- Capacity additions in Inner Mongolia to sustain oversupply in 2026

- Weak steel demand to cap prices despite rising raw material costs

Mysteel Global: China’s silico manganese (SiMn) market is expected to remain oversupplied in 2026, mainly due to planned capacity additions and ongoing weak demand, according to Mysteel’s latest forecast for the ferro alloy in its annual report.

New silico manganese capacity in North China’s Inner Mongolia is scheduled for commissioning this year, as smelters in this area can enjoy competitive smelting costs with low-cost electricity generated from green energy sources, the report pointed out, with about 2.78 million tonnes (mnt)/year of new silico manganese capacity expected to become operative there.

If this additional capacity comes online as scheduled, it may trigger an accelerated phase-out of small- and medium-scale producers, the report suggests. Less competitive smelters will face severe survival challenges, which may intensify industry consolidation and further widen the existing disparity in capacity distribution between northern and southern China, according to the report.

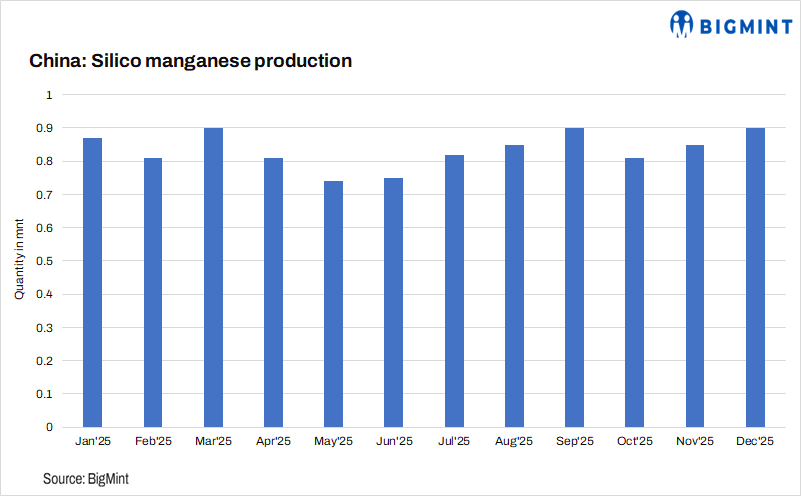

For 2025, total silico manganese production among the 187 Chinese smelters under Mysteel’s regular tracking reached 10.13 mnt, dipping by 0.2% from the previous year. The sampled smelters host 99% of China’s silico manganese smelting capacity.

Among the total, silico manganese output in Inner Mongolia increased by 1.2% y-o-y to 5.19 mnt last year, representing 51.2% of China’s total production, slightly higher than the ratio of 50.5% for 2024, Mysteel Global noted.

Silico manganese demand is expected to remain dull in 2026, due to the anticipated continued weakness in China’s steel market. For this year, China’s crude steel output is expected to continue its modest decline amid the country’s efforts to cut production capacity. Meanwhile, steel demand from the real estate sector may decline at a slower rate, but the sector remains a headwind, while the growth in steel use in the manufacturing sector is likely to cool, and steel exports pull back.

Robust supply and thin demand should keep Chinese silico manganese prices under pressure this year. However, the production cost of Chinese silico manganese smelters may increase with the higher prices of raw materials, including manganese ore and coke, the report pointed out. This may lend some support to China’s silico manganese prices from the cost side.

For 2026, China’s manganese ore prices are likely to remain firm as demand from domestic manganese alloy smelters is seen staying steady and offers from major overseas mines remaining generally high. At the same time, coke prices in China may recover this year on the back of the overall tight supply and the elevated production costs among coke makers.

After a rebound at the start of 2025, China’s prices of silico manganese and manganese ore declined steadily during the April-June quarter last year and then hovered at low levels in tandem with fluctuations in silico manganese futures prices, Mysteel Global noted.

At the end of 2025, Mysteel had assessed the national price of 6517 silico manganese at RMB 5,652/tonne ($811/t), including the 13% VAT, sliding by RMB 251/t from one year earlier.

In parallel, the price of South Africa-origin 36.5% grade Mn ore at North China’s Tianjin Port was assessed by Mysteel at RMB 35/dmtu, including the 13% VAT as of 31 December, higher by RMB 1.5/dmtu compared with the end of 2024.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply