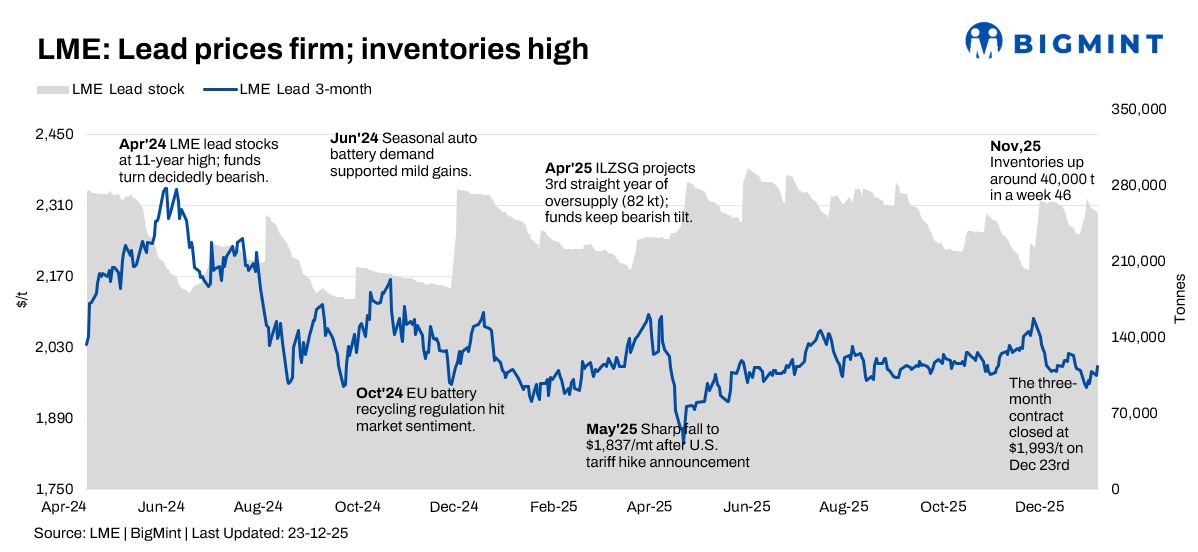

- LME lead inventories stay high in absolute terms

- Honda to buy out LG Energy’s Ohio EV battery plant

The global lead market was subdued during 22-26 December 2025, with Christmas‑related closures and year‑end position‑squaring keeping liquidity light. Price action on the London Metal Exchange (LME) was broadly sideways after earlier December weakness, as traders waited for clearer signals on battery demand and Chinese activity going into the New Year.

Price trends

LME lead prices moved within a narrow band through the week. Cash lead averaged around $1,925/t, while the three-month contract traded near $1,970/t. Cash prices edged up from approximately $1,920/t on 22 December to $1,930/t by 26 December, marking a w-o-w gain of about 0.5%.

Over the same period, the three-month price increased from around $1,960/t to $1,975/t (0.8% w-o-w). The forward curve remained in mild contango.

Inventory analysis

LME lead inventories stayed high in absolute terms and eased only marginally during the week. Exchange stocks declined from around 265,600 t on 22 December to approximately 258,600 t by 26 December, a draw of roughly 7,000 t (2.6% w-o-w).

Despite the modest reduction, visible stocks remain in the mid-250,000-t range, equivalent to several weeks of global refined lead consumption. This inventory overhang continues to weigh on market sentiment and limits upside potential, even as prices stabilise.

MCX lead trends (22-26 December)

On India’s MCX, lead futures mirrored the subdued tone on the LME, albeit with a slight upward bias. The near-month 31 December contract settled at INR 181,800/t on 22 December and edged up to INR 183,100/t by 26 December, registering a w-o-w gain of around 0.7%.

Prices traded within a narrow INR 181,000-183,000/t range, reflecting balanced domestic fundamentals–steady replacement battery demand offset by adequate refined supply and imports. Thin participation weighed on activity, with volumes falling from 190 lots on 22 December to 107 lots by 26 December, while open interest declined from 284 to 195 lots as traders rolled or squared positions into year-end. On a one-month basis, MCX lead remains marginally weaker, echoing the earlier global correction rather than indicating a deterioration in local fundamentals.

SHFE lead

On the Shanghai Futures Exchange, the most-active February 2026 lead contract traded at around CNY 15,800/t, up approximately 1% w-o-w. The SHFE/LME lead arbitrage hovered close to parity, implying near-neutral import economics and limited incentive for significant cross-border refined lead flows.

LG Energy Solution cancels $2.7 bn battery contract

South Korea’s LG Energy Solution has mutually terminated a 3.9 trillion won ($2.7 billion) battery supply deal with Freudenberg after the US firm exited the battery business. This follows Ford’s recent cancellation of a 9.6 trillion won contract, hitting LGES’s backlog.

Honda to buy out LG Energy’s EV battery plant

Honda Motor Co. will acquire LG Energy Solution’s Ohio EV battery plant assets for about 4.2 trillion won ($2.9 billion), reflecting slowing US electric-vehicle demand. The deal, set to close by February 2026, aims to boost operational efficiency amid broader EV market challenges.

Outlook

Heading into early January, LME lead prices are expected to remain range-bound, with elevated exchange inventories and modest battery demand capping upside. However, tighter Chinese inventories, maintenance-related supply disruptions, and pre-Lunar-New-Year restocking should provide upside support, keeping market focus firmly on inventory drawdowns and demand trends in the weeks ahead.

Leave a Reply