- Chennai billet prices gain INR 300/t w-o-w

- Steel prices show positive shift in Chennai

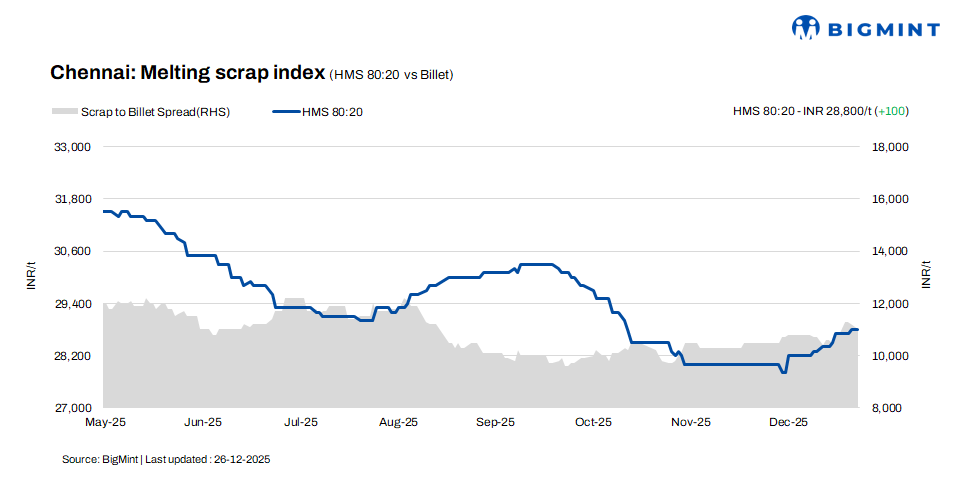

HMS (80:20) scrap prices in Chennai recorded a w-o-w increase of INR 100/t, reaching INR 28,800/t, according to BigMint’s latest assessment on 26 December. However, prices remained stable on a d-o-d basis. billet prices rose by INR 300/t w-o-w, reaching INR 39,800/t, but experienced a d-o-d decrease of INR 200/t. Rebar prices saw an increase of INR 700/t w-o-w, reaching INR 44,000/t, with no change on a d-o-d basis. The recent improvement in trade activity for semi-finished and finished steel indicated a positive shift in the market.

Imported and domestic price trends

Market participants indicated that imported shredded scrap was offered at $338-340/t CFR Chennai, while HMS (80:20) scrap was quoted at $318-320/t. Buyers were bidding slightly lower by $5-10/t. Buying interest remained subdued, as domestic scrap prices continued to offer better cost viability compared with imported material, thereby limiting fresh bookings.

In the Chennai market, domestic HMS (80:20) scrap is trading at INR 28,000-29,000/t for spot deals with immediate payment, while extended credit transactions are fetching higher levels of INR 29,000-29,500/t. Most market activity remains concentrated within the INR 28,500-29,500/t range, underlining the impact of liquidity pressures and the prominence of credit-driven pricing in the scrap market.

Buyer-supplier sentiments

A mill representative indicated that sponge iron prices have strengthened, primarily due to restricted supply in the merchant market, as major producers continue to channel production towards captive consumption. Meanwhile, billet and rebar offers have also shown improvement, supported by better demand for finished steel compared with the past couple of weeks. Finished steel inventories have eased notably from levels seen in recent months and are currently assessed at approximately 15-20 days.

A scrap supplier indicated that HMS (80:20) scrap prices are presently hovering in the range of INR 28,500-29,500/t, with variations driven by payment terms and mill-specific volume requirements. Reduced imported scrap inflows over the past few months, due to viability challenges, have provided support to domestic scrap prices. Moreover, improved liquidity conditions in recent days have contributed to a more positive market outlook.

Regional comparison

HMS (80:20) scrap prices in the Jalna market of western India were assessed unchanged at INR 29,600/t. Meanwhile, billet prices rose by INR 200/t to INR 40,300/t and rebar prices inched up by INR 100/t to INR 45,700/t.

Scrap offers in the region largely remained stable, while finished steel prices improved by INR 1,000-1,500/t in past couple of weeks. Despite this improvement, mills have kept their scrap purchase prices unchanged as they aim to maintain conversion margins, which had earlier narrowed.

Outlook

Market participants expect domestic scrap prices to remain stable in the near term, supported by firm supplier offers and relatively higher prices of imported scrap and sponge iron. Any short-term price movement is likely to be limited to INR 200-500/t, keeping overall market sentiment steady and range-bound.

Leave a Reply