- South African offers correct amid softer freight, muted buying

- Sponge iron prices improve, but coal procurement stays cautious

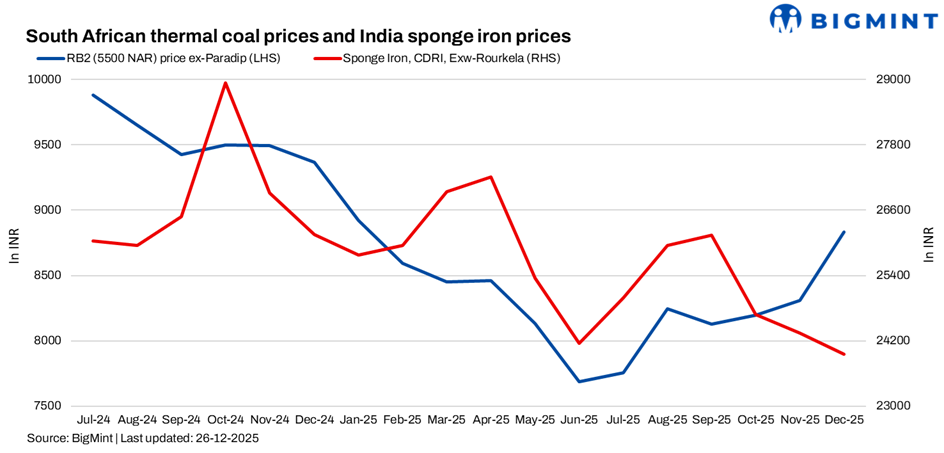

South African thermal coal prices softened across Indian ports during the week ended 26 December, as buying interest remained subdued amid a year-end slowdown. As per BigMint’s assessment, RB2 (5,500 NAR) ex-Paradip, Vizag and Gangavaram declined to INR 8,850-8,900/t w-o-w. RB3 (4,800 NAR) eased to INR 7,500/t ex-Vizag, down INR 50/t, while remaining stable at INR 7,550/t ex-Paradip and ex-Gangavaram. After a prolonged upward trend, offers corrected as freight rates dropped to around $12 from $14 last week. With Christmas and New Year holidays approaching, international markets remained largely inactive, further dampening trade momentum.

Domestic coal prices stayed stable w-o-w. According to BigMint’s assessment, 5,000 GCV was unchanged at INR 5,750/t, while 4,500 GCV remained at INR 4,800/t. Coal availability continued to remain comfortable across key consuming regions, keeping procurement largely need-based despite some improvement in downstream sentiment.

India’s sponge iron market showed firmer trends across most regions. CDRI ex-Rourkela rose INR 500/t w-o-w to INR 24,300/t. Prices across major markets increased by INR 50-300/t, supported by improved sentiment and firmer offers from key producers following better realisations earlier. Central and eastern regions led the recovery, with sellers attempting higher offers amid relatively improved conditions. However, buyers largely stayed cautious and adopted a wait-and-watch approach.

In contrast, southern markets remained mixed. Sponge iron prices declined by INR 100/t in Hyderabad and Bellary due to weak enquiries and sufficient material availability from earlier bookings. Chennai was an exception, where prices edged up INR 200/t on local demand support.

Portside thermal coal inventories increased 1.8% w-o-w to 13.31 mnt in the week ended 19 December, compared with 13.07 mnt in the previous week. While overall stocks rose, uneven distribution across ports continued to influence localised price movements.

Outlook

Coal market activity is expected to remain subdued in the next two weeks amid year-end holidays, and as the market waits for fresh downstream demand cues once normal trading resumes in the new year.

Leave a Reply