- Australia and Brazil drive weekly iron ore exports despite weak freight

- Declines in South Africa, Canada, Chile, and Peru cap overall export gains

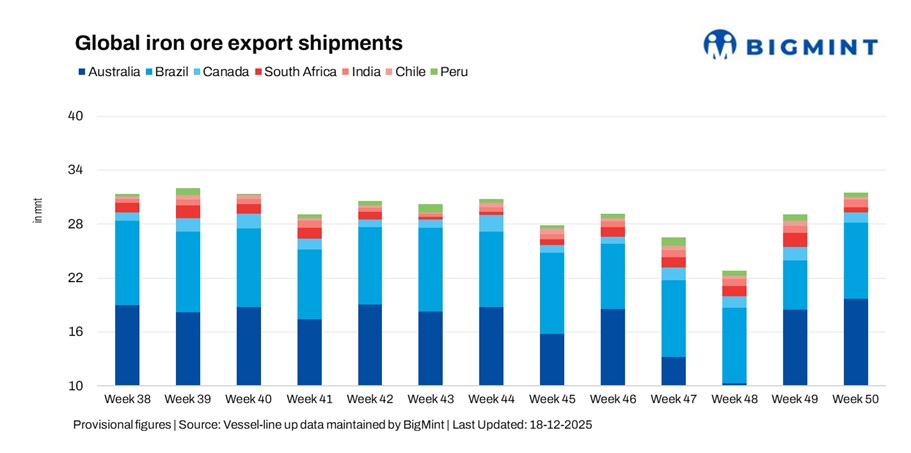

Global seaborne iron ore exports increased 8.7% w-o-w to 31.56 million tonnes (mnt) in the week ended 12 December, up from 29.02 mnt in the previous week, supported primarily by higher shipments from Australia and Brazil, according to the BigMint’s vessel line-up data. The weekly rise was recorded despite a broadly softer freight environment, as exporters released deferred cargoes and benefited from steady operational performance at key ports.

Australian exports continued to build on prior momentum, while Brazil staged a sharp recovery after the previous week’s decline. In contrast, shipments from South Africa, Canada, Chile, and Peru fell w-o-w, reflecting uneven cargo availability, scheduling constraints, and the impact of weaker long-haul freight sentiment. Softer Chinese demand visibility and cautious chartering behaviour also weighed on flows from several mid-sized suppliers.

Freight market sentiment turned bearish during the week, with falling freight derivatives, thin Pacific inquiries, and rising vessel availability pressuring rates across major routes. While the softer freight environment supported some short-haul movements, it constrained long-haul shipment economics, contributing to the mixed country-wise export performance observed during the week.

Country-wise trends

Australian iron ore exports extend gains

Australia’s iron ore exports increased 6.5% w-o-w to 19.67 mnt in the week ended 12 December, up from 18.47 mnt in the previous week, marking a second consecutive weekly rise. The improvement was underpinned by steady and uninterrupted loadings from Western Australian ports as miners continued to normalise shipment schedules following earlier volatility. Port Hedland led with 11.29 mnt, supported by Walcott at 4.55 mnt and Dampier at 3.46 mnt, reflecting broadly balanced port performance across the region.

On the demand side, China remained the dominant importer, absorbing 15.48 mnt, while Japan and South Korea received 1.92 mnt and 1.51 mnt, respectively. Export volumes were driven primarily by Rio Tinto (8.0 mnt), followed by BHP (5.97 mnt) and FMG (3.98 mnt). While Australia has traditionally relied on Western Australia for iron ore, emerging projects in other states are gradually adding supply, diversifying risk, and supporting the country’s competitiveness — particularly through high-grade, cleaner ores aligned with green steel production — without displacing WA’s dominant role. This includes Rio Tinto’s Gudai-Darri mine, its newest and most advanced Pilbara asset, currently producing 43 mntpa with plans to lift capacity to 50 mntpa.

Brazil rebounds sharply on release of deferred cargoes

Brazilian iron ore exports jumped 53.8% w-o-w to 8.50 mnt, rebounding sharply from 5.53 mnt in the previous week, as several deferred stems were released following earlier freight and tonnage related delays. The recovery was led by Ponta da Madeira, which loaded 3.74 mnt, followed by Tubarao at 1.94 mnt and Itaguai at 1.71 mnt, underscoring a broad-based pickup across major export terminals and a normalization of loading schedules.

On the demand side, China remained the dominant destination, absorbing 4.62 mnt, while Malaysia imported 0.39 mnt, and Japan and Oman received 0.32 mnt each. Export activity was largely driven by Vale (4.04 mnt) and CSN (3.64 mnt), together accounting for the bulk of shipments. Improved vessel positioning and a brief stabilization in long-haul fixing conditions supported higher loadings; however, overall market sentiment stayed cautious, with charterers continuing to resist firmer freight ideas, suggesting that the rebound was more a release of pent-up volumes than a clear shift in underlying demand.

