- Netherlands emerges as India’s top supplier

- Saves scrap remains dominant imported grade

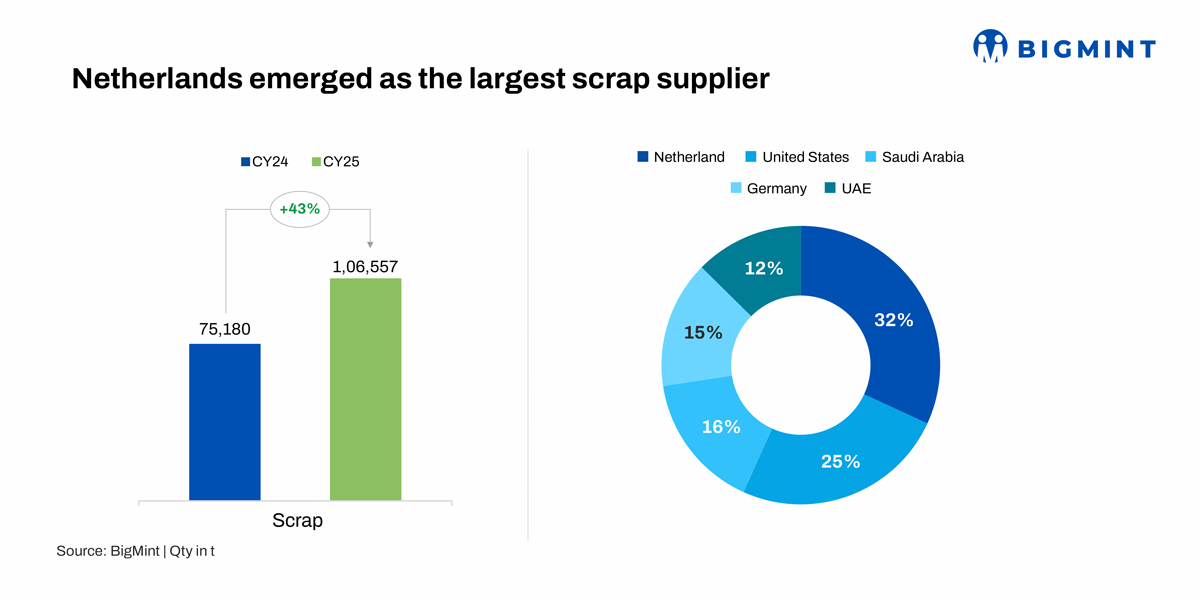

India’s zinc scrap imports increased sharply by 43% y-o-y in calendar year 2025 (CY’25) to 106,556 tonnes (t), compared with 75,180 t in CY’24, highlighting the expanding role of secondary zinc smelters in meeting domestic demand. Elevated zinc prices encouraged buyers to prioritise cost efficiency and flexible feedstock, resulting in higher intake of mixed and industrial-grade scrap. The rise also reflects broader sourcing diversification amid uneven global scrap availability.

Grade-wise zinc scrap imports

India’s zinc scrap imports increased across most grades in calendar year 2025 (CY25), reflecting firmer secondary zinc demand and improving processing economics. Saves (old zinc die-cast scrap) and Score (zinc sheet scrap) continued to dominate the import mix. Saves imports rose 33% year on year to 69,648 t, reinforcing its position as the preferred feedstock for secondary zinc producers. Score volumes climbed 61% y-o-y to 24,220 t, supported by favourable processing margins and steady overseas availability. Scroll-grade imports reached 7,442 t, pointing to greater acceptance of lower-grade material amid cost considerations. By contrast, Screen-grade imports declined 14% y-o-y to 1,859 t, reflecting more selective procurement due to higher impurity levels.

Top supplying nations

The Netherlands emerged as the largest incremental supplier, with shipments nearly doubling, up 113% y-o-y to 15,404 t, supported by steady scrap availability across the EU. The United States remained a key origin, with imports rising 47% y-o-y to 12,017 t on the back of consistent export flows.

Saudi Arabia supplied 7,660 t, up 22% y-o-y, reflecting stable Middle East trade routes. Germany recorded a 40% y-o-y increase to 7,156 t, aided by improved collection and export activity, while UAE shipments grew 30% y-o-y to 6,091 t, supported by regional re-export flows.

Collectively, these top five suppliers accounted for 59,376 t in CY’25, up 48% y-o-y from 40,068 t in CY’24, underlining India’s increasingly diversified sourcing strategy.

Scrap vs ingot context

Primary zinc ingot imports (semi-finished) are estimated at around 251,792 t for CY’25, up from prior years on galvanising demand. With scrap at 106,556 t, the scrap-to-ingot ratio neared 42%, showing secondary feed increasingly complements primary supplies without displacement.

Physical demand, policy impact

End-user demand from galvanising, alloy, and die-casting sectors supported the import uptick, with Q4’25 restocking occurring despite LME price volatility. Policy measures included the nil-duty regime on non-ferrous scrap-covering zinc waste and scrap (HS 7902)-set at 0% BCD from February 2025 under Union Budget 2025-26, which lowered landed costs for Saves and Score grades. Capacity expansions, including Hindustan Zinc’s INR 12,000 Cr investment adding 250 KTPA refined zinc capacity and new galvanising lines, increased secondary feedstock requirements. Preparatory compliance with EU Waste Shipment Regulation helped maintain scrap supplies from Netherlands (15,400 t) and Germany (7,150 t), while the EPR mandate for non-ferrous metals (effective April 2026, targeting 25% recycled zinc by 2031) influenced CY’25 import levels.

Zinc LME and scrap price trends in CY’25

Zinc prices on the London Metal Exchange (LME) strengthened on a y-o-y basis in CY’25, supported by firm price momentum in the second half of the year and a sharp contraction in exchange inventories. The LME 3-month zinc price averaged higher in CY’25, with prices recovering from mid-year weakness and closing the year near $3,090/t, compared with levels largely below $2,900/t during most of CY’24. This price firmness coincided with a significant drawdown in LME zinc stocks, which fell sharply through CY’25, dropping below 80,000 t by year-end from over 250,000 t during CY’24, lending strong underlying support to prices.

In line with higher LME zinc prices, imported zinc scrap prices also increased y-o-y in CY’25. As per BigMint’s assessment , average imported zinc diecast scrap prices (attachment 4-5%, CFR West Coast India) rose 7% y-o-y to $2,235/t in CY’25, compared with $2,089/t in CY’24. Prices gained momentum in the second half of CY’25, tracking the rally in refined zinc and tightening scrap availability.

Despite the rise in imported scrap prices, buying interest remained intact, as shrinking global inventories and firmer refined zinc prices supported scrap valuations. Market participants noted that zinc scrap prices closely tracked LME movements through the year, with inventory-led price strength playing a larger role than demand-side pressures in shaping the CY’25 trend.

Outlook

India’s zinc scrap imports could exceed 120,000 t in CY’26, fueled by industrial growth and EPR-compliant recycling push. Buyers will likely deepen ties with EU (Netherlands/Germany), Middle East, and US sources while monitoring US export curbs and SHFE scrap flows.

Leave a Reply