- Benchmark prices rise but weak demand prevents hikes in India

- Sankranti holidays, weak industrial activity slow down trading

Indian portside prices of Indonesian-origin thermal coal remained stable w-o-w during the week ended 17 January 2026, as subdued spot demand persisted across key calorific grades.

Market sentiment continued to be cautious, with buyers limiting purchases to immediate requirements amid weak industrial offtake and seasonal disruptions.

Price stability across key coal grades

According to BigMint’s assessments, prices of 5,000 GAR coal remained unchanged w-o-w at INR 7,200/t at Kandla and INR 7,100/t at Vizag, reflecting the absence of aggressive procurement activity. Similarly, 4,200 GAR coal prices were stable at INR 5,650/t at Kandla and INR 5,550/t at Vizag, as trading volumes remained thin.

Lower-grade 3,400 GAR coal prices also held steady at INR 4,450/t at Navlakhi, supported by consistent offtake from price-sensitive end-users, particularly in smaller industrial segments.

Weak industrial demand weighs on market activity

Market participants highlighted that coal buying in India remained slow, primarily due to reduced operating rates in downstream industries such as chemicals and textiles. Lower production levels have translated into softer coal consumption, prompting buyers to adopt a strictly need-based procurement approach, thereby limiting price movement despite higher international benchmarks.

Holiday impact, operational developments

Trading activity was further constrained by the Sankranti holiday period, which temporarily disrupted procurement. Additionally, operational challenges at Navlakhi eased as the weighbridge issue was resolved, with port operations resuming from the previous evening.

However, some supply-side constraints persisted, with loading delays reported in Indonesia due to heavy rainfall, limiting shipment availability but not yet exerting upward pressure on Indian portside prices due to weak demand conditions.

Freight market steady amid low cargo activity

Seaborne freights showed minimal movement during the week, mirroring the muted level of cargo bookings. BigMint assessed Supramax rates from East Kalimantan to Navlakhi at $10.80/dmt, down marginally by $0.21/dmt w-o-w, reflecting limited vessel demand and stable tonnage availability.

Portside coal inventories decline on improved evacuation

India’s portside thermal coal inventories declined by 2.3% w-o-w to 12.65 mnt in Week 2 of 2026, compared to 12.95 mnt in Week 1, as evacuation activity picked up following the holiday slowdown. While coal arrivals remained uneven across ports, faster dispatches at major locations resulted in a net drawdown, reversing the stability observed during the year-end period.

Power plant coal stocks remain adequate despite localised stress

Coal inventories at Indian thermal power plants increased marginally by 1.2% w-o-w to 53.56 mnt as of 14 January 2026, providing approximately 18 days of consumption cover. Although national stock levels remain comfortable, 16 power plants continue to operate under critical inventory levels, largely due to logistical constraints and coal quality mismatches, rather than any underlying supply shortage.

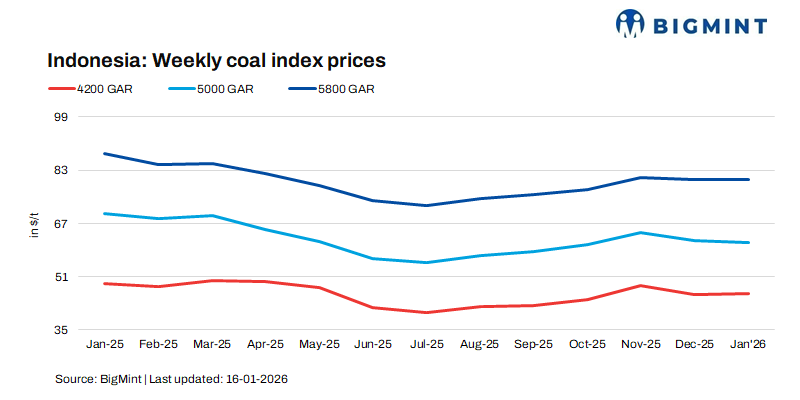

Indonesian benchmark prices edge higher, but immediate impact remains limited

Indonesia’s ESDM revised HBA thermal coal prices for the second half of January 2026, reflecting a broadly firm market on improving Asian demand and cautious miner supply. High-CV coal strengthened, with 6,322 kcal/kg GAR up 0.7% to $104.03/t, mid-CV 5,300 kcal/kg GAR (HBA-I) eased 0.87% to $71.61/t, while lower-grade 4,100 kcal/kg GAR (HBA-II) rose 2.8% to $48.39/t on cost-driven demand.

Indonesian weekly benchmark prices registered modest gains, with 5,800 GAR rising by $0.50/t, 4,200 GAR by $1.2/t, and 3,400 GAR by $0.35/t on a w-o-w basis. However, these increases have had limited pass-through into Indian portside prices, as cautious buying sentiment and sufficient domestic inventories continued to cap upside potential.

Outlook

Indian portside thermal coal prices are expected to remain stagnant in the near term, supported by stable global benchmarks but capped by weak industrial demand and ample inventories. Upside potential is limited until demand improves, while prolonged softness could place mild downward pressure, especially on higher-grade coal, if arrivals normalise.

Leave a Reply