- Wide bid-offer gaps to limit deal flow

- Buyers to stick to need-based procurement

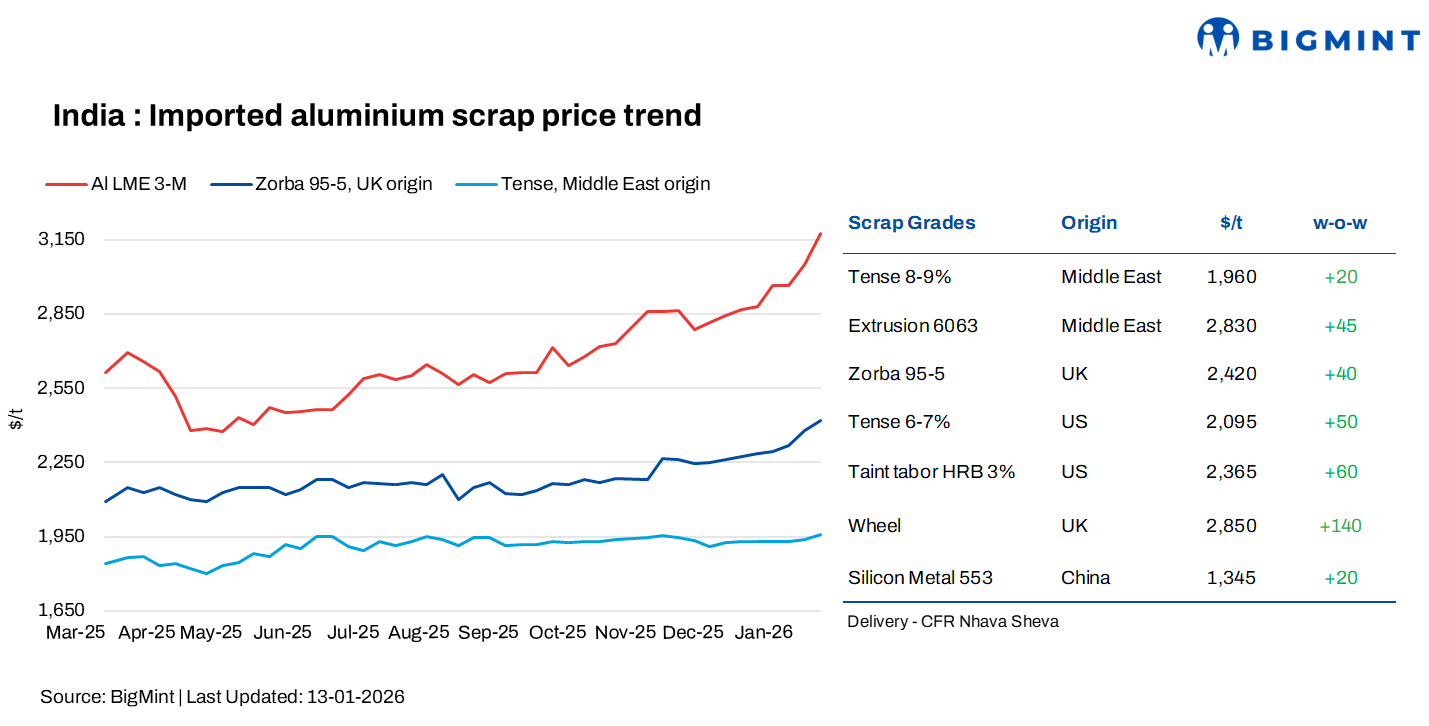

India’s imported aluminium scrap prices strengthened in the week ended 13 January, supported by a rise in prices on the London Metal Exchange (LME), steady buying interest and firm global aluminium sentiment. BigMint assessed Middle East-origin Tense (8-9%) at $1,960/t, up $20/t w-o-w, while Middle East-origin Extrusion 6063 rose $45/t to $2,830/t, driven by improved demand for higher-grade material.

