- Coke prices rose in Eastern India, remained steady in the West, with muted market activity

- Australian coal rise may boost domestic coke, supported by pig iron and anti-dumping

The Indian BF-grade metallurgical coke market remained largely stable on a week-on-week basis in the week ended 14 January. Market activity was subdued, with limited spot transactions and cautious buyer participation, reflecting a wait-and-watch approach amid evolving raw material cost dynamics and seasonal factors.

Price movement

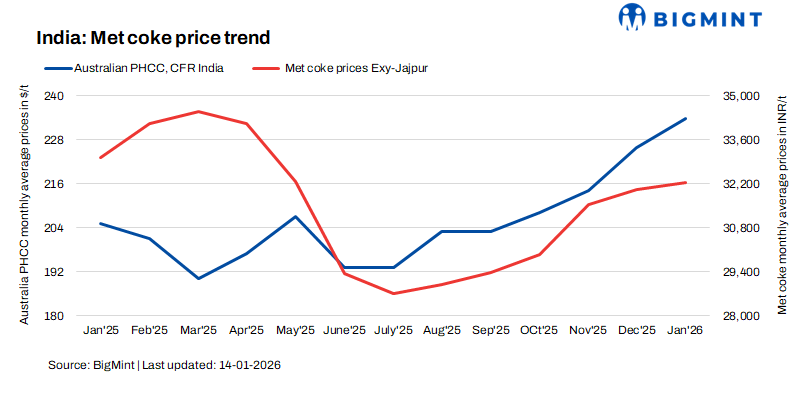

In eastern India, BF-grade metallurgical coke (25-90 mm) prices edged up marginally by INR 100/t to INR 32,300/t ex-Jajpur, supported by firmer input cost sentiment. Meanwhile, prices in western India remained unchanged at INR 30,100/t ex-Gandhidham.

“Imported Indonesian met coke prices have remained viable even after Anti Dumping imposition, hence import bookings have been concluded recently. Landed prices were heard in the range of INR 30,000-31,000/t.”, quoted sources.

Factors impacting Indian met coke prices –

- Demand and trading activity – Market participation remained muted, with no significant improvement in trade volumes. Buyers largely refrained from fresh commitments, relying instead on existing inventories. The market is expected to stay quiet in the near term, partly due to Sankranti-related holidays, which traditionally slow industrial activity and logistics.

- Coking coal prices surge w-o-w – Coking coal sentiment strengthened during the week, driven primarily by supply-side disruptions in Australia caused by adverse weather conditions. As a result, Australian premium hard coking coal (PHCC) prices increased by $10/t w-o-w to $228/t FOB Australia. While current met coke prices have not fully reflected this rise, higher coking coal costs are expected to exert upward pressure on coke prices once revised coal contracts are finalized. The impact of higher coking coal prices is anticipated to materialize in shipments arriving from late February to early March, suggesting a lagged pass-through to domestic coke pricing. In the interim, availability of older met coke stocks at relatively lower prices is limiting immediate price escalation.

- Chinese met coke prices stabilise – On 13 January, China’s metallurgical coke and coking coal markets remained stable. Steady mine output improved coal supply, but weak downstream demand and hand-to-mouth buying by steel mills kept prices flat, while futures-led trading activity did not alter near-term market fundamentals.

- Indian pig iron prices remain supportive – The Indian pig iron market offered notable support to the coke sector, with steel-grade pig iron prices ex-Durgapur rising by INR 200/t w-o-w to INR 36,700/t. Additionally, the imposition of provisional anti-dumping duties has improved sentiment in the domestic coke market, lending a degree of price stability despite weak spot demand.

Market outlook

The Indian BF-grade metallurgical coke market is expected to remain muted in January amid subdued trading and adequate low-cost inventories, though rising coking coal prices from Australian supply disruptions may provide cost support. Higher coking coal prices may give preference to coke purchases in the near term. With higher-priced coal shipments due from late February to early March, the medium-term bias remains cautiously positive, contingent on downstream demand.

Leave a Reply