- Mills remain firm on recent list price increases in Jan’26

- South, north see better trading but west continues to lag

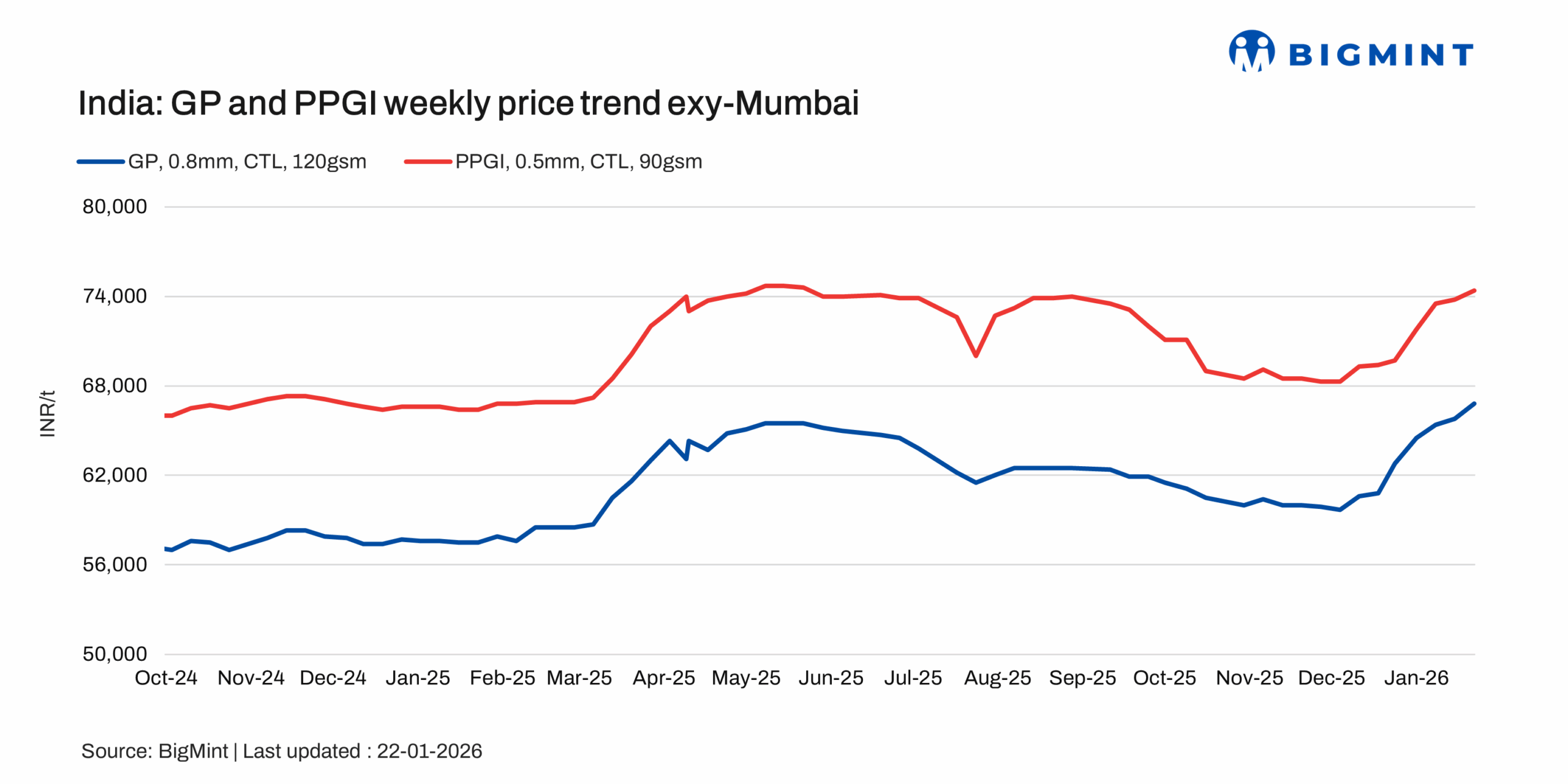

Indian coated flat steel prices rose slightly w-o-w on 22 January, as per BigMint’s assessments, supported by an improvement in trading activity. While overall, buying remained cautious, the market witnessed better participation compared to last week, with selective restocking and increased trade inquiries reflecting gradual demand improvement. Market sentiment strengthened as mills remained firm on recent price increases, and participants expect trading activity and demand to improve further in the coming weeks as the market adjusts to revised prices.

As per the latest assessment on 22 January 2026, galvanised plain (GP) coil (0.8 mm/CTL, 120 gsm, IS 277) prices were assessed at INR 66,800/t ($739/t) exy-Mumbai, up by INR 1,000/t ($11/t) w-o-w, with offers largely heard in the range of INR 66,000-67,500/t ($720-725/t). Prices increased w-o-w, supported by improved trade activity and mills seeking absorption of recent price increases.

Galvalume (0.5 mm/CTL, 1,220 mm, AZ150, IS 15961) was assessed at INR 77,900/t ($861/t) exy-Mumbai, up by INR 1,400 ($15/t) w-o-w, with offers heard in the range of INR 77,500-78,500/t ($846-857/t). Prices moved up w-o-w, tracking firm mill offers and steady buying interest.

Meanwhile, PPGI (0.5 mm/CTL, 90 gsm, IS 14246) was assessed at INR 74,400/t ($823/t) exy-Mumbai, up by INR 600/t ($6/t) w-o-w, with offers largely heard in the range of INR 74,000-75,000/t ($808-819/t). The w-o-w increase could be attributed to selective restocking and improving market sentiment.

All prices are exclusive of 18% GST.

Market update

West

Market activity in the western region was sluggish, with sentiment staying mixed and cautious. Trade continued to be dull, and the recent price rise was largely attributed to mills’ mid-January price revisions rather than any meaningful improvement in demand.

South

The southern market exhibited relatively firm sentiment, with trading activity continuing. However, liquidity remained tight due to the long weekend this week, resulting in fewer working days. Market participants indicated that faster liquidation was being prioritised, especially with payments driving trade decisions. Demand clarity is expected to improve once normal working schedules resume.

North

Trading in the northern region improved compared with the previous week, supported by better demand visibility. Additionally, speculation around a potential February price hike by mills lent support to market sentiment, making participants slightly more optimistic, even as overall buying remained selective.

Outlook

The coated flat steel market has seen recent price support driven largely by supply-side actions, while demand recovery remains gradual. Mills are closely monitoring price absorption at current levels, with buyers continuing to trade selectively.

Looking ahead, market activity is expected to improve as regular trading resumes. Industry chatter indicates that mills may attempt further price hikes next month, though the sustainability of any increase will depend on stronger demand and acceptance at higher price levels.

Leave a Reply