- Persistent overcapacity to keep margins under pressure

- Coke demand rise in 2025, supply far exceeds requirements

Mysteel Global: The elusive profitability that has frustrated China’s metallurgical coke sector in recent years is expected to continue pressuring the makers in 2026, with excess domestic capacity remaining the core of their problems, Mysteel predicts in its annual report on the commodity published recently.

With their businesses losing money for about three quarters of last year, the 30 merchant met coke makers under Mysteel’s nationwide survey recorded an average loss of Yuan 17.4/tonne ($2.5/t) on coke sales during 2025. Although this marked an improvement of Yuan 2.3/t from the previous year, the consecutive losses in two years still underscored the difficulty the coke makers face in restoring margins, a symptom of the entrenched overcapacity, the report stressed.

For full-year 2025, Mysteel calculated China’s pig iron output at around 900 million tonnes, higher by 22 million tonnes or 2.5% on year. The demand for coke, by extension, was correspondingly lifted to about 405 million tonnes, based on a coke ratio of 0.45 in pig iron production, according to the report.

In contrast, by the end of 2025 China had about 300 coking companies in operation, comprising 210 independent plants and 90 mill-affiliated ones, with a combined capacity of some 570 million tonnes/year, Mysteel’s survey showed.

“Against a backdrop of overcapacity, steelmakers hold the overwhelming advantage in price negotiations with coke producers,” the report said, adding that the latter often struggle to protect their profits.

Looking ahead into 2026, the report sees a net growth of 10.28 million t/y in met coke capacity being commissioned in North China’s Shanxi province, the country’s major coke producing region.

On the other hand, China’s pig iron output is expected to decline by 8-10 million tonnes this year, equivalent to a 3.6-4.5 million tonnes loss in met coke demand, Mysteel Global calculated based on the 0.45 coke ratio.

“Considering the multiple challenges facing China’s steel sector, including a persistent downturn in the domestic real estate market and mounting pressure on China’s steel exports, pig iron output is estimated to drop from 2025,” the report explained.

As the supply-demand relationship in the met coke market is set to slacken further, Chinese coke producers will continue to suffer from low margins this year, the report concludes. When pricing their products, coke producers will also rely more on cost support from the coking coal market.

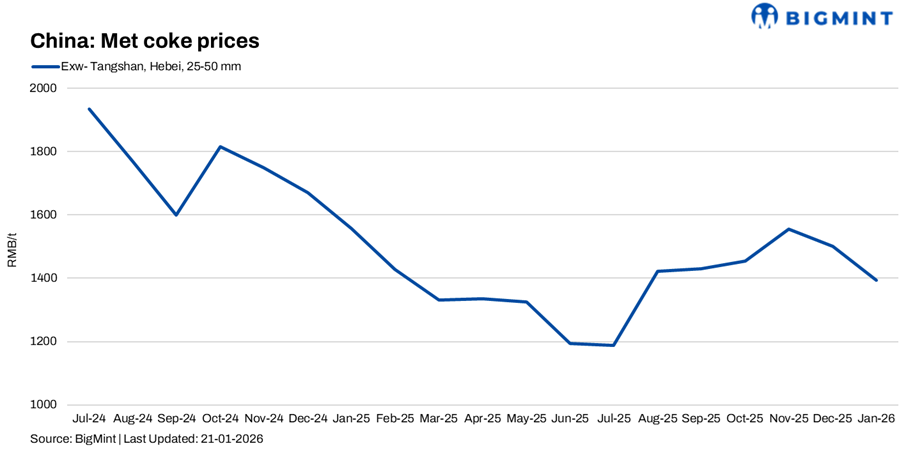

The report sees the price for quasi-first-grade dry-quenching met coke in Shanxi’s Lvliang city hovering around Yuan 1,500/t this year, fluctuating by around Yuan 300/t higher or lower. This compares with the average last year of Yuan 1,463/t, according to Mysteel’s assessment.

In comparison, the price for a premium domestic coal type, Anze low-sulfur primary coking coal produced in Shanxi’s Linfen city, is seen fluctuating in the range of Yuan 1,200-1,800/t, with an annual average of Yuan 1,400-1,450/t, according to another Mysteel report on coking coal.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply