- CR busheling prices mirror flat steel volatility through 2025

- Domestic supply improves but remains structurally short

- Policy support to steel and autos underpins late-year recovery

How has CR busheling evolved in India’s steel raw material mix?

India’s CR busheling scrap market has steadily moved from a niche industrial by-product segment to a strategically important input for flat steel producers. Generated from stamping, blanking and rolling losses at cold-rolling mills as well as automotive and appliance manufacturing units, CR busheling is prized for its low residual content, tight chemistry control and suitability for high-quality flat steel production. As mills push for better yield control and cleaner charge mixes, demand for prime industrial scrap has strengthened, elevating CR busheling’s role in procurement strategies.

Is domestic supply keeping pace with consumption?

In FY2025, India’s CR busheling consumption is estimated at 2.5-3 million tonnes, while domestic generation is assessed at around 2-2.8 million tonnes. The gap has been partially bridged by imports of about 0.2 million tonnes, primarily sourced from the United States and select European markets. Although domestic availability improved during the year, supply remained broadly tighter than demand, sustaining a premium over other scrap grades.

Higher scrap generation was supported by policy-led expansion in the automotive sector. Government incentives linked to vehicle scrappage, including concessional RTO registration for new vehicles and a GST reduction to 18% on eligible purchases, lifted auto sales and production. Increased stamping and processing activity translated into higher volumes of prime industrial scrap, helping reduce import reliance and reinforcing the domestic CR busheling market.

What drove CR busheling price movements in 2025?

