- Imported scrap demand capped by weak steel consumption

- Mills prioritise liquidity and inventory control

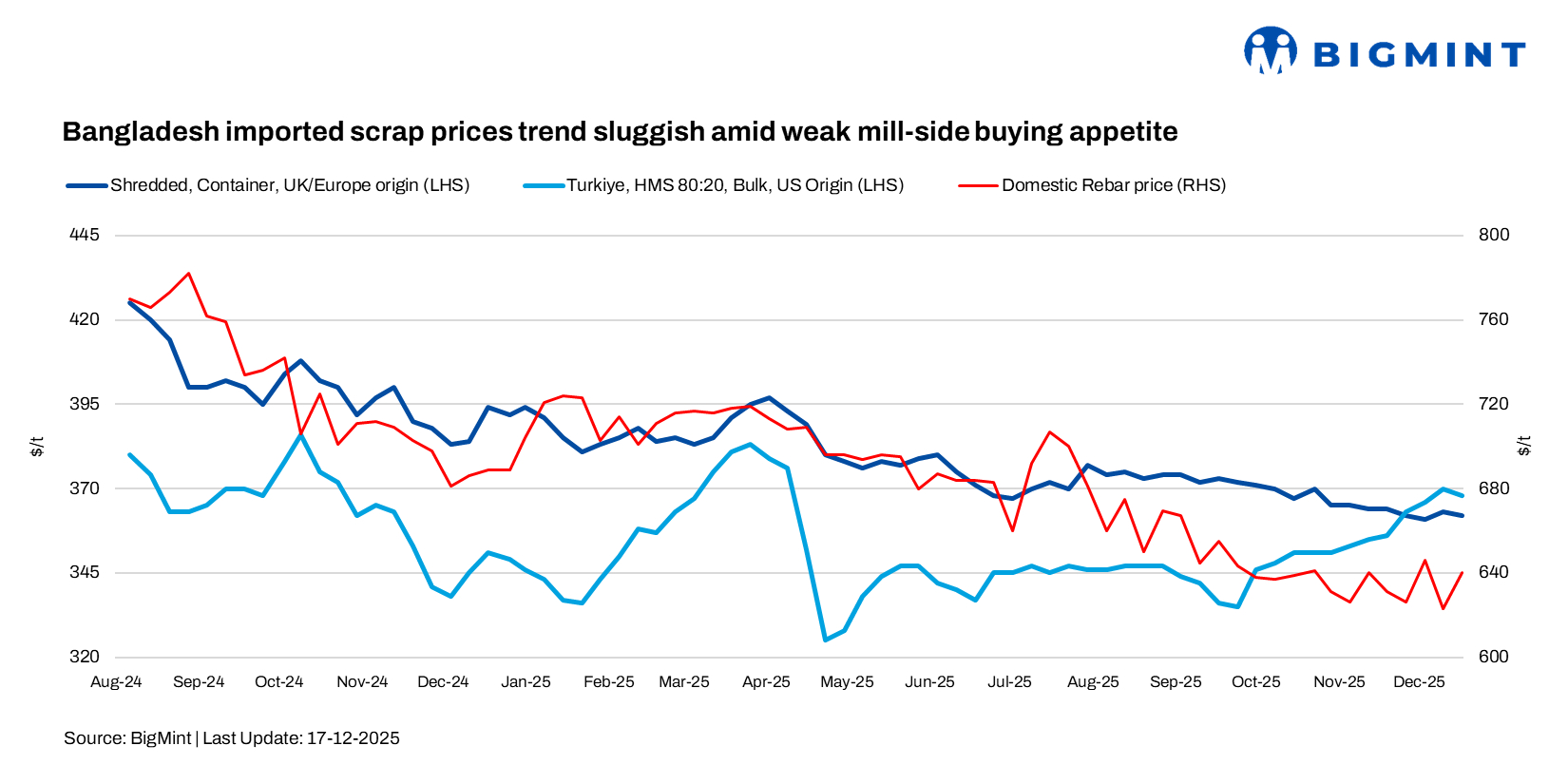

Bangladesh’s imported scrap market continued its sluggish trend in the third week of December 2025, reflecting year-end slowdown in the steel sector and subdued buying from mills. Containerised prices stayed largely unchanged, with Australia origin HMS 80:20 at $330-332/t CFR, Middle East origin HMS 1 at $338-342/t CFR, shredded at $358-360/t CFR, and PNS at $364-365/t CFR (Singapore).

As per market insiders, Australian scrap flows into Asia narrowed sharply as steel demand weakened across Bangladesh, India, and Pakistan, while Indonesia halted scrap imports due to licensing and contamination issues. Australian HMS 80:20 was reported selling as low as $270-275/t FAS Melbourne, shown the stressed regional market and limited outlet options.

BigMint’s weekly assessments

- European-origin HMS (80:20) held at $342/t inched up by $1/t w-o-w

- European-origin containerised shredded inched down by $1/t w-o-w to $362/t.

- Japanese-origin H2 bulk hold steady w-o-w to $342/t.

- US-origin HMS (80:20) bulk remained unchanged w-o-w to $356/t.

Bulk cargoes drew limited interest, with US-origin HMS quoted mostly at $355-360/t CFR, while Japanese H2/HS offers at $345-355/t CFR failed to attract buyers.

Major Chattogram based mills showed selective bulk inquiries, but restocking activity remained below normal seasonal expectations.

Domestic market

Domestic steel prices remained under pressure, reflecting weak construction demand. Billet prices were assessed at BDT 63,000-64,000/t ($516-524/t), while rebar traded at BDT 74,000-78,000/t ($606-639/t). Local melting and ship-scrap prices softened to BDT 45,000-50,000/t ($369-409/t) amid poor rolling margins and cautious furnace operations.

Overall domestic sentiment stayed defensive, with mills prioritising inventory control over fresh raw-material intake.

Sentiment weakened further after reports that Bangladesh’s government may cut foreign project aid by BDT 140 billion ($1.15 billion) in the FY26 Revised ADP, reducing total foreign aid allocation to BDT 720 billion ($5.90 billion). Sluggish implementation of development projects has raised concerns over future steel demand–particularly infrastructure-linked consumption–adding another layer of caution to the scrap market.

Bangladesh’s ship recycling sector showed mixed signals. Chattogram remained the most active yard in November, receiving multiple LNG carriers, an MR tanker, and a mini cape, including HKC-compliant units. However, weakening local currency, falling steel plate prices, high freight rates, and political uncertainty ahead of the February 2026 elections forced recyclers to lower bids. Recent vessel sales below market benchmarks dragged prices down, with conventional vessel offers now hovering near or below $400/LDT, pointing to a quieter period ahead.

Outlook

Bangladesh’s scrap market is expected to remain subdued over the course of December, with weak steel demand, and tight liquidity continuing to cap both imported and domestic activity. Any meaningful recovery is likely to depend on improvements in construction demand, project executions.

Leave a Reply