- Finished flats get support from strong dollar

- Tsingshan hikes global stainless steel prices

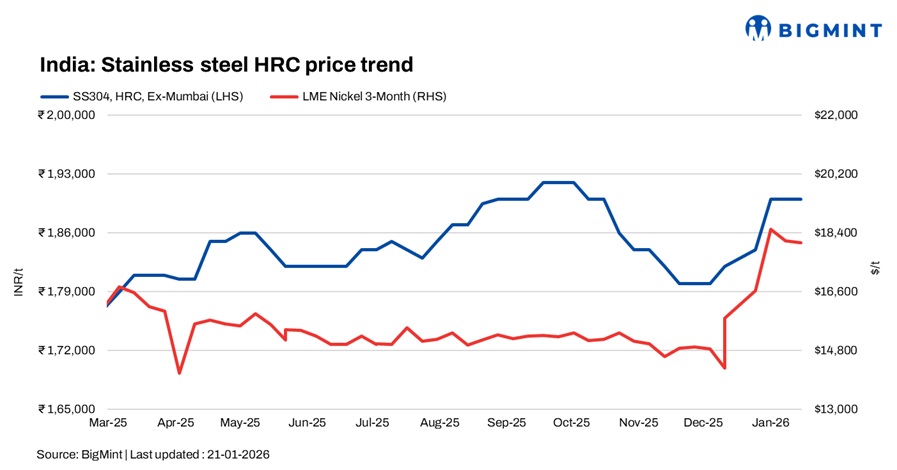

India’s stainless steel market remained firm on 21 January 2026, amid elevated global cost pressures, raw material volatility, and a strong US dollar. However, buying activity stayed cautious, with demand remaining limited.

Finished flats

The finished flats market maintained an upward trend, supported by a strong US dollar and firm global cues ahead of the Chinese New Year holidays. However, demand remained muted, with buyers staying cautious amid heightened price volatility. Imports continued to arrive, including non-licensed material, supported by the BIS compliance extension until 31 March.

BigMint’s benchmark assessment for 304 hot-rolled coils (HRCs) was at INR 190,000/t ex-Mumbai, while 316 HRCs stood at INR 336,000/t, both steady w-o-w.

A trader said prices have moved up, but buying interest remained limited as participants stayed in a wait-and-watch mode. Import activity also remained subdued, with some material facing delivery delays and clearance-related issues at Mumbai port.

Globally, Indonesia’s Tsingshan raised export prices for 304 stainless steel by a further $50/t on 16 January, marking the third hike this month and taking cumulative increases to $140/t. The producer also increased 316L prices by $100/t.

Meanwhile, Vietnam-origin 304 CR coil offers were heard at around $2,150-2,160/t (INR 197,000-198,000/t) CFR Nhava Sheva.

Finished longs

Finished longs prices stayed elevated on the back of higher raw material costs, but domestic demand remained sluggish. Market participants were largely cautious, with limited buying activity amid ongoing price volatility.

BigMint’s benchmark assessment for stainless steel 304L (25 to 100 mm) black round bars was at INR 163,000/t ex-Mumbai, up by INR 3,000/t. Meanwhile, SS 316L black round bars were at INR 280,000/t ex-Mumbai, up INR 2,000/t w-o-w.

Chinese stainless steel and NPI prices

In China, prices of domestic stainless steel 304-grade CRCs stood at RMB 14,850/t ($2,132/t) exw, while FOB tags of 304-grade CRCs were firm at $2,010/t. Indonesian FOB prices of nickel pig iron (NPI) (12-14%) were at $132/t, and NPI (10-12%) stood at $130/t.

LME nickel prices

Benchmark three-month contract nickel prices on the London Metal Exchange (LME) were at $18,070/t on 21 January, down slightly from $18,160/t in the previous week. LME-registered nickel stocks stood at 284,736 t, largely stable as compared to 284,658 t in the previous week.

Ferro molybdenum: Indian ferro molybdenum prices edged up by INR 35,000/t ($382/t) in comparison to the assessment on 14 January. Steady demand in the domestic market and global price hike were the key factors pushing prices.

Ferro molybdenum prices in India were INR 2,975,000/t ($32,494/t) exw-India, as per BigMint’s assessment on 21 January.

Ferro chrome: Indian high-carbon ferro chrome (HC60%) prices remained steady w-o-w at INR 105,700/t ($1,181/t) exw-Jajpur.

Odisha Mining Corporation (OMC) has scheduled an auction on 27 January for 3,000 t of high-carbon ferro chrome across multiple grades and sizes (Cr: 50-64%, 0-100 mm). The base price for the largest lot of 1,500 t (Cr: 60-64%, 10-100 mm) has been set at INR 104,500/t exw. Delivery of the material is scheduled within 30 days from the date of contract.

Ferro silicon: Indian ferro silicon (70%) prices remained largely stable, down by a minor INR 200/t ($2/t) as compared to the previous assessment on 12 January. Prices held steady, as market sentiment remained stable and neutral. Tight spot supply prevented significant price correction.

As per BigMint’s assessment on 19 January, ferro silicon prices in India were at INR 93,800/t ($1,031/t) exw-Guwahati. In Bhutan too, prices dipped by INR 200/t ($2/t) w-o-w to INR 93,700/t ($1,029/t) exw.

Ferrous scrap: India’s imported ferrous scrap market showed a firmer tone, supported by improved sentiment, though underlying demand remained selective. Offers from key origins strengthened, with HMS 80:20 largely indicated in the low-to-mid $330/t CFR, shredded around $350-355/t, and PNS near $360/t and above. Some EU-origin shredded offers tested higher levels, while West Coast India bids lagged. Buying interest improved on expectations of a March-April construction pickup, but price firmness was primarily driven by higher finished steel prices rather than a broad-based demand recovery.

Outlook

Stainless steel prices are expected to remain supported in the near term, backed by a strong US dollar, firm global cues, and continued cost-side pressure from nickel and alloy prices. However, upside may be capped by cautious buying interest and muted domestic demand

Leave a Reply