- Supply constraints supported prices, but deals stayed selective

- Domestic coal availability capped aggressive import buying

Coal markets this week reflected a guarded but firm tone. Import prices stayed supported by supply-side constraints and global cost pressures, while buying remained selective and largely need-based. Domestic availability continued to cap aggressive procurement, keeping volumes controlled. Participants focused on grade suitability and immediate requirements rather than stock building, with holidays and logistical factors still influencing trade flow. Overall sentiment suggested stability with an upward bias, but without broad-based demand revival.

Indonesian coal prices mixed

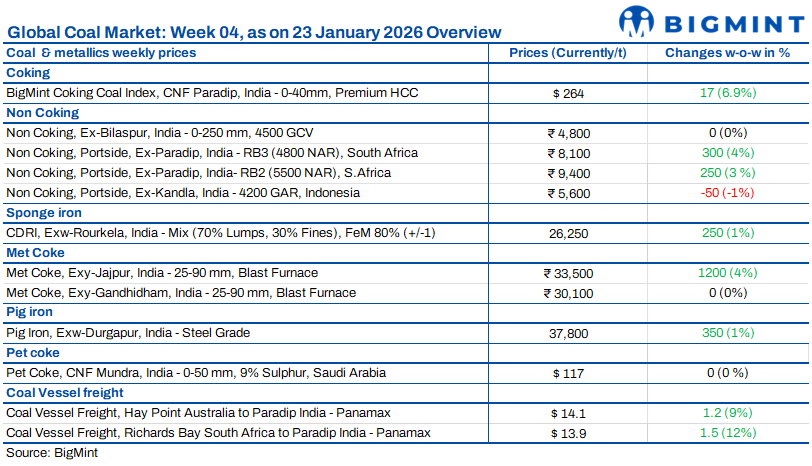

Indian portside Indonesian thermal coal prices showed mixed movement in the week ended 23 January 2026 as cautious, need-based buying persisted. As per BigMint’s assessment, 5,000 GAR prices rose by INR 50/t w-o-w to INR 7,250/t at Kandla and INR 7,150/t at Vizag. In contrast, 4,200 GAR declined by INR 50/t to INR 5,600/t at Kandla and INR 5,500/t at Vizag, reflecting weak industrial demand. Lower-grade 3,400 GAR firmed by INR 50/t to INR 4,500/t at Navlakhi on limited availability. Buying remained restricted to immediate needs amid adequate stocks. Indonesian benchmarks rose marginally, but the impact on Indian prices stayed limited.

South African coal prices hit highs

South African thermal coal prices at Indian ports strengthened further in January, reaching one-year highs as tight portside stocks, firmer global indices and higher freight costs pushed offers up. As per BigMint’s assessment, exw-Paradip 5,500 NAR rose by INR 250/t w-o-w to INR 9,400/t, while 4,800 NAR increased by INR 300/t to INR 8,100/t. At Vizag, 5,500 NAR climbed by INR 250/t to INR 9,250/t and 4,800 NAR jumped by INR 350/t to INR 7,950/t. Despite higher prices, trades remained selective, with limited deals around INR 9,000-9,100/t. Export offers stayed firm at $79-80/t FOB and $93-94/t CFR India, while domestic coal prices stayed unchanged.

Coking coal index jumps sharply

BigMint’s premium hard coking coal index surged by $17/t w-o-w to $264/t CNF Paradip on 23 January 2026, supported by a reported 75,000 t cargo sale at $250/t FOB Australia. Australian coking coal prices rose further as heavy rainfall from Cyclone Koji disrupted mining and port operations, with vessels awaiting berthing. Indian met coke prices stayed supported, with eastern India BF-grade coke rising by INR 1,200/t to INR 33,500/t ex-Jajpur on higher input costs. Indian Tier-I mills lifted rebar prices by up to INR 1,250/t, improving steel margins. Chinese met coke prices stayed stable despite hike attempts. Trade sources expected the rally to continue short term, though buying resistance capped further sharp gains.

Met coke prices firm

Indian BF-grade metallurgical coke prices rose w-o-w, supported by a sharp rally in coking coal prices, though spot trade activity remained subdued. In eastern India, BF-grade met coke prices increased by INR 1,200/t to INR 33,500/t ex-Jajpur, driven by higher raw material costs and firmer upstream sentiment. In contrast, western India prices stayed unchanged at INR 30,100/t ex-Gandhidham due to comfortable supply and weak buying interest.

Demand remained muted as buyers relied on inventories, while Sankranti holidays disrupted operations. In China, met coke prices stayed stable as mills resisted hikes despite rising costs. Indian pig iron prices rose by INR 1,050/t to INR 37,750/t ex-Durgapur, lending indirect support. Prices were expected to stay muted short term, with potential upside from late February.

Coal freights edge up

Dry bulk coal freight rates into India edged up w-o-w, supported by higher bunker prices and a recovery in the Baltic index, though fixing activity remained limited. The Baltic Dry Index rose 229 points to 1,761, with Panamax up 216 points and Supramax up 56 points. Rising crude prices lifted bunker costs, squeezing owner margins and prompting resistance to lower rates, even as ample tonnage capped gains.

Panamax freights from Australia to India increased to $14.1/dmt, while South Africa-India rose to $13.9/dmt. Indonesia-India Supramax rates stayed flat at $10.8/dmt. Despite firmer sentiment, fixtures remained sparse, mainly involving SAIL. Near-term outlook stayed soft to range-bound amid weak cargo enquiries and high vessel availability.

Leave a Reply