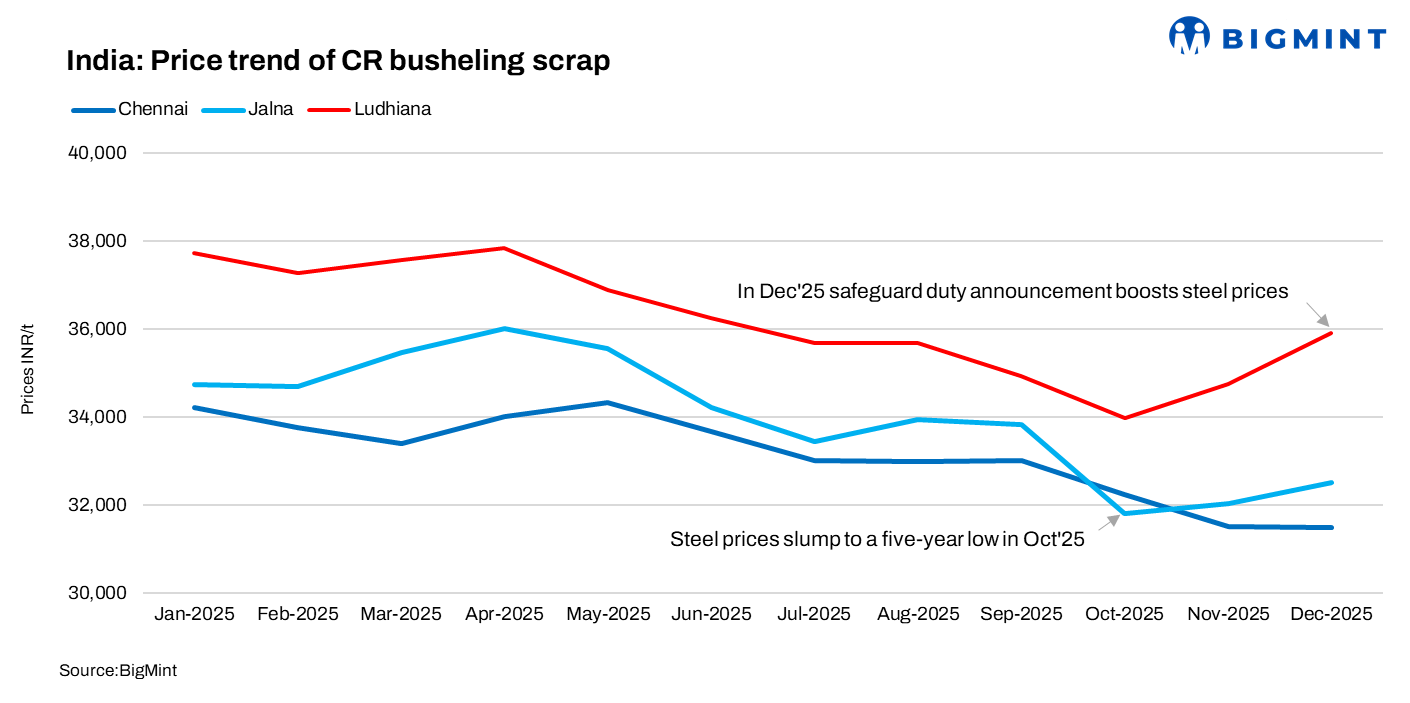

CR busheling prices followed a mixed trajectory in 2025, closely tracking swings in flat steel prices and mill purchasing sentiment. Early and mid-year movements reflected cautious buying amid uneven demand for finished steel. Market conditions deteriorated sharply in October, when CR busheling prices fell to near a five-year low, in line with a steep correction in domestic steel prices. Weak end-user demand, elevated inventories and margin pressure forced mills to curb scrap intake across key consuming regions.

Sentiment improved toward the end of the year. In December, domestic steel prices rebounded following the announcement of safeguard duties on Chinese steel imports, lifting mill realizations and restoring procurement appetite. The policy-driven recovery in flat steel spilled over into the scrap market, prompting restocking and firmer bids. By late 2025, CR busheling prices had stabilised at higher levels, supported by improved steel fundamentals and tighter spot availability.

Where is CR busheling supply concentrated?

Western India accounts for the largest share of CR busheling generation, led by Maharashtra and Gujarat, reflecting the concentration of automotive and engineering hubs. Northern India follows, supported by strong auto and white goods manufacturing clusters, while southern India contributes smaller but steady volumes.

Supply through the auction route remains largely OEM-driven and highly structured, providing mills with relatively transparent price discovery and predictable material flows. Large automotive OEMs dominate the auction landscape, including Maruti Suzuki, Mahindra & Mahindra, Tata Motors, Hyundai and Ashok Leyland, alongside a range of medium-sized OEMs and component manufacturers.

Maruti Suzuki is the single largest and most consistent supplier, typically auctioning around 5,000 tonnes of CR busheling each month through scheduled e-auctions. These sales often serve as a benchmark for pricing and sentiment across the prime scrap market. Other OEMs release material in clusters, aligning auctions with plant-level production cycles across western, northern and southern India. Engineering units also contribute via auctions, though volumes are smaller and less regular.

How did flat steel prices influence scrap dynamics?

Flat steel prices remained under pressure for much of 2025, shaping scrap buying behaviour. On a y-o-y basis, BigMint’s benchmark assessment for hot-rolled coils (IS2062, Gr E250, 2.5-8 mm/CTL) declined by INR 1,980/t to INR 49,280/t in 2025, compared with INR 51,260/t in 2024. Cold-rolled coil prices followed a similar trend, with the yearly average falling by INR 2,500/t to INR 56,200/t from INR 58,700/t a year earlier. Weak end-user demand and cautious optimism around policy interventions kept steel prices subdued for most of the year, limiting mills’ willingness to chase higher scrap costs until the late-year recovery.

What is the outlook for 2026?

Looking ahead to 2026, CR busheling demand is expected to rise further, supported by incremental flat steel capacity additions, higher electric arc furnace penetration and improving scrap segregation practices. Supply growth is likely to lag consumption, keeping the market structurally tight and supportive of prices. Upside risks remain during periods of strong HRC production or slower-than-expected industrial scrap generation.

At the same time, continued expansion in the automotive sector is set to reinforce domestic scrap availability. Policy incentives tied to vehicle scrappage and tax concessions are expected to sustain higher stamping activity, gradually strengthening the supply base. Even so, the balance is likely to remain finely poised, ensuring CR busheling retains its premium status within India’s scrap complex.

Leave a Reply