assessed in the range of $355-357/t CFR Chattogram Port. Containerised scrap from Oceania also traded within familiar bands, with HMS 80:20 quoted at $345-350/t CFR, HMS 1 at $355-360/t CFR, and shredded material indicated at $365-370/t CFR, reflecting steady but cautious buying interest.

Turkiye: Deep-sea imported scrap prices were largely stable on 2 february, with market participants reporting muted trading activity amid tightening margins on both the buying and selling sides.

Prices edged slightly higher despite muted trading, supported by supply-side constraints. US-origin deep-sea scrap was indicated around $380-382/t CFR, while EU-origin material was heard near $375/t CFR, though rising labour, energy and raw material costs in January continued to squeeze mill margins as finished steel prices failed to keep pace.

Leave a Reply