- China property sector support expectations aid outlook

- Delays in Southeast Asia smelter expansions persist

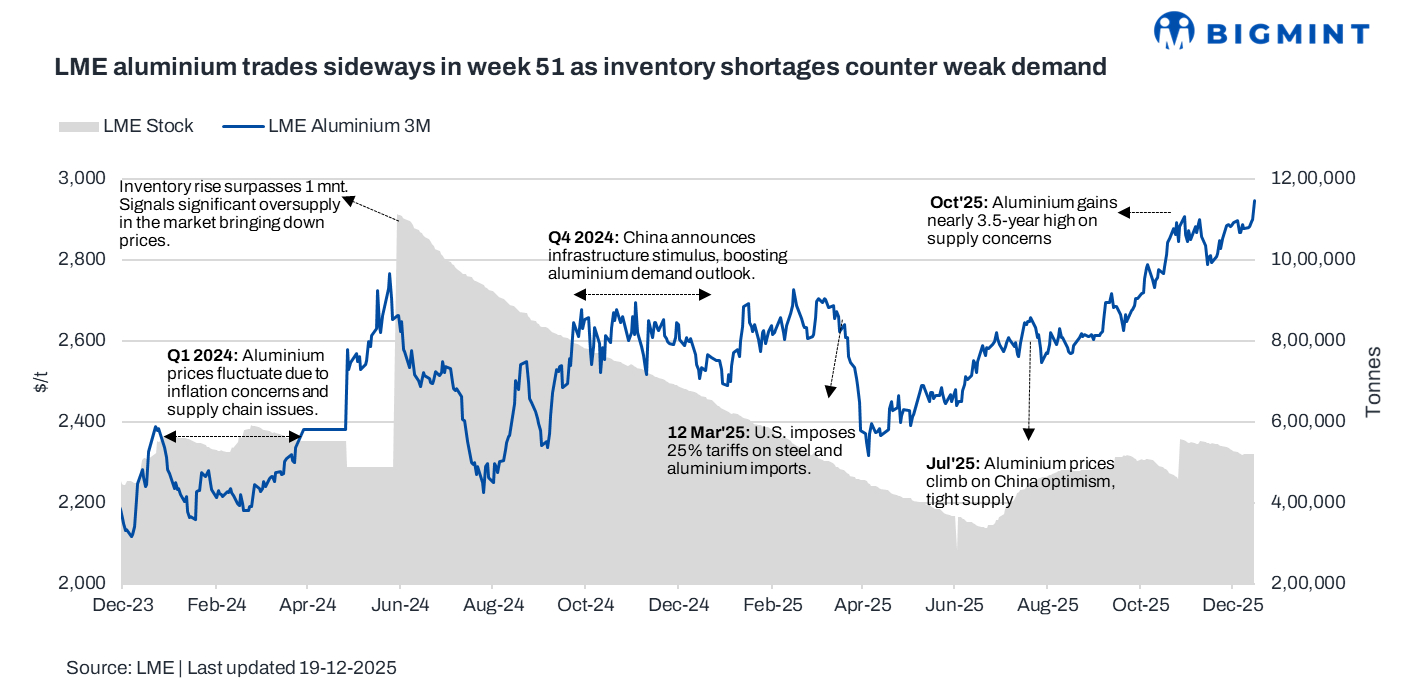

Aluminium prices on the London Metal Exchange (LME) increased slightly during the week ended 19 December. The increase in aluminium prices was supported by improving demand expectations due to a potential China stimulus and persistent global supply constraints, including capped output, delayed smelter expansions, and ongoing operational disruptions that have tightened overall availability.

Pricing, inventory trends

LME aluminium prices averaged $2,900/tonne (t) in the week ended 19 December, marking an increase of $21/t or 0.7% increase w-o-w. Prices opened the week largely rangebound at around $2,880/t before edging higher to around $2,898/t by mid-week. Prices eventually closed at $2,945/t on 19 December.

Meanwhile, LME aluminium inventories witnessed outflows, with stocks marginally down by 0.4% at 519,600 t against 521,660 t in the previous week.

Factors impacting prices

Market sentiment was bolstered by optimism around potential policy support measures from China aimed at stabilising the property sector, which lifted expectations for downstream metal consumption. While broader macroeconomic uncertainty and cautious investor positioning limited aggressive upside, the demand outlook was sufficient to keep prices on a firm footing through the week.

On the supply front, concerns remained pronounced, providing a strong underlying support to prices. China’s aluminium output is nearing its regulatory production ceiling, restricting scope for further capacity additions, while delays in new smelter projects across Southeast Asia have slowed incremental supply growth. These issues have been compounded by ongoing operational disruptions at select global smelters, tightening availability in the physical market. As a result, producers continued to command stronger negotiating power, reinforcing bullish sentiment and underpinning the w-o-w rise in aluminium prices.

Outlook

Aluminium prices are likely to remain supported as supply-side constraints continue to limit availability, particularly with China operating close to its output cap and delays persisting in new smelter additions. While expectations of policy support in China could lend intermittent demand-side optimism, broader macroeconomic uncertainty may cap sharp upside. Overall, the market is expected to trade with a firm bias, with prices sensitive to developments in global production disruptions and signals on downstream demand recovery.

Leave a Reply