Prices for UK-origin Zorba 95/5 increased $40/t to $2,420/t, while US-origin Tense (6-7%) gained $50/t to $2,095/t. US-origin Taint Tabor HRB (3%) climbed $60/t to $2,365/t, while UK-origin Wheel scrap saw a sharp rise of $140/t to $2,850/t, leading gains across grades.

LME aluminium climbs sharply as stocks edge lower

At the close of trading on 12 January 2026, LME aluminium three-month prices rose over 5% to $3,177.50/t, from $3,022.50/t on 5 January 2026. Meanwhile, LME aluminium inventories declined by 10,925 t, falling from 506,750 t to 495,825 t, indicating a drawdown in visible stocks alongside the price increase.

Aluminium prices gained w-o-w as supply-side tightness outweighed mixed demand signals. Market sentiment was supported by China’s strict enforcement of its 45 mnt smelting capacity cap, limiting incremental supply amid improving domestic consumption. Reduced Chinese exports, down sharply y-o-y, further tightened global availability. Delays and higher costs in overseas capacity expansion, particularly in Indonesia, added to supply concerns.

Market scenario

The imported aluminium scrap market remained under mixed sentiment, with overseas prices continuing to stay elevated. While a limited section of buyers was willing to match higher offers to secure material, the majority adopted a wait-and-watch approach, leading to slower buying activity. Elevated price levels increasingly strained purchasing appetite, restricting deal closures.

A defining feature of the market was the wide bid-offer disparity of around $40-50/t across several scrap grades, underscoring the gap between seller expectations and buyer willingness. This mismatch kept trading activity subdued, with most buyers refraining from aggressive spot purchases and limiting procurement to immediate requirements. Rapid day-to-day movements in the LME further amplified price risk, prompting consumers to delay fresh commitments until greater price clarity emerged.

A few deals were heard concluding in the imported aluminium scrap market. US-origin Taint Tabor was reported sold at around $2,280/t, while UK-origin Wheel scrap was heard traded in the range of $2,880-2,910/t. Meanwhile, UAE-origin Taint Tabor was indicated at levels of $2,450/t and above, reflecting firm seller expectations despite subdued overall market activity.

At the same time, demand for domestic aluminium scrap strengthened, as buyers increasingly shifted preference toward local material. Higher import prices and an unfavourable exchange rate made imported scrap less attractive on a landed-cost basis. This shift resulted in tighter domestic scrap availability, as more buyers competed for limited local supplies. Tense scrap, in particular, remained scarce, sustaining firm demand and providing strong price support in the domestic market. Secondary aluminium producers increasingly favoured domestic sourcing due to faster availability, reduced logistical uncertainties, and greater procurement flexibility.

Middle East-origin Taint Tabor and Extrusion 6063 continued to witness weak buying interest, as sellers held firm offers reflecting higher replacement costs, while buyers resisted chasing prices higher, resulting in minimal deal closures.

Adding to the overall slowdown, market activity in Punjab was largely muted, with trading nearly at a standstill due to the Lohri festival, further constraining spot market participation. Overall, the aluminium scrap market remained cautious, weighed down by elevated prices, currency pressures, volatile global cues, and seasonal factors, even as domestic scrap prices held firm amid tight supply conditions.

China silicon

According to BigMint, China-origin Silicon Metal 553 rose $20/t to $1,345/t w-o-w on a CFR Nhava Sheva basis. Prices rose due to tight supply from power and environmental curbs, higher energy costs, and steady demand from aluminium alloy producers, prompting sellers to raise offers.

Outlook

In the near term, imported aluminium scrap prices are likely to remain firm but range-bound, supported by strong LME aluminium prices, declining global inventories, and continued supply-side constraints. However, buying activity may stay cautious due to elevated price levels, wide bid-offer gaps, and exchange-rate pressures. Demand is expected to tilt further toward domestic scrap, keeping local prices supported amid tight availability, while imported volumes could remain selective until price stability improves.

Leave a Reply