- Coated steel prices rise on improved trade activity

- Market sentiment improves despite uneven regional demand

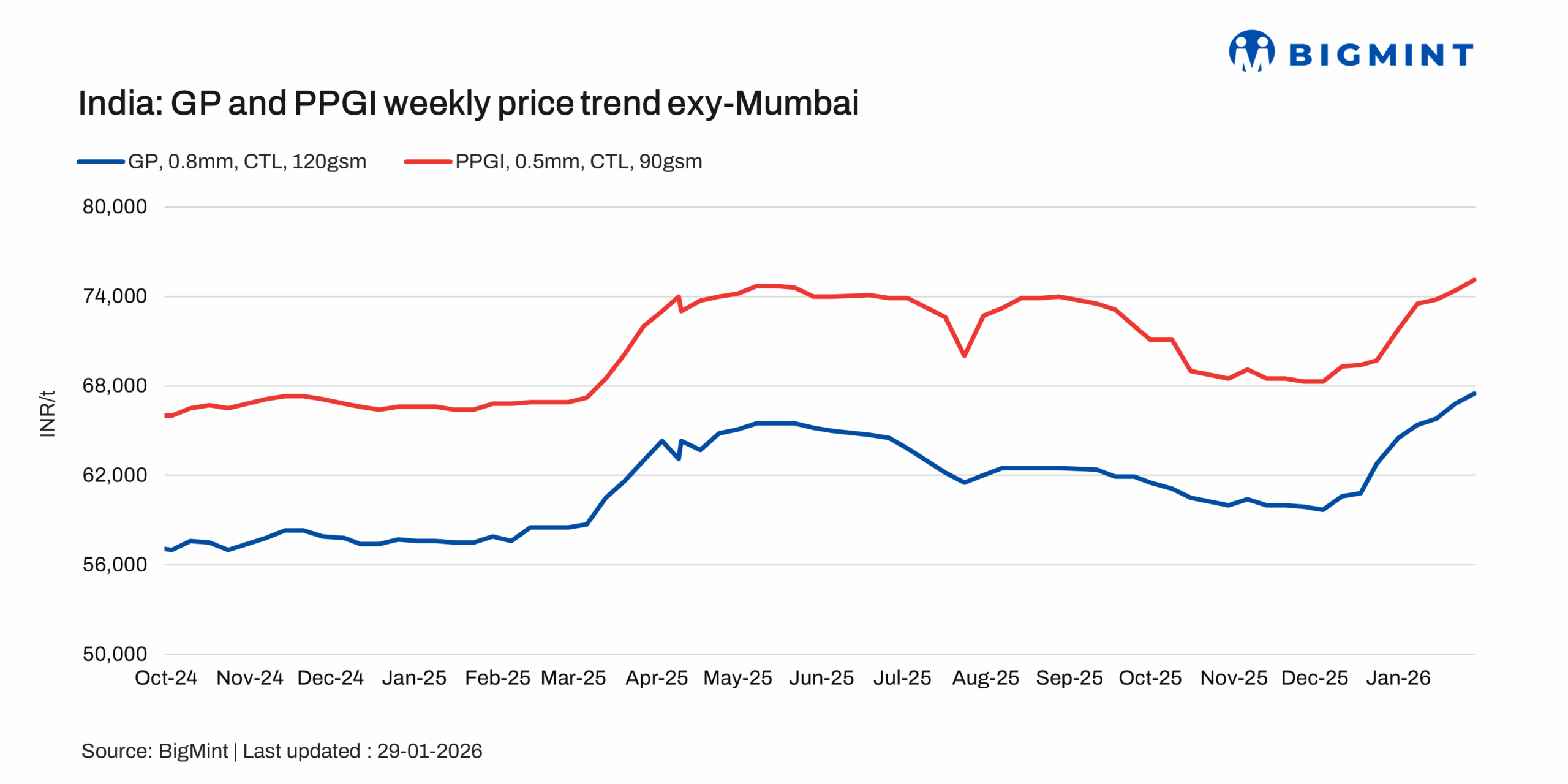

Indian coated flat steel prices rose slightly w-o-w on 29 January 2026, supported by slightly firmer demand and a modest improvement in trading activity. While buying interest remained selective, market participants reported comparatively better trade enquiries, indicating a gradual pickup in demand. Sentiment was further influenced by a price increase announced by one of the major mills during the week. However, market sentiment remained mixed, as demand conditions varied across regions: some markets witnessed slower offtake, while others reported stable-to-improving demand.

Rising zinc prices continued to provide cost-side support to the coated steel market. Hindustan Zinc raised zinc ingot prices to INR 343,500/t ($3,735/t) as of 29 January, while LME zinc prices climbed to $3,476/t, up sharply w-o-w, pushing up replacement costs for galvanisers. Domestic zinc scrap and by-product prices also strengthened, with zinc diecast scrap assessed at $2,660/t CFR west coast, zinc dross at INR 259,200/t ex-Delhi and INR 255,000/t ex-Mumbai, and zinc oxide at INR 247,200/t ex-Delhi. These firm upstream prices limited downside risks for coated steel prices and supported mills’ pricing stance despite regionally mixed demand.

The upward movement in flat steel substrates continued to lend cost-side support to the coated steel market, as higher HRC and CRC prices pushed up replacement values for galvanisers. Trade-level HRC prices were assessed in the range of INR 50,000-52,900/t, while CRC prices were heard at INR 54,500-60,500/t, following recent mill price hikes. BigMint’s benchmark HRC assessment rose by INR 700/t ($8/t) w-o-w to INR 52,400/t, while CRC prices increased by INR 600/t to INR 57,900/t ex-Mumbai. The firmer substrate pricing environment enabled GP, GL, and PPGI producers to hold offers at elevated levels despite regionally mixed demand.

