- G4 coal volumes drop, prices correct sharply

- Premiums normalise after mid-Jan’26 spike

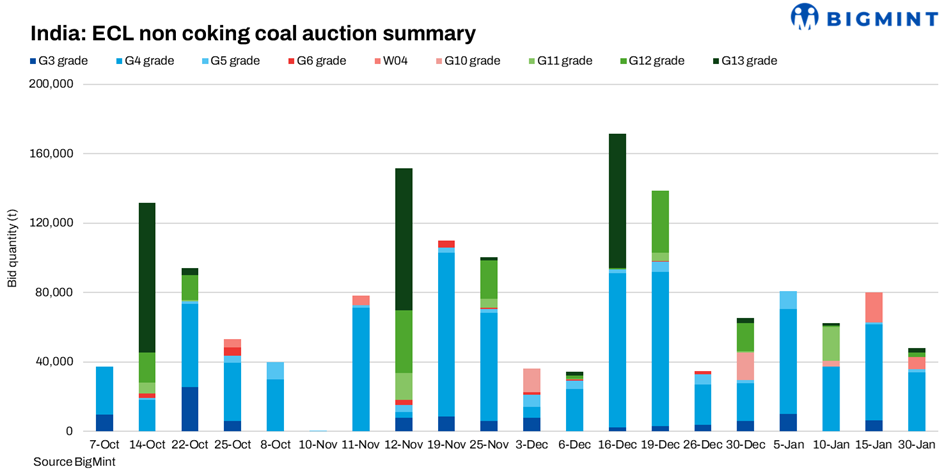

Eastern Coalfields Limited’s (ECL) auction on 20 January 2026 reflected cooling interest and softer prices compared with the 15 January auction, thereby indicating renewed buyer caution. Total bid quantity declined sharply to 47,900 t, down from 80,300 t on 15 January, underscoring restrained procurement despite continued availability of mid-CV coal.

The auction outcome suggested that buyers remained selective and price-sensitive, expanding volumes only where pricing aligned closely with recent benchmarks rather than chasing quality premiums aggressively.

G4 coal prices fall sharply

G4 grade coal continued to dominate allocations but with lower volumes and weaker average pricing. Total G4 bid quantity stood at 34,050 t, compared with 55,500 t on 15 January, accounting for around 71% of total auction volumes.

Average G4 prices eased to INR 4,515/t, down from INR 5,505/t in the previous auction, marking a clear correction after the sharp premium-driven rally seen earlier. Mine-wise outcomes showed tighter price convergence across sources. Sonepur Bazari OC accounted for the bulk of G4 volumes at 20,000 t, clearing at INR 4,703/t, while Nakrakonda OC supplied 9,050 t at INR 4,439/t.

Underground sources such as Khottadih UG, Lower Kenda UG, and Shyamsundarpur UG cleared smaller parcels largely around INR 4,437/t, significantly below the elevated UG realisations of over INR 7,000/t recorded on 15 January. This highlighted a normalisation of UG premiums and reduced willingness to pay for scarcity-driven parcels.

Volumes limited for lower-CV grades

Interest outside G4 stayed muted and price-disciplined. W04 accounted for 7,000 t, clearing at an average of INR 4,612/t, broadly aligned with recent reserve-linked levels. G13 volumes stood at 2,600 t at INR 1,713/t, while G12 cleared 2,350 t at INR 1,798/t, reflecting strictly utility-linked buying.

G5 saw limited interest, with 1,900 t sold at INR 4,084/t, indicating that buyers avoided expanding exposure to non-core grades amid softer sentiment. Compared with 15 January, volumes across all non-G4 grades declined, reinforcing the narrower procurement focus.

Buyer participation narrows, remains fragmented

Buyer participation on 20 January was more limited and fragmented than in the previous auction. Iconic Coal Company emerged as the largest buyer with 5,400 t of G4 at INR 4,567/t, followed by Shakambhari Ispat and Power with 4,650 t at INR 4,667/t, and Satyam Smelters with 4,000 t at INR 4,717/t.

Traders such as Khatu Shyam Steels, Mark Trading Company, and Ranisati Coal Carriers selectively lifted smaller G4 parcels, largely within a tight INR 4,400–4,700/t range. Participation in G12 and G13 was confined to a handful of buyers, including Jaiswal Brothers and Shree Balaji Coal Traders, reflecting strictly requirement-driven procurement.

Comparison with 15 January auction

- 40% lower total bid volumes

- Clear correction in G4 prices

- Sharp moderation in UG-origin premiums

- Greater price convergence across mines

Takeaway

Buyers have clearly scaled back volumes and resisting elevated premiums. Demand remained anchored to G4 coal, but pricing reverted closer to sustainable levels.

Leave a Reply