- Persistent domestic shortages keep prices strong

- LME aluminium three-month prices decline by 0.8% w-o-w

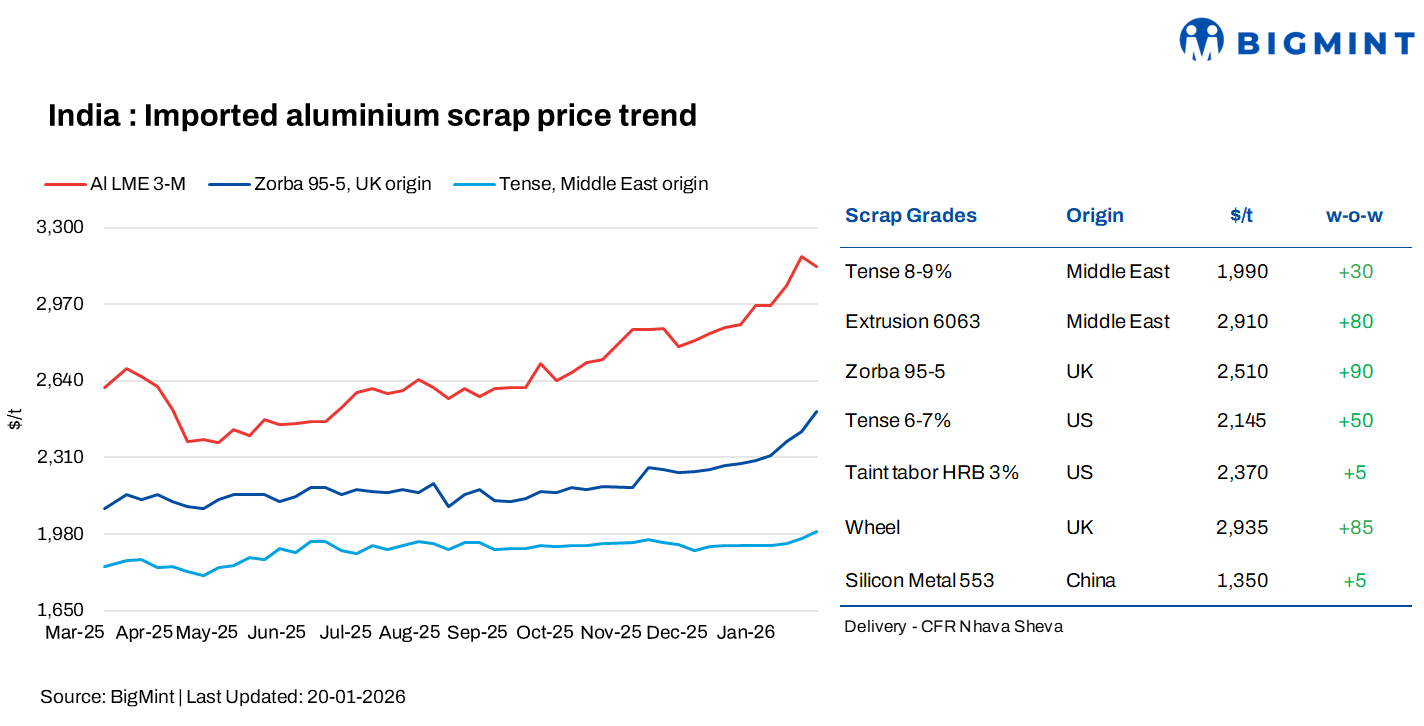

India’s imported aluminium scrap prices strengthened, as assessed on 20 January 2025, despite a decline in prices on the London Metal Exchange (LME). The uptrend was supported by steady buying interest, firm global aluminium sentiment and supply constraints. BigMint assessed Middle East-origin Tense (8-9%) at $1,990/t, up $30/t w-o-w, while Extrusion 6063 rose sharply by $80/t to $2,910/t amid improved demand.

UK-origin Zorba 95/5 increased $90/t to $2,510/t, while US-origin Tense (6-7%) gained $50/t to $2,145/t. US-origin Taint Tabor HRB (3%) edged up $5/t to $2,370/t, and UK-origin Wheel scrap advanced $85/t to $2,935/t.

LME aluminium prices ease

At close of trading on 19 January 2026, LME aluminium three-month prices declined by 0.8% w-o-w to $3,152/t from $3,177/t on 12 January 2026. Meanwhile, LME aluminium inventories fell by 2.2%, dropping 10,825 t from 495,825 t to 485,000 t, indicating continued drawdowns in visible stocks despite the price correction.

Aluminium prices rose w-o-w as supply-side tightness outweighed mixed demand signals. Market sentiment was underpinned by China’s strict enforcement of its 45-mnt smelting capacity cap, which constrained incremental supply even as domestic consumption showed signs of improvement. A sharp y-o-y decline in Chinese exports further tightened global availability, while delays and rising costs in overseas capacity additions–particularly in Indonesia–added to supply-side concerns.

Market scenario

The imported aluminium scrap market remained firm during the period, even as LME prices edged lower. Overseas offers stayed elevated, supported by tight global availability and firm seller expectations. While a small section of buyers was willing to accept higher prices to secure material amid supply constraints, most participants adopted a cautious, wait-and-watch stance. Elevated price levels, combined with sharp day-to-day volatility on the LME, increased price risk and dampened overall buying activity, resulting in limited spot deal closures.

A notable feature of the market was the wide bid-offer gap of around $40-50/t across several aluminium scrap grades, underscoring the persistent mismatch between seller expectations and buyer willingness. This divergence kept trading activity subdued, with buyers largely restricting procurement to immediate or contractual requirements. Uncertainty around near-term price direction further encouraged consumers to defer fresh commitments until greater clarity emerged.

On the import side, only selective transactions were concluded. Around 500 t of UK-origin Zorba 95/5 was purchased at $2,500/t, CFR Nhava Sheva. UK-origin Wheels scrap was heard bought at $2,880/t, CFR Nhava Sheva, while Saudi-origin Wheels scrap continued to command strong offers, with material indicated at around $3,000/t for delivery to Chennai and confirmed deals concluded at $2,970/t, CFR Mundra. The ongoing shortage of Wheels scrap across origins continued to provide firm price support, even as overall market activity remained muted.

Meanwhile, the domestic aluminium scrap market remained extremely tight, with supply shortages emerging as the key driver of prices. Availability of key grades was limited, particularly Tense scrap, leading to strong competition among buyers for spot material. Tense in Chennai continued to trade at a premium, with deals last week reported at INR 209-210/kg, reflecting the severity of the domestic supply crunch. In north India, Tense in Delhi was heard bought at around INR 206/kg for a small parcel of about 30 t, further highlighting tight availability across regions. Despite the dip in LME prices, persistent shortages in the domestic market kept prices firm and prevented any meaningful correction.

China silicon

According to BigMint, China-origin silicon metal 553 edged up by $5/t w-o-w to $1,350/t on a CFR Nhava Sheva basis, supported by firm demand from aluminium alloy producers amid tight availability.

Outlook

In the near term, India’s aluminium scrap market is expected to remain firm, supported by persistent supply constraints in both imported and domestic segments. Limited availability of key grades, especially Tense and Wheels, is likely to keep prices supported despite softness or volatility in LME aluminium prices.

Leave a Reply