- Ample inventories, rising use of NPI limit mills’ scrap intake

- Strengthening nickel prices offer limited cost-side support

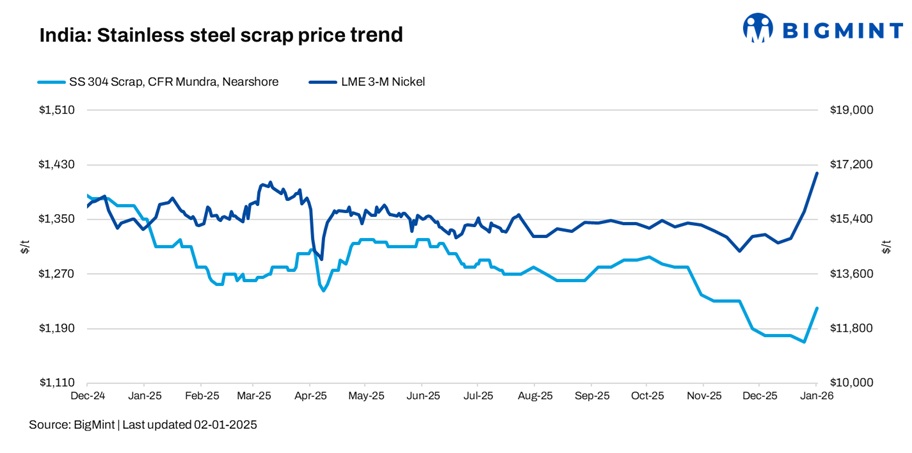

India’s stainless steel scrap market remained weak during the week ended 2 January, as major mills slowed procurement due to comfortable inventory positions and increased usage of cost-effective substitutes such as nickel pig iron (NPI). Buying interest also remained selective due to the New Year holidays, keeping overall market sentiment subdued. However, rising nickel prices provided limited cost support to stainless steel.

A leading stainless steel producer, which had suspended scrap purchases across all plants since mid-November amid inventory accumulation and NPI availability, reportedly resumed buying from one facility. However, traded volumes were marginal, according to sources.

Domestic 304-grade stainless steel scrap prices were assessed at INR 104,000/t DAP Delhi, unchanged w-o-w. Imported 304-grade scrap from nearshore origins was assessed at $1,220/t CFR Mundra, up $50/t w-o-w, supported by rising nickel prices.

In the imported segment, market participants largely adopted a wait-and-watch approach as European markets remained closed due to the New Year holidays. Market participants also expected further price gains, linked to the recent strength in nickel.

BigMint’s scrap assessments

- Nearshore-origin SS 316 scrap (loose): $2,430/t, up $50/t w-o-w.

- Nearshore-origin SS 201 scrap (loose): $640/t, up $20/t w-o-w.

- Nearshore-origin SS 430 scrap (loose): $560/t, steady w-o-w.

- SS 316 scrap, DAP Delhi: INR 205,000/t, steady w-o-w.

- SS utensil, DAP Delhi: INR 58,000/t, steady w-o-w.

Global sentiment remains under pressure

Global stainless steel scrap markets continued to face pressure, led by persistent oversupply and weak mill demand, particularly in the US. Low stainless steel consumption and steady scrap inflows resulted in elevated inventories at scrap yards, forcing processors to cut 304-grade scrap prices to multi-year lows in mid-December.

The seasonal slowdown in mill buying began earlier than usual this year due to weaker finished steel demand. Although stainless steel mills typically raise scrap intake in Q1CY’26, market participants remained doubtful about a strong rebound amid continued nickel price volatility and abundant global nickel supply. Overall sentiment remains bearish to cautious, with limited upside visibility.

LME nickel supports cost sentiment

Benchmark three-month contract nickel prices on the London Metal Exchange (LME) were at $16,930/t on 2 January, up by 8% from $15,650/t in the previous week. LME-registered nickel stocks stood at 255,162 t, a marginal 0.2% decrease compared to the 255,696 t in the previous week.

Outlook

India’s stainless steel scrap market is currently in a consolidation phase following the earlier rally seen in past months. While underlying fundamentals remain unchanged, buying is expected to stay cautious in the near term due to stable supply conditions and mills’ reliance on alternative raw materials. Any meaningful price upside will likely depend on a sustained recovery in stainless steel demand and clearer global commodity cues.

Leave a Reply