- Consistent offtake from West Asia, Europe help anchor basmati exports

- Non-basmati exports fluctuate on cautious buying, policy uncertainty

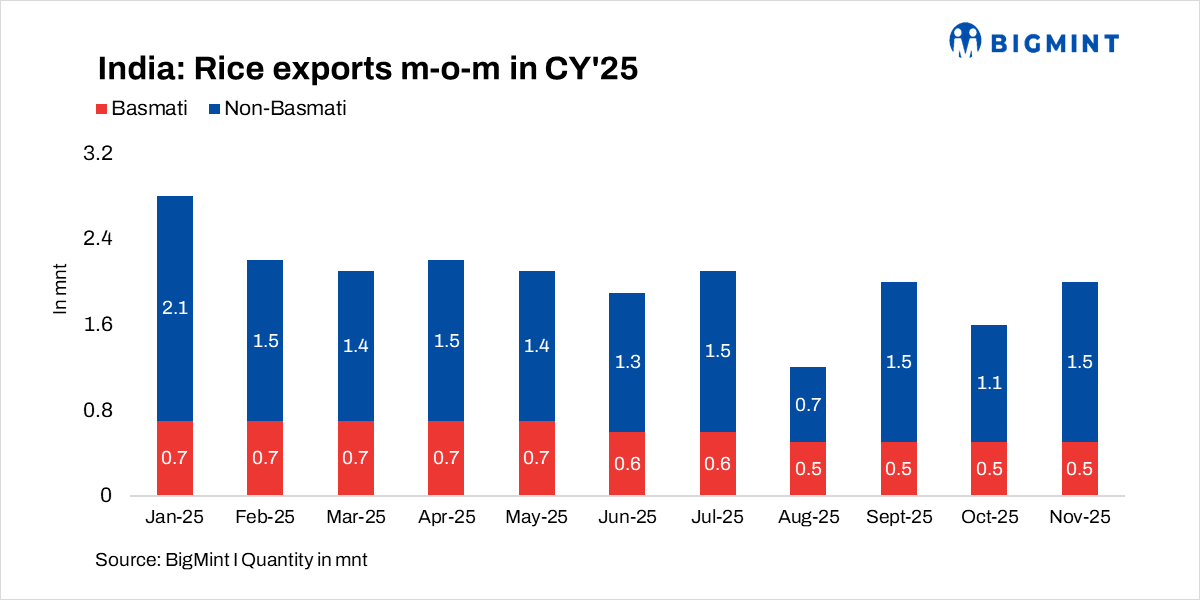

India’s basmati rice exports remained largely stable through CY’25, reflecting resilient demand from premium markets despite seasonal shipment adjustments. Volumes averaged about 0.7 million tonnes (mnt) per month from January to May before easing to 0.6 mnt in June and July and settling at around 0.5 mnt from August through November.

The gradual decline points to normal seasonality rather than demand weakness, with exporters managing shipments to protect price realisations amid firm paddy costs and limited aged-stock availability. Consistent offtake from West Asia and Europe helped anchor exports at a stable base in the second half of the year, even as shipments faced intermittent pressure from geopolitical disruptions, including US tariff uncertainty and Iran’s economic crisis, alongside domestic weather-related setbacks such as floods impacting crop quality, and intensifying competition from other global suppliers. The US imposed a 25% tariff on Indian rice imports (mainly targeting basmati), which affected supply to this market.

The US administration has also accused India of “dumping” rice, a claim India has rejected. Heavy rainfall and floods in India’s major basmati-growing regions, particularly Punjab, in August and September 2025, negatively impacted the crop yield and quality. Pakistan benefits from not using certain pesticides (such as Tricyclazole) that are common in India, giving it a competitive edge in markets such as Europe, where standards are stricter.

Non-basmati shipments swing amid policy, demand uncertainty

Non-basmati rice exports showed marked volatility, starting at 2.1 mnt in January before falling to the 1.4-1.5 mnt range through mid-year. August marked a sharp dip to 0.7 mnt as buyers delayed purchases amid policy uncertainty and expectations of improved supply visibility. Indian non-basmati rice struggled with price competitiveness compared to offers from Thailand, Vietnam, and Pakistan, whose weaker currencies against the US dollar made their exports more affordable.

Many traditional importing countries in Africa had surplus stocks from the previous year, leading them to cut down on new purchases. Shipments rebounded in September, softened in October, and recovered again in November, underlining stop-start buying rather than sustained demand momentum.

Outlook remains cautious into year-end

Looking ahead, basmati exports are expected to remain at these levels, supported by steady premium demand but capped by high raw material costs. Non-basmati shipments are likely to stay volatile, tracking policy clarity, government stock positions, and buying patterns from price-sensitive destinations. Overall export momentum will hinge on clearer policy signals and the pace of fresh crop arrivals.

However, reports from late CY’25 project a strong recovery and a potential new record for India’s total rice exports in FY’26, driven by a domestic surplus and a strategic push into new markets as global trade dynamics evolve and prior policy constraints ease. Despite these challenges, official projections for FY’26 anticipate a recovery and potential record-high exports overall due to robust domestic production and efforts to enter new markets such as Japan and Indonesia.

Leave a Reply