- India scrap firms on stronger steel prices

- Pakistan subdued amid weak utilisation, year-end slowdown

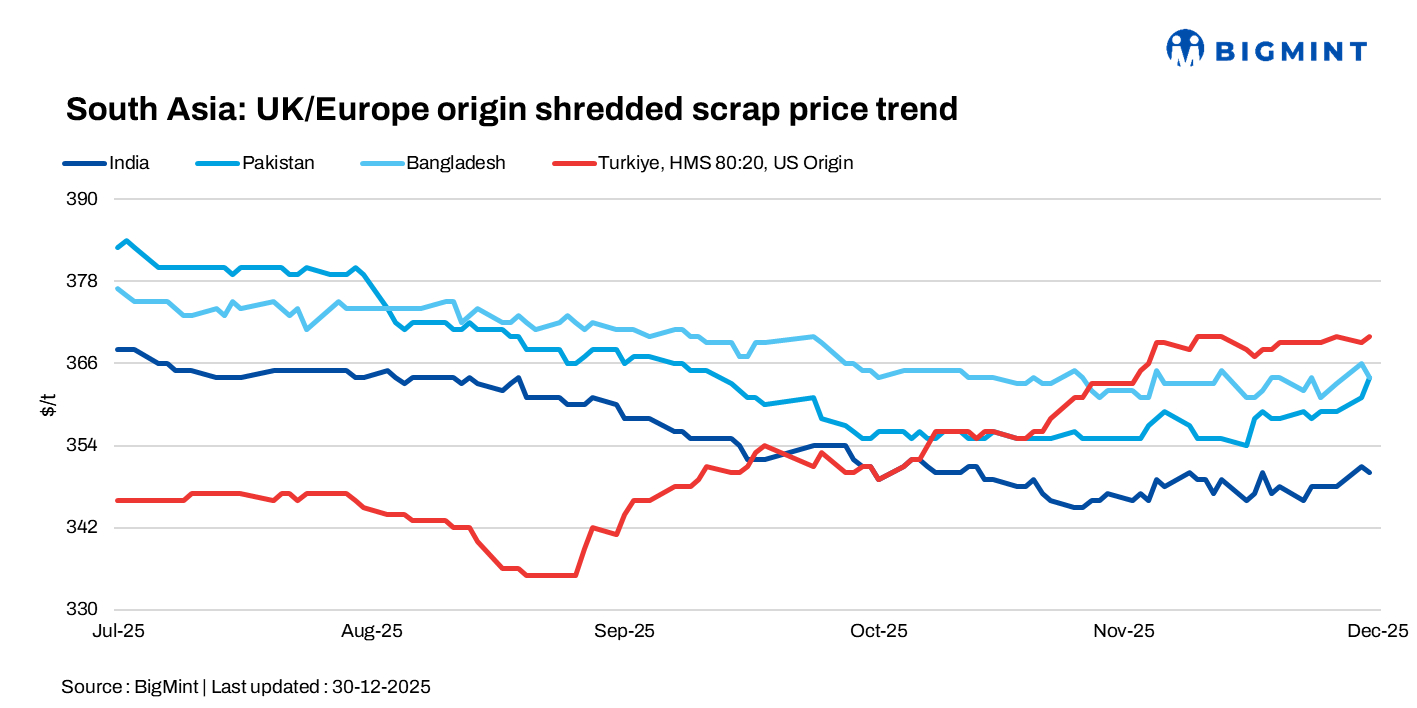

South Asia imported scrap markets showed mixed sentiment, with India firming on stronger domestic steel prices, while Pakistan and Bangladesh remained subdued due to weak buying interest. Turkiye prices edged up on US-origin deals, supported by expectations of tighter supply and firmer January settlements.

India: Imported scrap market sentiment remian firm d-o-dy basis, with prices moving up since the last close and expectations building that the week may trend higher across scrap grades. The uptick was driven by stronger domestic rebar and billet prices and some scrap tightness, prompting buyers to exit the wait-and-watch mode and actively chase mid-level offers.

Workable offers included Senegal HMS 80:20 at around $340/t CFR Mundra, Kuwait HMS 90:10 at $355/t CFR Mundra with offers up to $360/t, Ireland and Poland HMS (around 2% impurities) near $340/t CFR Mundra, Brazil HMS (around 3% impurities) at about $327/t CFR Mundra, Malaysia turnings at $305/t CFR Chennai.

Pakistan:Imported scrap market remained largely quiet, with assessed prices hovering at subdued levels amid year-end slowdowns. Shredded scrap offers were heard in the range of $366-378/t, though workable levels were closer to $360-362/t, mainly quoted by middlemen, as mill buying interest stayed weak. With mill utilisation down to around 40%, the market was described by participants as almost closed, limiting fresh transactions and keeping activity minimal.

Bangladesh: The imported scrap market in Bangladesh remained sluggish, with mills showing limited buying interest during the day. Offers for Australian-origin shredded scrap were heard at $360-362/t CFR, while PNS from Singapore and Hong Kong was quoted at $360-366/t CFR.

Turkiye: Deep-sea imported scrap prices firmed on December 30 after a US-origin HMS 80:20 deal concluded on Christmas Eve, with US-origin levels heard around $370/t and European-origin cargoes at $363-366/t. Market participants expect further firmness in January, supported by higher domestic prime scrap settlements and tightening availability, as European mills may be forced to raise prices after keeping them unchanged for an extended period.

Leave a Reply