As per latest assessment, galvanised plain (GP) coil prices are at INR 67,500/t ($734/t) exy-Mumbai, up by INR 700/t ($8/t) w-o-w. Market offers were largely heard in the range of INR 67,000-68,000/t ($728-739/t). The price uptick was supported by marginally firmer demand and improved trading activity during the week.

Pre-painted galvanised iron (PPGI) prices were assessed at INR 75,100/t ($817/t) exy-Mumbai, registering a w-o-w increase of INR 700/t. Offers were mostly reported in the range of INR 74,500–75,500/t ($811-822/t), supported by selective restocking and stable buying interest.

Meanwhile, galvalume (BGL) prices were assessed at INR 78,500/t ($854/t) exy-Mumbai, up by INR 600/t ($6/t) w-o-w, with offers heard in the range of INR 78,000-79,000/t ($849-860/t). Prices moved up on the back of firm mill offers, though demand remained regionally mixed.

All prices are exclusive of 18% GST.

Market updates:

West:

Market activity in the western region remained subdued, with demand conditions weak amid recent price increases. However, the slowdown was attributed more to higher prices rather than excess inventory, as material availability was reported to be relatively tight in the market. Despite muted buying sentiment overall, demand for GP material was heard to be present, though trade conversions remained limited.

North:

The northern market witnessed steady demand for coated products, with trading activity reported to be healthy during the week. Improved demand visibility supported market sentiment, and participants indicated a positive near-term outlook, although buying continued to remain selective.

South:

Demand in the southern region remained supportive, with market participants reporting active trade executions. Overall sentiment stayed positive, and the near-term outlook was optimistic, backed by ongoing demand and improved market confidence.

Outlook:

Market sentiment is expected to turn cautiously positive as improving trade enquiries in select regions and tighter material availability begin to influence buying behaviour. While participants are likely to remain selective, expectations of possible mill price revisions in early February could prompt some advance purchases.

Leave a Reply