- Aluminium demand remains resilient despite higher prices

- Domestic premiums rise to $290-300/t over LME cash prices

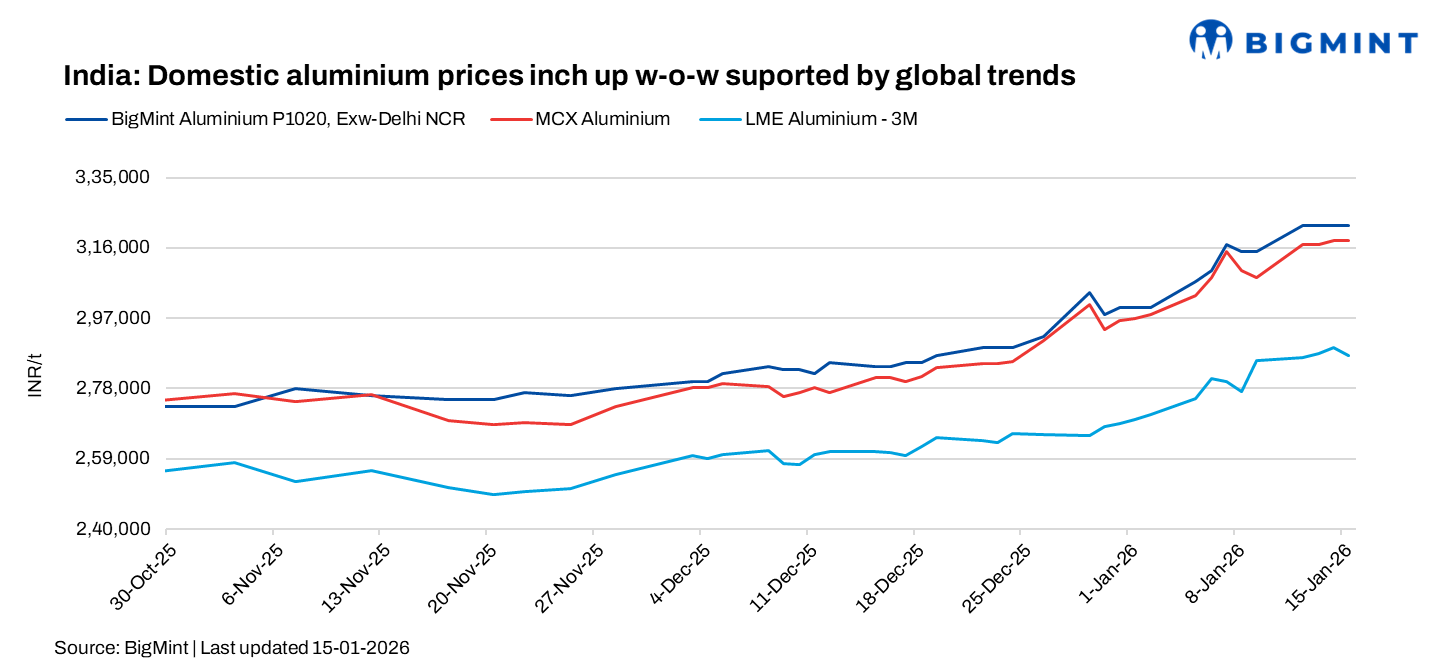

Domestic aluminium prices in India continued to strengthen w-o-w, supported by upward revisions from primary producers amid firm LME and MCX aluminium futures and ongoing global supply concerns. The price increase came despite adequate domestic availability and only moderate downstream demand, highlighting the continued influence of global market signals on local pricing.

According to BigMint’s assessment, domestic aluminium ingot prices in Delhi rose by INR 7,000/t, or 2%, w-o-w to INR 322,000/t, while Mumbai prices increased by INR 13,000/t, or 4.2%, w-o-w to INR 325,000/t as of 15 January.

How did Indian and global exchanges perform?

Domestic aluminium futures on the MCX remained stable on a w-o-w basis at INR 306,500/t as of 15 January, indicating a pause after recent gains amid steady spot market conditions.

In the global market, LME aluminium prices strengthened by $92/t, or 3.0%, w-o-w to $3,205/t, supported by firm sentiment and supply-side concerns. LME aluminium prices rose w-o-w as supply constraints outweighed mixed demand cues. Tight supply from China’s capacity cap, lower exports, delayed overseas expansions, and falling regional inventories continued to support market sentiment.

Meanwhile, LME warehouse stocks declined by 9,750 t, or 1.9%, w-o-w to 492,000 t, underscoring continued inventory drawdowns. The combination of stable domestic futures, higher global prices, and falling exchange stocks helped maintain a firm tone in the aluminium market.

Aluminium majors raise offers

The continued rise in domestic aluminium ingot prices was driven by successive upward revisions from primary producers during the period. BALCO raised its P1020 price from INR 332,000/t on 9 January to INR 340,000/t on 10 January, followed by further hikes to INR 342,000/t on 14 January and INR 344,500/t on 15 January, reflecting sustained pricing strength.

Hindalco also implemented steady increases, revising its P1020 price from INR 328,000/t on 9 January to INR 338,750/t on 10 January, then to INR 340,750/t on 14 January and INR 343,250/t on 15 January, underscoring firm producer confidence amid supportive market conditions.

Meanwhile, NALCO raised its P1020 price from INR 320,000/t on 7 January to INR 330,700/t on 14 January, an increase of INR 10,700/t, or 3.3%.

Market participants noted that sentiment in the domestic aluminium market has turned positive, with demand remaining healthy despite elevated LME prices. Inventories with major domestic producers were reported to be comfortable, supporting steady supply, while market activity continued to improve. Premiums strengthened to around $290-300/t above LME cash, reflecting better offtake and a firm order book. Participants added that, despite high LME levels, buying interest remains steady, indicating a gradual pick-up in overall market momentum.

Additionally, global primary aluminium production reached 67.49 mnt in 11MCY’25, up 1.1% y-o-y, although November output declined 3.3% m-o-m to 6.09 mnt.

Global aluminium developments

Saudi Arabia set to see major expansion

Saudi Arabia is set to become a major aluminium hub as PIF has partnered with Red Sea Aluminium Holdings to develop an integrated complex in Yanbu, featuring advanced smelting and continuous casting facilities. The project will produce high-value aluminium for domestic and international markets, boost industrial capabilities, attract investment, and focus on workforce development, positioning the Kingdom as a key player in global aluminium manufacturing.

Chinese production costs may ease in Jan’26

Meanwhile, China’s aluminium production costs are expected to ease in January 2026, driven by falling alumina prices, despite rising electricity costs. While auxiliary material costs may decline slightly, lower alumina costs will remain the main factor reducing overall production costs, supporting continued profitability across domestic operations.

Outlook

Domestic aluminium prices are expected to remain firm in the near term, supported by elevated LME prices, continued producer-led price revisions, and strong premium levels. While downstream demand may stay moderate, falling exchange inventories and sustained global supply constraints are likely to limit any sharp downside, keeping market sentiment positive.

Leave a Reply