- Multiple east coast deals reported this week

- Domestic coal prices stable, sponge prices offer mild support

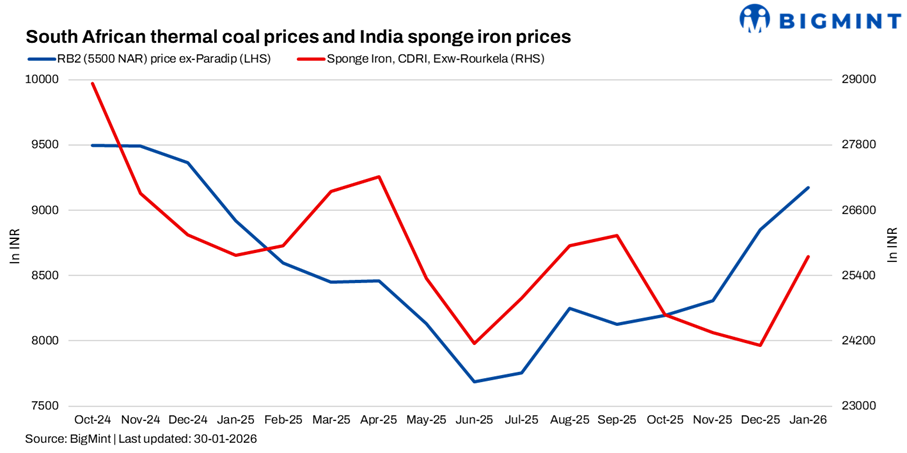

South African thermal coal prices at Indian ports moved higher again in week 5 as tightening inventories and selective trades supported offers. As per BigMint’s assessment, exw-Paradip 5,500 NAR grade coal increased by INR 100/t w-o-w to INR 9,500/t, while 4,800 NAR remained stable at INR 8,100/t. At Vizag, 5,500 NAR rose by INR 150/t to INR 9,400/t and 4,800 NAR gained INR 50/t to INR 8,000/t. Indicative east coast levels were heard at INR 9,400-9,500/t for 5,500 NAR and INR 8,100-8,200/t for 4,800 NAR. Offers at Ennore were around INR 9,700/t plus GST and Mangalore around INR 9,450/t plus GST.

“The majority of the South African coal port stocks at Dhamra and Gangavaram have been sold out and we shall now resume offers for February deliveries. Sponge iron prices have remained supported which have pushed offers high”, highlighted a participant from a trading house.

Trades reported despite selective buying

Several deals were concluded during the week despite cautious buying sentiment. A 50,000 t cargo was booked at $92/t CNF Paradip, while another trader fixed 75,000 t of 5,500 NAR at around $94/t CNF east coast and a 75,000 t RB2 deal was concluded by a trader at around $95/t CNF Mangalore. A parcel of 2,000 t was traded at INR 9,400/t exw-Mangalore. CNF India levels were indicated at $95/t for 5,500 NAR and $81-82/t for 4,800 NAR, with freight around $13-14/t. In Dhamra, 30,000 t of RB1 was reported sold at INR 10,700/t. Market sources said material at Haldia was largely sold out, with limited fresh offers from ports such as Gangavaram and Dhamra.

Domestic scenario

Domestic non-coking coal offers remained stable w-o-w, supported by steady supply from SECL auctions. On 27 January, SECL offered 1,716,050 t and allocated 915,200 t, with bulk mid-CV grades fetching near-floor prices. Sponge iron CDRI, exw-Rourkela, increased by INR 50/t w-o-w to INR 26,300/t, while d-o-d gains of INR 100-400/t were recorded across regions on 29 January. Finished steel demand remained measured, keeping overall buying selective despite firmer raw material sentiment.

Outlook

Portside prices are expected to remain firm in the near term, supported by low stock levels, reported cargo bookings and steady raw material sentiment, although broader demand remains need-based.

Leave a Reply