- Billet prices surge INR 1,700/t w-o-w as demand improves

- Recent slowdown in import activity aids scrap price uptick

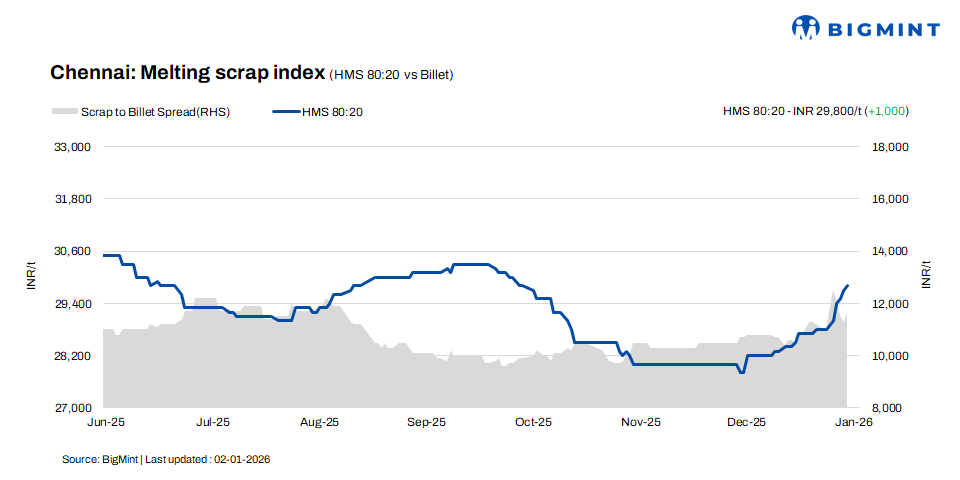

HMS (80:20) prices in Chennai increased by INR 1,000/tonne (t) w-o-w to INR 29,800/t, according to BigMint’s latest assessment on 2 January 2026, supported by a mild d-o-d rise of INR 100/t.

Billet prices improved by INR 500/t d-o-d to INR 41,500/t while registering a cumulative increase of INR 1,700/t w-o-w. Similarly, rebar prices also rose by INR 1,500/t w-o-w to INR 45,500/t while increased by INR 500/t d-o-d. The recent improvement in trading activity for semi-finished and finished steel pointed to a positive shift in overall market sentiment.

Imported, domestic price trends

Market participants indicated that imported shredded scrap was offered at $340-345/t CFR Chennai, while HMS (80:20) was quoted at $320-325/t. Buyers bid $5-8/t lower. Buying interest remained subdued, as domestic scrap prices continued to offer better cost viability than imported material, thereby limiting fresh bookings.

HMS (80:20) prices in the domestic market were quoted at INR 29,500-30,000/t for spot deals with immediate payment. Transactions involving extended payment terms were concluded at higher levels of INR 30,000-30,500/t. Market activity remained largely concentrated within the INR 29,500-30,500/t band.

Buyer-supplier sentiments

According to sources, the steel market witnessed a positive shift in the week ended 2 January. Sponge iron prices in Chennai improved, supported by higher offers from neighbouring states. Billet demand picked up in the region, while rebar trade improved in the retail segment, although project-based demand remained relatively subdued. Finished steel inventory levels declined, currently estimated at around 10-15 days. Meanwhile, major market players started offering billets in the market to balance and manage their finished steel inventories.

A scrap supplier indicated that HMS (80:20) prices hovered in the range of INR 28,500-29,500/t, with variations driven by payment terms and mill-specific volume requirements. Strengthening billet and sponge iron prices lent support to the scrap market. Moreover, subdued imported scrap activity over the past few months has further aided the upward momentum in domestic scrap prices.

Regional comparison

In the western India-based Jalna market, billet prices increased by INR 1,000/t d-o-d to INR 43,800/t, while rebar prices rose by INR 400/t to INR 50,000/t. Meanwhile, HMS (80:20) scrap prices edged down by INR 100/t d-o-d to INR 30,600/t.

According to market sources, trading activity in steel products has improved over the past couple of days. The inventory build-up in finished steel, which had earlier exerted selling pressure on mills, has largely been cleared. However, scrap prices did not mirror the gains seen in semi-finished and finished steel, as mills continue to receive sufficient scrap supplies to sustain operations.

Outlook

According to market sources, scrap prices are expected to either remain stable or witness marginal upside in the coming days, supported by recent improvements in prices of other steel products. Any price uptick is likely to be limited to a narrow range of around INR +/- 200-500/t.

Leave a Reply