Canada exports ease on weaker spot activity

Canada’s iron ore exports fell sharply by 24.9% w-o-w to 1.15 mnt in the week ended 12 December, down from 1.53 mnt in the previous week, as fresh cargo nominations slowed amid subdued spot demand. Shipments were evenly split between the two key loading ports, with Sept Iles accounting for 0.58 mnt and Port Cartier 0.57 mnt. On the supplier front, AMNS led exports with 0.57 mnt, followed by Guinea & Nimba Mines at 0.35 mnt and IOC at 0.23 mnt, reflecting a more selective loading programme compared to the previous week.

On the demand side, France emerged as the largest destination with 0.39 mnt, while China received 0.17 mnt, indicating relatively modest intake levels. Although port operations remained stable, softer Atlantic freight sentiment and cautious chartering activity weighed on overall export momentum. The combination of weaker freight cues and limited buying interest curtailed fixing activity, leading to a noticeable pullback from the stronger performance seen in the prior week.

South Africa shipments drop sharply

South Africa’s iron ore exports plunged 60.6% w-o-w to 0.59 mnt, down sharply from 1.50 mnt in the previous week, marking a significant pullback after a period of elevated shipments. All recorded volumes were shipped from Saldanha Bay, with the decline reflecting a combination of subdued trading activity, limited fresh cargo nominations, and scheduling constraints that curtailed loading programmes.

On the demand side, Japan emerged as the leading importer, taking 0.24 mnt of South African iron ore. Weak sentiment on long-haul routes, coupled with cautious chartering and a lack of new enquiries, further weighed on export momentum, keeping regional flows under pressure despite stable port operations. Meanwhile, Anglo American has also received Canadian approval to merge with Teck, forming Anglo Teck, a Canada-headquartered mining giant, while its South African operations are now largely limited to Kumba Iron Ore.

Indian exports rise on steady regional demand

India’s iron ore exports rose 11.1% w-o-w to 0.84 mnt in the week ended 12 December, up from 0.76 mnt in the previous week, supported by steady loadings from east coast ports. Dhamra led shipments with 0.29 mnt, followed by Paradip at 0.25 mnt, reflecting stable operational performance and a consistent flow of cargo nominations from key exporters.

On the demand side, China remained the leading destination, importing 0.30 mnt of Indian iron ore. Stable Supramax vessel availability and reliable regional demand allowed Indian exporters to sustain growth, even as broader freight sentiment softened, helping the market retain a measured but positive export trajectory.

Chilean shipments retreat after prior rebound

Chile’s iron ore exports fell 43.1% w-o-w to 0.32 mnt, reversing part of the strong recovery seen in the previous week. Shipments were concentrated at Totoralillo (0.17 mnt) and Huasco (0.15 mnt), with the decline largely driven by limited fresh cargo availability and softer chartering interest in the Pacific, which constrained new fixtures.

On the demand side, China and Japan were the key destinations, importing 0.17 mnt and 0.15 mnt, respectively. Despite continued Chinese buying interest, cautious fixing behaviour and uneven vessel positioning weighed on overall export momentum, resulting in a subdued shipment profile for the week.

Peruvian exports fall on reduced cargo availability

Peru’s iron ore exports declined 27.6% w-o-w to 0.49 mnt, down from 0.67 mnt in the previous week, as reduced cargo nominations and scheduling delays constrained loading activity. Exports were entirely driven by Shougang Hierro, with San Nicolas serving as the sole loading port, both accounting for 0.49 mnt, highlighting a highly concentrated shipment profile for the week.

On the demand side, China was the primary destination, importing 0.31 mnt of Peruvian iron ore. Despite a generally workable mid-range Pacific freight environment, limited cargo availability and timing-related constraints weighed on overall export volumes, preventing a steadier flow of shipments.

Iron ore freight market turns bearish

Iron ore freight market sentiment turned decisively bearish in the week ended 12 December, as falling freight derivatives, thin Pacific cargo enquiries, and ample vessel availability weighed on rates across both the Atlantic and Pacific basins. Softer visibility on Chinese demand and a slowdown in winter restocking reduced chartering appetite, while the steady build-up of open tonnage prevented any meaningful rate recovery, keeping owners under pressure.

Although some cargo flow emerged from Brazil and West Africa, fixtures were largely concluded at lower levels, reflecting cautious and price-sensitive charterer behaviour. Subdued activity out of South Africa and a cooling Indian Ocean Supramax market further compounded the weakness, constraining long-haul shipment economics and resulting in uneven export performance across key iron ore origins.

Outlook

Global iron ore exports are expected to remain mixed through December, with Australia likely to maintain firm shipments due to short-haul advantages, strong Asian demand, and efficient operations. Brazil’s exports remain sensitive to long-haul freight conditions, while mid-sized and smaller exporters may face ongoing week-to-week volatility due to cautious chartering and selective fixing. Unless Chinese demand improves and freight markets stabilise, a sustained upside in global exports appears limited, with uneven shipment momentum across regions.

Meanwhile, Rio Tinto has approved a $294 million feasibility study for the Rhodes Ridge iron ore project in the Pilbara. The project could produce 40-50 million tonnes per year and become a long-term pillar of Australia’s iron ore industry.

Leave a Reply