- Export demand mixed, Pakistan, India show resistance to UAE’s offers

- Some UAE sellers intend to stay on sidelines until new tax system kicks in

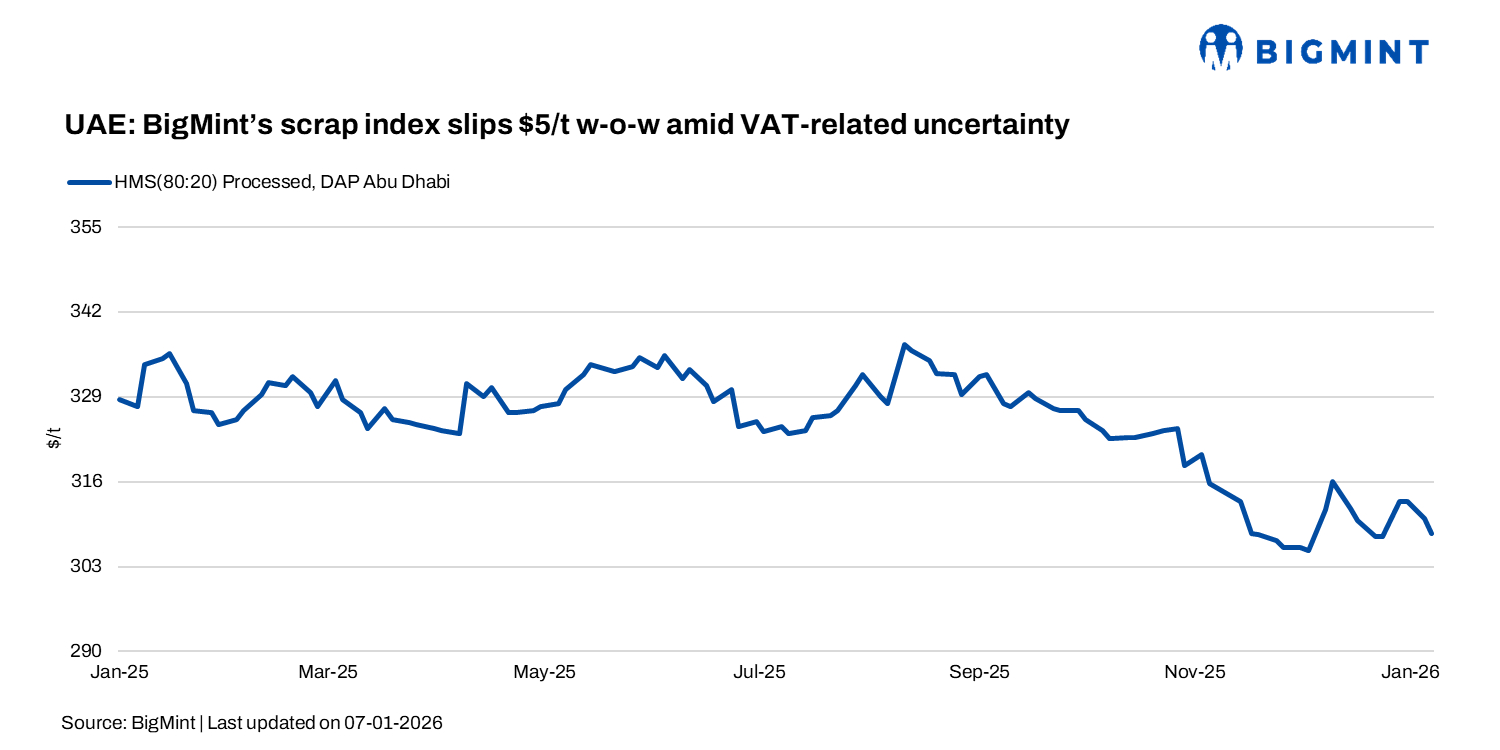

UAE’s scrap prices dropped w-o-w on 7 January during the first week of 2026 due to muted trade during the year-end. The processed heavy melting scrap (HMS) index fell AED 18/t ($5/t) w-o-w to AED 1,132/t ($308/t). Procurement remained selective, with Pakistani and Indian buyers deeming Middle East’s export offers as being too high.

Following the announcement of the VAT reverse charge mechanism on domestic scrap metal trading from 14 January, some suppliers indicated that they are now sharing prices on a VAT-exclusive basis. However, others stated that they would stay on the sidelines until 13 January, as they need further clarity on prices.

Market updates

As per market insiders, processed HMS was heard in the range of AED 1,120-1,140/t ($305-310/t), while HMS 80:20 was indicated near AED 1,050/t ($286/t). Shredded scrap was quoted at around AED 1,170-1,180/t ($319-321/t), with processed PNS assessed at AED 1,130-1,150/t ($308-313/t). Latest market chatter broadly placed processed HMS at AED 1,130-1,140/t ($308-310/t).

DAP Abu Dhabi indications

- Processed HMS: AED 1,130-1,140/t ($308-310/t)

- Shredded: AED 1,180-1,190/t ($321-324/t)

- PNS: AED 1,140-1,160/t ($310-316/t)

- Pure LMS: AED 950-1,000/t ($259-272/t)

Export market

Export market participants reported a few spot deals from the UAE, indicating mixed buying interest across South Asia. Low-grade auto HMS from the Middle East was sold at around $325/t CFR Mundra for a 500-t parcel, while HMS 90:10 was heard concluded near $355/t CFR Qasim for similar volumes.

Market chatter suggests Middle East auto HMS was offered in the $325-330/t CFR Mundra range, with good-quality pure LMS at $310-315/t CFR Mundra.

For Pakistan, UAE HMS 90:10 was discussed at around $355-358/t CFR, while UAE-origin shredded was indicated near $370/t CFR Qasim and HMS sheared at $350-355/t CFR Qasim.

Outlook

The UAE’s scrap and steel markets are likely to remain subdued next week, as mills continue to adopt a wait-and-watch stance amid policy and pricing uncertainty. Evolving clarity around the application and treatment of VAT in scrap transactions is prompting both buyers and suppliers to delay firm price revisions, with cautious procurement and limiting near-term momentum.

Leave a Reply